![]()

![]()

![]()

![]()

12-Month Forecast, Updated 30th November 2020

Our previous 12-month forecast update was three months ago. Although a

lot has happened in the world and financial markets since then, our

intermediate-term views are pretty much unchanged.

What transpires in the major financial

markets over the coming 12 months hinges to a large extent on what happens

to "inflation"* and the US dollar's exchange rate, which are, themselves,

inter-related (what happens to the US$ has a big influence on what happens

to "inflation", and vice versa). This is often the case, by the way, in

that if you are right about the US$ and "inflation" you stand a good

chance of being right about the stock, bond, gold and commodity markets.

Regarding "inflation", our 12-month

lookahead is unchanged since the start of this year. In January we wrote

that the next 12 months would involve a substantial (by the standards of

the past 10 years) increase in what most people think of as "inflation".

Obviously there was a huge detour during March-April as the developed

world experienced the most intense deflation scare ever thanks to

government-imposed economic shut-downs in reaction to the COVID-19

pandemic. However, the monetary and fiscal responses to the debilitating

effects of the shut-downs combined with the semi-permanent damage to the

production structure should ensure that "inflation" indicators such as the

US CPI are at 10-year highs by the second quarter of 2021. This prediction

is unchanged from our previous update.

In effect, policymakers have taken

actions that simultaneously will limit supply and bring about a large

increase in monetary demand. The idea that this will lead to much higher

prices for many things should not be controversial.

The following excerpt from our

previous 12-month forecast update (in July-2020) remains applicable:

"The

idea of a Q1-2020 detour followed by a steeper move in the direction

originally envisaged applies almost across the board to the markets we

track. For example, in January we forecast that the Dollar Index (DX)

would trend downward over the ensuing 12 months as the US stock market

became a relative laggard and as 'capital' shifted towards the economies

that provided the most leverage to commodity production, and that the

Australian dollar (A$) would be the strongest of the major currencies. The

"coronacrisis" prompted a scramble for US dollars during the first half of

March that led to a rapid rise in the DX and a crash in the A$, but since

the third week of March the DX has trended downward and the A$ has been

the world's strongest major currency by a wide margin."

Since we wrote the above, evidence has

emerged to support our view that the US stock market will become a

relative laggard. As illustrated by the following weekly chart, the S&P500

ETF (SPY) peaked relative to the iShares MSCI Eurozone ETF (EZU) in

early-May and made a lower high in October. A lower low would confirm the

trend shift in relative strength.

With regard to expected performance

over the coming 12 months we remain bullish on the A$ and bearish on the

DX, although we acknowledge the risk of significant countertrend moves

over the coming 2 months.

Also still applicable are the

following comments regarding commodities:

"...in

January we wrote that the monetary inflation rebound promoted by central

banks would boost the prices of industrial commodities such as oil and

copper to a far greater extent than it boosted economic growth and overall

corporate profitability. This is starting to become evident. It's likely

that oil and the stocks of oil producers will perform worse over the

course of 2020 than we expected in January, but industrial metals and the

associated equities look set to do as well as originally expected.

Furthermore, oil should return to its January-2020 high (near $60) or

higher by the second quarter of next year."

The oil sector was comparatively slow

to rebound from the major economic dislocation that occurred during

March-April, but it has started to play catch-up and looks set to

outperform over the bulk of the coming 12 months. However, it should be

kept in mind that the nascent oil-stock rally is part of a much bigger

story. Specifically, we are witnessing a cyclical rise in commodity prices

driven by monetary and fiscal profligacy combined with government-imposed

production obstacles and extreme relative under-valuation.

Regarding the US stock market, in our

previous 12-month forecast update we wrote that we expected the SPX to

exceed its early-2020 all-time high during the first half of next year if

not sooner, but that the new high would be solely the result of US$

depreciation. In other words, it looked to us like the US stock market's

'real' bull market top was in the past. We will stick with that assessment

for now.

As an aside, if you sell short and the

price goes up you will lose money regardless of whether the price gain is

'real' or solely the result of currency depreciation. In general, it isn't

a good idea to be short the stock market at a time when central banks and

governments are throwing huge amounts of money around, although individual

stock shorts could still work.

Our outlook for the US economy has

been essentially unchanged over the past six months. We are expecting the

economic rebound that got underway during May-June of this year to peak by

the middle of next year at well below the January-2020 level and for the

US economy to be back in official recession territory by the first half of

2022.

Turning to the bond market, again

there's no change in our 12-month outlook. We expect that bond yields will

rise over the coming 12 months and that the yield curve will continue its

steepening trend (in response to rising inflation expectations), but that

the magnitudes of both moves will be less than they 'should' be due the

actions of the Fed and other central banks.

We expect that gold will resume its

long-term upward trend in US$ terms by early next year, but we think that

it made a multi-year peak in A$ terms and relative to the S&P Spot

Commodity Index (GNX) during March-April of this year. Due to the

sentiment boost it will get from new highs in the US$ gold price, the gold

mining sector should perform well next year.

Summing up, we continue to expect that

the price trends that were set in motion between mid-March and mid-April

of this year will extend well into next year. This means that we are

looking for continued weakness in the US$ and strength in the commodity

currencies, across-the-board strength in commodity prices, strength in

gold in US$ terms but not in terms of industrial metals or the GNX,

strength in non-US equities relative to US equities, and strength in the

gold mining sector of the stock market.

*There

are many ways to define inflation. We put quotation marks around the word

to indicate that in this case we are using the popular/mainstream

definition -- an increase in the general price level as measured by the

CPI.

12 Month Forecast,

updated 29th July 2020

We published a 12-month forecast on 20th January, 2020. Due to government

decisions to lock down large parts of many economies in response to a flu

virus, this forecast was overwhelmed by events over the ensuing two

months. We therefore did a forecast update on 15th April, but at that time

there were too many unknowns to be specific.

Probably the most

important part of our January-2020 forecast was our outlook for

"inflation", the reason being that most of our market views hinged off our

"inflation" view. In January we wrote that the next 12 months would

involve a substantial (by the standards of the past 10 years) increase in

what most people think of as "inflation". In April we didn't change our

"inflation" forecast, but an adjustment was appropriate.

We

explained the adjustment using a metaphor. We wrote: "Originally, we

were going to take a flight from Singapore to northern California. Now, we

will be flying from Singapore to Alaska, but we will be getting there via

New Zealand." In other words, there was going to be even more

"inflation" than originally envisaged -- after a big move in the opposite

direction.

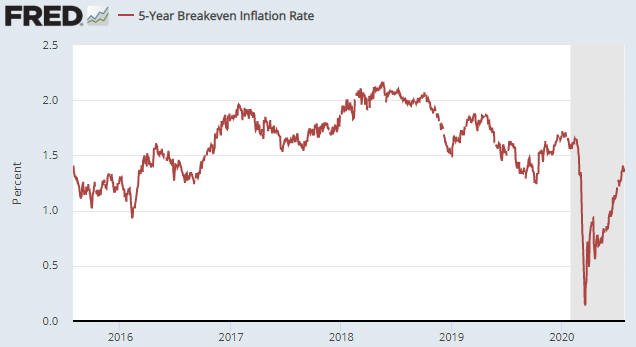

By way of additional explanation, here is a chart that

shows the "5 year breakeven inflation rate". In effect, this chart shows

the expected (by the market) yearly rate of CPI growth over the next few

years. This year started at around 1.7%, after which there was a plunge to

around 0.2% and then an upward move to around 1.4%. We think that the

post-March-2020 upward trend is destined to continue over at least the

next 12 months.

Our reason for expecting much higher "price inflation" was/is not only

the tremendous size of the monetary response to the economic damage caused

by the lockdowns, but also the way the new money was/is being distributed.

Of particular relevance, unlike the previous bouts of Quantitative Easing

that were totally focused on pumping money into the financial markets,

this time around a lot of new money has been and will continue to be

provided directly to businesses and individuals. This should ensure that

the 'problematic' inflationary effects (the effects on the prices of

everyday goods and services, as opposed to the prices of assets) of the

2020 money pumping will be much greater.

In the April update we

summed up our adjusted "inflation" outlook by writing: "...the stage

is being set for a veritable tidal wave of new money to meet a reduced

supply of goods and services. This WON'T result in hyperinflation in the

US or other developed economies in the foreseeable future (say, the next

two years), but it very likely will result in much higher levels of "price

inflation" within 12 months of the passing of the immediate COVID-19

crisis."

We don't have to make another adjustment, but it is

now possible to be more specific. The immediate COVID-19 crisis ended in

May-June, so our expectation is that the US (many other countries too, but

the problem will be bigger in the US due to that country's

disproportionately-large increase in government spending) will be

experiencing the highest rate of "price inflation" in more than 10 years

by Q2-2021.

The idea of a Q1-2020 detour followed by a steeper move

in the direction originally envisaged applies almost across the board to

the markets we track. For example, in January we forecast that the Dollar

Index (DX) would trend downward over the ensuing 12 months as the US stock

market became a relative laggard and as 'capital' shifted towards the

economies that provided the most leverage to commodity production, and

that the Australian dollar (A$) would be the strongest of the major

currencies. The "coronacrisis" prompted a scramble for US dollars during

the first half of March that led to a rapid rise in the DX and a crash in

the A$, but since the third week of March the DX has trended downward and

the A$ has been the world's strongest major currency by a wide margin.

For another example, in January we wrote that the monetary inflation

rebound promoted by central banks would boost the prices of industrial

commodities such as oil and copper to a far greater extent than it boosted

economic growth and overall corporate profitability. This is starting to

become evident. It's likely that oil and the stocks of oil producers will

perform worse over the course of 2020 than we expected in January, but

industrial metals and the associated equities look set to do as well as

originally expected. Furthermore, oil should return to its January-2020

high (near $60) or higher by the second quarter of next year.

Regarding the US stock market, in January we wrote:

"The

long-term US equity bull market won't end in 2020, but the January-2020

high for the S&P500 Index (SPX) will be close to its high for the year.

More specifically, we expect a sizable correction from a January high

followed by a rally that makes only a marginal new high (at best) before

the next sizable correction gets underway. In this regard, 2020 will have

a lot more in common with 2018 than with 2017 or 2019."

We

ended up getting a crash rather than just a "sizable correction", but the

SPX actually has followed the expected pattern and probably will continue

to do so. However, it's certainly possible that for all intents and

purposes the long-term equity bull market ended in the first quarter of

this year.

We say "for all intents and purposes" because we think

that the SPX will exceed its early-2020 all-time high during the first

half of next year if not sooner, but that the new high will be solely the

result of US$ depreciation. In other words, it looks like the US stock

market's 'real' bull market top is behind us.

Regarding the US

economy, although coming into this year the message from our favourite

leading indicators was that a recession would begin during the first half

of 2020, we guessed in January that there would be sufficient monetary

inflation to postpone the start of a recession until 2021. The lockdowns

invalidated this guess.

Both the monetary and fiscal responses to

the lockdown-related economic collapse should ensure that there won't be

anything like a complete recovery from the H1-2020 recession for many

years. As explained over the past couple of months, we are expecting the

economic rebound that got underway during May-June of this year to peak

during the first half of next year at well below the January-2020 level

and for the US economy to be back in official recession territory by the

first half of 2022.

Regarding the bond market, in January of this

year we thought that yields would move higher during 2020, but not

substantially so, and that the US yield curve would steepen. The US yield

curve has steepened significantly since early this year, but thanks to the

economic lockdowns the US T-Bond yield made a new all-time low in

March-2020 and has since chopped around near its low. We expect that bond

yields will rise over the coming 12 months and that the yield curve will

continue its steepening trend, but that the magnitudes of both moves will

be less than they 'should' be due the actions of the Fed.

In

general, we expect the price trends that were set in motion between

mid-March and mid-April of this year to continue until at least the second

quarter of next year. This means that with regard to the next 9-12 months

we are looking for continued weakness in the US$ and strength in the

commodity currencies, across-the-board strength in commodity prices,

strength in gold in US$ terms but not in terms of industrial metals or the

S&P Spot Commodity Index (GNX), strength in non-US equities relative to US

equities, and strength in the gold mining sector of the stock market.

As always there will be corrections along the way, with the period

between now and the early-November US election being a likely time-window

for significant countertrend moves.

12 Month Forecast,

updated 15th April 2020

Due to the dramatic events of Q1-2020, the main ones being the

economy-wide shutdowns, the stock market crash that resulted from the

shutdowns, and the massive central bank buying spree prompted by

collapsing asset prices and sky-rocketing job loss numbers, an update to

our 12-month forecast seems appropriate.

Unfortunately, there is so

much uncertainty right now that drawing conclusions about what the future

holds in store is far more difficult than usual. In particular, a great

deal hinges on the timing of a general return to work, which at the moment

is unknown. For example, there's a huge difference for both the financial

markets and the economy between a May-June return to work and an

August-September return to work. Therefore, while we know that our

previous forecast (dated 15th January 2020) has been largely overridden by

events, at this time we simply don't have enough information to do a

comprehensive update.

What we can do right now is address a few

parts of our previous forecast that definitely are not going to happen or

will happen in a very different way, beginning with our forecast that the

next 12 months will involve a substantial (by the standards of the past 10

years) increase in what most people think of as "inflation".

The

two overarching contributors to "price inflation" are the change in the

supply of goods/services and the change in the monetary demand for

goods/services. Thanks to the lockdowns, both sides of this supply-demand

equation have plummeted over the past several weeks. Furthermore, with

regard to big-ticket and discretionary items, demand has fallen much

faster than supply. This should lead to large short-term declines in some

of these prices.

Now, we get the impression that most

policy-makers and commentators are labouring under the assumption that the

economy can be shut down for a few months and then restarted, such that

within a short time almost everything is back to the way it was prior to

the shut-down. However, the economy doesn't work that way. Many businesses

will never be able to restart, many supply chains will be permanently

broken and many jobs will be lost forever. Consequently, the supply side

has suffered a hit that probably will take years to recover from, even if

government restrictions start being lifted within the next few weeks and a

general return to work occurs before mid-year.

The supply side also

will be hurt in the long-term by the massive amount of money that is being

thrown around by governments and central banks in an effort to reduce the

short-term pain. The reality is that governments and central banks do not

have wealth reservoirs that can be drawn upon in times of crisis. All they

can do is redistribute existing wealth and incentivise capital consumption

('eating of the seed corn'). This will ensure that the economy is not as

productive post-crisis as it was pre-crisis.

At the same time, the

new money that is being injected into the economy will give the monetary

demand for goods/services a substantial boost AFTER the immediate crisis

has passed. Note that unlike the Quantitative Easing of 2008-2014, which

involved pumping money into the financial markets, this time around a lot

of new money will be provided directly to businesses and individuals. This

means that the inflationary effects of the current money-creation schemes

will be more apparent in everyday prices than was the case with earlier

schemes.

In summary, the stage is being set for a veritable tidal

wave of new money to meet a reduced supply of goods and services. This

WON'T result in hyperinflation in the US or other developed economies in

the foreseeable future (say, the next two years), but it very likely will

result in much higher levels of "price inflation" within 12 months of the

passing of the immediate COVID-19 crisis.

We can use an analogy to

explain the change to our "inflation" forecast. Originally, we were going

to take a flight from Singapore to northern California. Now, we will be

flying from Singapore to Alaska, but we will be getting there via New

Zealand.

Another part of our previous forecast that can be updated

immediately has to do with recession. Even though our leading indicators

were suggesting that a US recession would begin during H1-2020, at the

beginning of this year we guessed that the US economy would be stagnant

during 2020 and that the strong rebound in monetary inflation throughout

the developed world over the preceding six months would postpone the start

of a global recession until 2021. Due to the widespread lockdowns there is

no doubt that a global recession began in March of 2020, but there isn't

yet enough information to speculate about when the recession will end.

We also can be fairly certain that our previous forecasts regarding

oil and the oil sector will be wrong. In some industrial commodity markets

the lockdown-related supply reductions could, within a few months,

counteract the lockdown-related demand reductions, enabling prices to make

new 12-month highs by the end of this year in response to the coming

increase in monetary demand. The oil market is a different story, though.

Unless war breaks out in the Middle East, an abundance of supply probably

will weigh heavily on the price for the bulk of this year, preventing

anything more bullish than a rebound to the $40s. The low oil price

should, however, eventually take a significant toll on oil supply,

potentially paving the way for a substantial price rise during 2021.

We plan to do our next 12-month forecast update in July. Hopefully by

then the virus-related lockdowns will be over, thus removing a huge source

of uncertainty and enabling us to be more specific about all the markets

we follow.

12 Month Forecast,

updated 20th January 2020

1) The next 12 months will involve a substantial (by the standards of the

past 10 years) increase in what most people think of as "inflation".

Central bank money-pumping, commercial bank money creation, the general

belief that central banks have gone too far in their efforts to promote

"inflation" and an increase in the use of fiscal stimulus leading to

accelerated growth in government indebtedness will contribute to the loss

of money purchasing power. The key, however, will be the spreading

realisation that central banks have begun to act with the express purpose

of monetising government deficits.

2) Rising inflation expectations will lead to an

upward trend in government bond yields (a downward trend in government

bond prices) throughout the developed world, but a major rise in interest

rates won't happen in 2020. The start of a major rise in interest rates

will wait until after the next global recession.

3) Due in part to the general realisation that the

experiment with negative interest rates has been a total failure, the ECB

will come under irresistible political pressure to end this experiment.

Consequently, bond yields will rise further (bond prices will fall

further) in Europe than in the US.

4) When the global quantity of negative-yielding

debt soared to around US$17T in August-2019 we wrote that this was a type

of bubble peak and that the quantity of such debt would reduce to zero

within two years. Due largely to rising interest rates in Europe, this

forecast will come to fruition in 2020.

5) Rising inflation expectations will put upward

pressure on long-term interest rates relative to short-term interest

rates, causing the US yield curve to steepen. The steepening of the yield

curve will be assisted by the Fed keeping its boot on interest rates at

the short end of the curve.

6) Due to a strong rebound in monetary inflation

throughout the developed world over the past six months and signs that

China's central planners have begun to loosen the monetary reins, a global

recession won't begin until 2021. However, the US tariffs on Chinese

imports will continue to weigh on US economic growth and election-related

uncertainty will become a significant economic depressant at some point,

resulting in a nearly-stagnant US economy during 2020.

7) The monetary inflation

rebound promoted by central banks will boost the prices of industrial

commodities such as oil and copper to a far greater extent than it boosts

economic growth and overall corporate profitability. Oil also will get

boosted during the second half of the year by heightened geopolitical

tensions in the Middle East and the resultant threat of a supply shock.

Consequently, oil will be the US stock market's best-performing major

sector by a wide margin.

8)

Due largely to rising long-term interest rates and a steepening yield

curve, US bank stocks will perform better than the broad market. However,

thanks in part to the large gains that were made by these stocks during

the final four months of 2019, absolute returns won't be impressive.

9) In response to the scaling back and eventual

removal of the ECB's destructive negative interest rate policy (NIRP),

euro-zone bank stocks will perform substantially better than their US

counterparts.

10) Non-US

equities in general and European equities in particular will do better

than US equities as the combination of high average valuation and slow (or

no) earnings growth finally begins to weigh on the US stock market.

11) The Dollar Index will trend downward as the US

stock market becomes a relative laggard and as 'capital' shifts towards

the economies that provide the most leverage to commodity production. The

Australian dollar will be the strongest of the major currencies.

12) The long-term US equity bull market won't end

in 2020, but the January-2020 high for the S&P500 Index (SPX) will be

close to its high for the year. More specifically, we expect a sizable

correction from a January high followed by a rally that makes only a

marginal new high (at best) before the next sizable correction gets

underway. In this regard, 2020 will have a lot more in common with 2018

than with 2017 or 2019.

13)

Despite a lacklustre economy and stock market, Donald Trump will be

re-elected in November-2020 thanks mainly to the lack of a viable

alternative. However, the stock market's celebration will be short-lived

due to the massive protests that will erupt during the weeks following the

election.

14) The US$ gold

price will make a 12-month high during the first quarter of 2020.

Thereafter it will move in a wide range, with the effects of its relative

expensiveness and precarious sentiment situation being offset by

supportive fundamentals stemming from economic and political uncertainty.

15) Silver will outperform gold, but copper and

zinc will outperform silver. As a result, base-metal mining stocks

generally will do better than gold or silver mining stocks.

16) The Fed will be like a deer in the headlights.

It will be concerned about rising "inflation", but it will be dissuaded

from rate-hiking by stock market volatility and generally lacklustre

economic data. However, in a 'hat tip' to the evidence of increasing

"inflation" the Fed will end its balance-sheet expansion by April-2020.

As an aside, there is a largely-irrelevant debate

happening in the world of market commentators as to whether the Fed's

latest asset monetisation program is Quantitative Easing (QE). The Fed

claims that it is not QE because the program was not introduced with the

aim of easing monetary policy and stimulating the economy, and some

analysts agree. However, the Fed's reason for implementing a policy does

not determine the nature of the policy. The Fed's provision of 'liquidity'

to the "repo" market involves very short-term loans and therefore is not

QE, but the $60B/month asset monetisation program introduced by the Fed in

mid-October of last year has exactly the same effects on bank reserves and

the money supply as the QE programs of 2008-2014. Regardless of the Fed's

stated or actual motivation, the program eases monetary conditions by

increasing the quantity of money. It is, by definition, quantitative

easing. That's a fact.

17)

The periodic stock market swoons will not help the Treasury market,

because government bonds will stop being perceived as safe havens.

18) Due to the combination of adverse changes in

climate (the changes aren't caused by humans, but that's a separate

issue), reduced international trade as regions become increasingly

isolationist and the higher cost of bulk commodity shipping due to

IMO 2020, the prices of many agricultural commodities will commence

major upward trends. This will lead to much higher stock prices for

fertiliser producers such as Nutrien (NTR) and Mosaic (MOS).

In addition to the intermediate-term expectations

outlined above, here are some big themes that extend well beyond the next

12 months but still could influence our positioning over the year ahead:

1) The rising interest-rate trend

This is a new secular trend that will evolve into

one of the biggest stories of the 2020s.

2) A paradigm shift in road transportation

Road transportation will be revolutionised in two

ways: Electric Vehicles (EVs) will proliferate during the first half of

the 2020s and during the second half of the 2020s there will be a major

shift away from car ownership due to the combination of automation

(self-driving vehicles) and ride sharing.

A related issue is that most analysts are

forecasting steady growth in EV production, but that's not the way

important new technologies are adopted. Instead, the rate of adoption

tends to follow the

Innovation

S-Curve.

In the bottom

part of the "S", growth is significant but the new technology is yet to

make major inroads. At some point a critical mass of usage is achieved and

the growth becomes explosive. In seemingly no time the technology goes

from being used by a relatively small group of early adopters to being

used by almost everyone. The television, the microwave oven, the personal

computer, the internet and the smart phone all went through "S curves". We

expect that it will be the same story for EVs.

EV usage currently is in the bottom part of the

"S". The big unknown is when the middle part of the "S" will begin. We

doubt that it will begin this year, but it could begin during 2021-2022.

Because most analysts are

not factoring the "Innovation S Curve" into their EV production forecasts,

most current estimates of future demand for the commodities used in the

manufacture of EV batteries and motors will prove to be far too low. A

likely consequence will be much higher prices for battery metals

(primarily lithium, nickel and cobalt at this time) and the rare earth

metals used to make the permanent magnets that go into electric motors.

3) The end of the age of real estate

It will still be possible to achieve good returns

by investing in real estate, but gone are the days when anyone could buy a

house almost anywhere and likely end up with a substantial profit as long

as they held for 10 years or more. From now on only astute investors will

consistently make good returns from real estate, where "astute" means able

to time the cyclical swings in the broad market or able to correctly

anticipate future supply-demand imbalances in specific areas.

For the average person, residential property will

transition from an investment to what it was prior to the 1970s: a

consumer good (something bought solely for its use value).

There are two reasons for the change, the first

being the interest-rate trend. The 3-4 decade downward trend in interest

rates resulted in a 3-4 decade upward trend in housing affordability for

buyers using debt-based leverage (that is, for the vast majority of

buyers). There were corrections along the way, but provided that long-term

interest rates continued to make lower lows there eventually would be a

pool of new debt-financed buyers able to pay a much higher price.

There's a good chance that the secular

interest-rate trend reversed from down to up during 2016-2018. If so,

future house buyers that don't have good timing and/or substantial

area-specific knowledge generally won't make long-term capital gains on

their residential property purchases.

The second reason for the change involves the

availability of credit. Over the past 50 years it became increasingly easy

for the average person to borrow a lot of money using his/her house as

collateral, because the overarching trend was for banks to leverage-up

their balance sheets. However, the high levels of existing indebtedness

and restrictions on the extent to which banks can leverage themselves

probably mean that it will become progressively more difficult to qualify

for a home mortgage.

4)

Under-investment in fossil fuels

Due to political correctness gone mad, many large

investors will steer clear of opportunities in the oil, gas and coal

industries. This will lead to higher energy costs and slower economic

growth than otherwise would be the case.