![]()

![]()

![]()

![]()

- Interim Update 1st May 2019

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The Monthly Closing

Prices

At around this time every month

we review some of the most important (from our perspective) monthly

charts. We do this because monthly closing prices can confirm or deny

intermediate-term trend changes.

A month ago we wrote:

"Gold

could spike down to $1250 or a little lower during April without adversely

affecting its intermediate-term (3-12 month) prospects, but to maintain

its intermediate-term bullish posture it must stay above $1280 on a

monthly closing basis."

Gold traded below its 21-month MA (the

blue line on the following chart) and low enough to test its 8-month MA

(the black line on the following chart) during April, but ended the month

above $1280 and both of the aforementioned MAs. This means that gold's

position on the monthly chart remains bullish.

Unlike the

gold-mining sector and the silver market, the gold market is yet to

generate a significant bearish signal.

Over the past 2-3 weeks the gold-mining sector generated multiple

bearish signals. The latest was GDX's April close below its 21-month MA

(the blue line on the following chart).

The SPX/euro ratio generated a bearish signal when it ended the month

of December-2018 below its 20-month MA, but the signal was invalidated the

following month. SPX/euro has just made a new all-time high, providing

further evidence that a bear market did not begin last year.

There's a high probability that the T-Bond entered a bear market in

2016. As previously mentioned, we expect that the 84-month MA will act as

resistance during the bear market similarly to how it acted as support

during the preceding bull market.

A month ago we noted that the

T-Bond had ended March-2019 slightly above its 84-month MA. Our conclusion

was that it had reached a potential ceiling and that April probably would

be a down month. The following chart shows that the T-Bond lost 2.2 points

during April, which is consistent with our expectation that the 84-month

MA will act as resistance.

Note that we are allowing for the

possibility that the March-2019 rebound high will be tested before the

next leg of the bear market gets underway.

US Recession

Watch

Our three favourite leading

indicators of US recession are the ISM New Orders Index (NOI), Real Gross

Private Domestic Investment (RGPDI) and the yield curve. All three of

these indicators should generate warning signals ahead of the next

recession.

The latest monthly NOI was reported on Wednesday 1st May

and revealed that there was a substantial decline in this measure of

manufacturing-industry strength in April. The index has dropped to near

the 2-year low reached in December-2018 and is now precariously close to

the level it would have to move below (the red line on the following

chart) to warn of a recession.

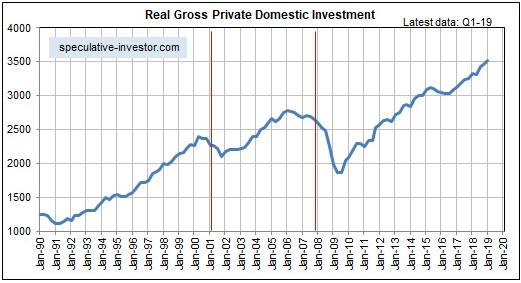

The latest quarterly RGPDI number (for Q1-2019) was published last

week. As illustrated below, RGPDI extended its upward trend and made a new

all-time high in Q1-2019. Given the typical historical lag between a

downward reversal in RGPDI and the start of a recession, this suggests

that a recession won't begin earlier than the final quarter of 2019.

The yield curve generates a recession warning when it 'flattens' to an

extreme and then begins to steepen, regardless of whether or not the

extreme entails an inversion.

The US yield curve is indicated on

the first of the following charts by the 10yr-2yr yield spread and on the

second of the following charts by the 10yr-3mth yield spread. Previously

we focused on the 10yr-2yr spread when assessing the yield-curve trend,

but, to minimise the risk of being whipsawed, from now on we will require

that a reversal be signaled by both of the spreads depicted below.

Both spreads have widened a little over the past month, but not by enough

to signal a trend reversal.

Based on the latest data, our rough estimates of recession start-time

probabilities are:

- Q2-2019: 5% (unchanged from a month

ago)

- Q3-2019: 15% (not specified a month ago*)

-

Q4-2019: 30% (not specified a month ago*)

- Later than 2019: 50%

(unchanged from a month ago)

Overall, there was no significant

change in recession start-time probabilities last month. In effect, the

strength signaled by the extension of RGPDI's upward trend was offset by

the plunge in the ISM New Orders Index.

*A

month ago we didn't have separate probabilities for Q3 and Q4 2019, but we

did have a probability for a recession start in H2-2019. Over the past

month the probability of a recession starting in H2-2019 is unchanged at

45%.

The Stock Market

The S&P500 Index (SPX) made a

marginal new all-time high on Tuesday of this week that was confirmed by a

new all-time high for the NYSE Advance-Decline Line (ADL). It then pulled

back on Wednesday.

At this point, a decline to the 50-day MA (2846

and rising) or lateral support at 2800 would be a normal correction.

Given the continuing upward trend in the ADL we aren't expecting

anything more bearish than a correction over the next few weeks. That

being said, the low monetary inflation rate makes the market acutely

vulnerable to a shift away from risk. We mean that a relatively small

increase in the demand to hold cash (a natural consequence of greater risk

aversion) could result in a very fast unwinding of bullish speculations.

We are thinking of something along the lines of what happened in

January-February of 2018, when the SPX lost 11% of its value within the

space of about two weeks. The decline could even take the form of a "flash

crash".

We wouldn't attempt to trade the aforementioned short-term

risk, but with the SPX testing last year's high it would make sense to

take an INITIAL longer-term bearish position at this time. The position

could be in the form index put options with an expiry date of

January-2020, or a leveraged inverse index fund such as SDS or QID. The

idea would be to make a quick exit (at a profit) if the "flash crash" risk

materialises or otherwise to methodically add to the position over the

next few months in readiness for a large decline later this year.

Gold and the Dollar

Gold

The

following daily chart shows that the US$ gold price oscillated in a narrow

range bounded by its 20-day MA and lateral support at $1280 during the

first three days of this week. Note, though, that the chart doesn't

include the post-FOMC price action. In the aftermath of the Fed news the

gold price dropped into the $1270s, but at the time of writing it hasn't

broken below last week's low.

Despite the financial-market volatility added by the Fed news, the

gold market's position now is not materially different to what it was at

the end of last week. The following comments from the latest Weekly Update

therefore still apply, except that resistance has edged down from $1302 to

$1300.

"Friday's up-move ended at the 20-day MA and there is

significant additional resistance in the form of the 50-day MA and a

downward-sloping trend-line only 1% above the current price (at $1302), so

the gold market still has some heavy lifting to do to confirm an upward

trend reversal. However, it's likely that at least a multi-week price low

is in place.

There's a realistic chance that gold will test its

February high within the coming month, but first it has to get above

resistance at $1302."

Silver

On

Wednesday the silver price fell from the top to the bottom of its

'declining wedge' pattern.

Due to Wednesday's price action, the following paragraph from the 22nd

April Weekly Update is worth repeating:

"Declining wedge

patterns generally are viewed as bullish, but in our experience they

aren't reliable enough to risk money on. The main reason we have drawn the

pattern on the following chart is to illustrate silver's reducing

volatility. The market is 'coiling' and should soon (within the next two

weeks) either resume the upward trend that began last November or

accelerate downward. The former obviously would be more bullish in the

short-term, but the latter could set the stage for a more bullish

intermediate-term outcome."

Silver still hasn't broken out of

its 'wedge', but over the past three days it has 'pushed the envelope' --

first by making a failed attempt to break out to the upside and now by

dropping as far as it can go without breaking out to the downside.

A downside breakout could lead to a quick decline to near major support at

$14.00, which certainly would be an excellent long-term buying opportunity

and possibly would be an excellent short-term buying opportunity. Whether

or not it was an excellent short-term buying opportunity would have to be

determined at the time by looking at sentiment indicators.

As

mentioned in the latest Weekly Update, an upside breakout from the 'wedge'

probably would be followed by a rebound to the $15.60s.

Gold Stocks

At the end of last week we thought that the

gold-mining sector, as represented by GDX, had commenced a minor rebound

(a counter-trend move to resistance within an on-going short-term downward

trend), but it wasn't to be. Instead, we got a 3-day bounce that

culminated last Friday (we were anticipating at least a 1-2 week rebound)

followed by a drop to a new multi-month low on Wednesday 1st May.

Wednesday's decline took GDX down to its 200-day MA, which we had warned

could happen prior to last week's upward reversal. The following chart

shows that GDX managed to hold this moving average on a daily-closing

basis, but note that both the HUI and the XAU ended the day well below

their own 200-day MAs.

The extension of the gold sector's short-term decline opens up the

possibility that the next rebound will be stronger than the counter-trend

move we were anticipating at the end of last week. However, we expect to

be playing defence with our gold-mining exposure for a while yet rather

than attempting to trade rebounds that in the grand scheme of things will

turn out to be unimpressive.

A development that could spur

something more interesting than 5%-10% bounces in the gold-mining indices

and ETFs is a downward reversal in the Dollar Index (DX). To generate

preliminary evidence of such a reversal the DX would have to close below

97.

The Currency Market

At the conclusion

of the FOMC meeting on Wednesday 1st May the Fed issued its updated

comments about monetary policy and the economy. There were no significant

changes in the Fed's planned actions or words, but, strangely, the market

reaction suggested that a significant number of traders were anticipating

a further shift by the Fed into 'dovish territory', that is, a further

shift towards a monetary easing bias. We say "strangely" because it isn't

possible for the Fed to become more 'dovish' without a plausible pretext,

such as a plunging stock market and/or signs that a banking crisis is

brewing. With the senior US stock indices near all-time highs, the Fed is

already as easy as it can be.

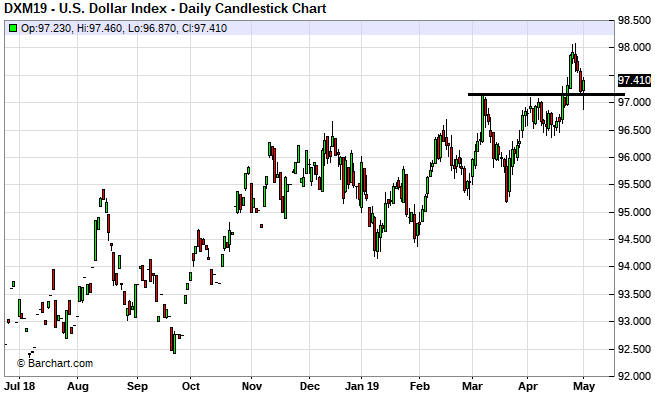

Anticipation that the Fed was about

to become even more 'dovish' is evident in the performance of the Dollar

Index (DX) before the Fed's post-meeting announcement. As illustrated by

the following daily chart, over the first 2 days of this trading week the

June-2019 DX futures contract pulled back to test last week's upside

breakout (it ended Tuesday's session right at the breakout level). It then

traded below the breakout level on Wednesday prior to the Fed's

announcement, potentially setting the stage for a bearish signal in the

form of a failed upside breakout. At this stage, however, last week's

breakout has held.

The price action over the final two days of this

week will be interesting, as the POTENTIAL for a failed upside breakout in

the DX still exists.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Kidman

Resources (KDR.AX) is not in the TSI Stocks List, but in several

TSI commentaries over the past year we have described it as a good way to

gain exposure to lithium.

Kidman

Resources (KDR.AX) is not in the TSI Stocks List, but in several

TSI commentaries over the past year we have described it as a good way to

gain exposure to lithium.

It was announced earlier today that KDR

has received a cash takeover bid from Wesfarmers (a large Australian

conglomerate) at a premium of about 50% to the preceding day's closing

price. This is very good news for KDR shareholders.

There is a

realistic possibility of a higher bid, so shareholders who have no

immediate need for additional cash probably should hold for now.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://www.barchart.com/

![]()