|

- Interim Update 2nd July 2003

The US

Stock Market

Taking Stock

Over the past several weeks we've discussed

some of the things we expect to see in the early stages of the next major

decline in the stock market. Here's a recap on some of these early warning

signals.

1. We won't include a chart of the

NDX/Dow ratio in today's commentary, but as noted many times over the past

6 months we expect the early stages of the next major decline in the stock

market to be characterised by persistent weakness in the NASDAQ100 Index

relative to the Dow Industrials Index. This has been the case with every

substantial decline over the past few years and we don't see why it won't

be the case in the future. The NDX/Dow ratio achieved a new closing high

on Wednesday, so this indicator is NOT signaling that a major decline has

begun.

2. Bank stocks have been leaders in

the rally that began last October and the performance of the banking sector

often indicates the underlying health of both the market and the economy.

If a pullback in the Bank Index (BKX) is a correction within a continuing

uptrend, as opposed to the start of a new major downtrend, it should hold

above 800.

3. The Biotechnology Index (BTK) was

one of the first indices to bottom last year. Given its price action over

the past month it is also likely to be one of the first indices to break

below important support and thus provide an early warning signal that a

major decline in the overall market is underway.

4. The Walmart (WMT) stock price has

tended to lead the S&P500 Index over the past year and may have done

so again when it peaked in late April about 7 weeks prior to the peak in

the S&P500. However, having made a lower high WMT now needs to make

a lower low (by closing below $51.50) to confirm that an intermediate-term

downtrend is in effect. If this happened it would indicate to us that an

important peak was already in place for the S&P500. Conversely, if

WMT were able to close above its April high it would suggest that the S&P500

was at least 6 weeks away from a peak.

5. A normal correction in the NASDAQ100

Index at this stage should hold above support at 1156.

6. If the overall stock market were

close to a peak we would expect to see strength in the gold sector. This

is, in fact, what we have seen over the past few months and, in particular,

since the beginning of May. Notice, on the below chart, how the AMEX Gold

BUGS Index (HUI) broke out to the upside in February of 2002. This upside

breakout occurred about 6 weeks prior to a peak in the Dow Industrials

Index

and represented a warning that the rebound in the overall stock market

from its September-2001 bottom was almost over. As such, when the HUI moves

decisively above the 'triple top' created over the past 13 months (triple

tops almost never hold) it won't necessarily be a sign that a major decline

has begun in the overall market. It will, however, be a sign that a peak

is close at hand.

Current Market Situation

Sentiment has reached levels that are

consistent with what we'd expect to see near a major peak. Also, there

have been signs of distribution over the past 2-3 months. For example,

insiders have been selling stock at a rapid rate and Investors' Intelligence

reports that there were more than 100 buying climaxes on the NYSE in 10

out of the past 12 weeks (a buying climax occurs when a stock makes a new

52-week high and then closes down on the week). However, there is scant

evidence at this stage that a major decline has already begun.

It will be informative to observe how

the market behaves over the next 2 weeks. As discussed in the latest Weekly

Update, this week was likely to see some strength in the market due to

seasonal factors. Beginning next week, though, we'll find out how much

real strength there is.

Bonds

Japanese Government Bonds (JGBs) have

fallen sharply over the past month and at the close of trading on Wednesday

JGB futures were poised right at intermediate-term support (refer to the

below weekly chart). This could be just a sharp pullback within a continuing

bull market, but if support at 141 is decisively breached then the probability

that a major peak is already in place will increase substantially.

As discussed in the 23rd June Weekly

Update, from a cyclical perspective the most likely time for a major low

in US bond yields (a major high in US bond prices) is October of this year.

However, if the JGBs have peaked then there isn't much chance that US bonds

will exceed last month's high. As such, we will consider a weekly close

below 141 in the JGB futures to be a clear sign that a major peak for US

bonds is behind us.

On a slightly different topic, we will

need to see how bonds behave in parallel with significant stock market

weakness to know whether the inverse relationship between stocks and bonds

that has characterised the past 5 years is still in effect. Over the past

3 months we've seen stocks and bonds rally in parallel, but we are yet

to see any meaningful concurrent declines.

Gold and

the Dollar

Currency Market Update

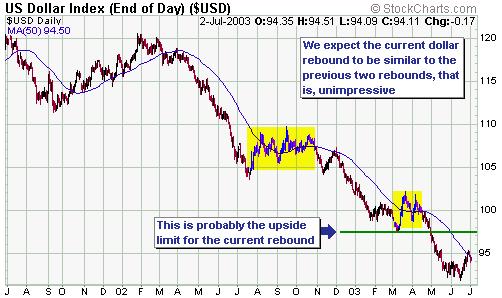

We expect the Dollar's rebound to continue

over the next month or so, but as discussed in recent commentaries we don't

think the upside potential is great. In fact, in all likelihood the current

rebound will be similar in magnitude to the rebounds that occurred during

July-October of last year and March-April of this year. This means that

the Dollar probably has about 2-3% of upside potential from yesterday's

closing level.

Below is a chart of the Yen covering

the past 3 years. The Yen has major resistance at around 86-87 and every

time it approaches this resistance the Bank of Japan jumps into the market

and buys enough dollars to ensure that a breakout does not occur. It is

always dangerous to bet against the ability of any central bank to depreciate

its currency because the one thing that central banks are good at is currency

depreciation, but in this case the upward pressure under the Yen as a result

of natural market forces is huge. Not only do the Yen bulls have the fundamentally

weak Dollar in their favour, there is a significant probability that the

Japanese stock market made a long-term bottom earlier this year. As such,

the Yen is likely to benefit from capital repatriation as well as new foreign

investment over the coming months.

We expect the Yen to overcome the BOJ

intervention and break above the 86-87 level before the end of this year.

A reasonable upside target for the Yen over the next 12 months is 100 Yen

to the Dollar (about 15% above the current level).

Gold and Gold Stocks

From the latest Weekly Update: "Over

the past few weeks we've mentioned the $340-$345 range as a likely short-term

downside objective for August gold futures. Gold traded down to this level

last Thursday, so there is a reasonable chance that a short-term low is

in place. Lower levels are, however, probably going to be reached before

the next major advance gets underway. As previously advised, two consecutive

daily closes in the gold price above its 18-day moving average will warn

us that the short-term trend has turned higher."

The rebound in the gold price over

the past few days confirms that a short-term low was, indeed, put in place

last Thursday. As the below chart shows, gold has now traded back up to

resistance defined by the 18-day moving average, the 50-day moving average

and the short-term channel, so the short-term upside potential from here

is minimal IF we were correct when we stated that lower levels would be

reached before the next major advance gets underway.

Regardless of what happens in the short-term,

the upside breakout in the NEM stock price in early June (see chart below)

supports our view that gold and gold stocks are headed much higher before

the end of this year. We expect NEM to trade up to $50 within the next

12 months, although we are not interested in buying the stock because the

type of financial market environment in which NEM would gain 50% from its

current level would result in most of our junior gold stocks experiencing

much greater percentage gains. If gold and gold stocks pullback over the

next few months then NEM could drop all the way back to around $26-$27

without doing significant damage to the technical picture, although it

is more likely that support at around $30 will contain any pullbacks.

Looking for investment-grade buying

opportunities amongst the juniors

In last week's Interim Update we included

a valuation comparison of junior gold stocks and mentioned that NovaGold

Resources (TSX: NRI) was the one stock covered in our comparison table

that currently wasn't in the TSI Stocks List and that we would add to the

List if we weren't already overloaded with gold stocks. Overloaded or not,

having done some more research on NRI we are going to add the stock to

the List now. The below review of NRI explains why.

First, some introductory information.

Historically, markets have valued exploration/development

stage companies based on the stage of advancement of their projects to

production and/or the likelihood of a takeover prior to production. For

North American based companies the average adjusted market cap (market

cap plus debt minus cash) per ounce of the total MI&I (measured, indicated

and inferred) resource for a producing company is a little more than $100/oz.

At the Feasibility stage it is typically $30-50/oz, at the Pre-Feasibility

stage it is around $20 per ounce, and at the resource definition stage

post discovery it is typically $5-10 per resource oz. These values appear

to reflect the market discount that the project will make it to production,

that is, Feasibility-stage ounces attract a 50% discount to a production

valuation, Pre-Feasibility ounces a 50% discount to the Feasibility level,

etc. Takeovers such as Francisco Gold by Glamis have tended to be somewhere

between Feasibility and production valuation levels on a per resource ounce

basis.

Using this approach a systematic progression

is seen in increased value as a project goes from initial discovery and

resource definition to eventual production or takeover. In fact, based

on this approach there is potentially as much increase in value from the

resource definition to production stage as there is in the initial discovery

phase but with a much higher likelihood for success and therefore lower

risk since a gold deposit has already been found. Depending on how many

shares a company will need to issue to progress their project from stage

to stage this could represent as much as a doubling in share price at each

development milestone.

With the above in mind, let's now take

a look at NovaGold.

Below is a chart that shows the estimated

stock price of NRI at various stages of development assuming a) a gold

price of $325, and b) that NRI will need to issue an additional 10M shares

to fund its portion of the Donlin creek construction costs. The black vertical

line indicates the current amount of NRI's total gold resource (assuming

NRI ends up owning 30% of the Donlin Creek project), so the point on the

left-hand scale corresponding to the intersection of the black vertical

line with one of the coloured lines shows what the NRI stock price will

potentially be at a particular stage of development.

The current development schedule for

the Donlin Creek Joint Venture is to complete the Pre-Feasibility Study

in Q4 2003. Therefore, the above chart suggests that a reasonable value

for NRI at the end of this year would be US$5/share (C$6.60/share) assuming

the current schedule is achieved and a gold price of $325/ounce. In other

words, there appears to be substantial upside potential in NRI over the

next 6 months even if the gold price does not rise. Another way

to look at the situation is that there is a substantial margin of safety

built into NRI's current stock price.

The Feasibility definition drilling

is scheduled to be completed during 2004 with the Feasibility Study anticipated

to be complete in late 2004. Final permitting and design work would be

targeted to begin in early 2005 with a construction decision no later than

2007 (most likely in 2006) for Placer Dome to earn its additional 40% in

the project. Due to the size of the mine, construction will likely take

12 or more months with first gold production coming in 2007 or 2008. Total

gold production is currently anticipated to be 1.0 to 1.2 million ounces

per year with NovaGold's share of production anticipated at 300,000 to

400,000 ounces per year.

Note that under the joint venture agreement

between Placer Dome and NovaGold, Placer will finance the project from

now until the point where a construction decision is made. In fact, NRI's

involvement in Donlin over the next 2-3 years should be minimal, enabling

the company to focus on its other projects.

Speaking of other projects, prior to

Donlin Creek coming on stream NovaGold will be advancing its two wholly

owned projects in Nome, Alaska to production decisions. At the Rock Creek

Project the 1.1 million ounce deposit is anticipated to produce 100,000

ounces per year from an open-pit operation. An independent Scoping Study

is expected by mid-summer 2003 with on-going feasibility drilling through

the fall. A revised resource estimate is expected after final assays are

complete late in 2003. The Feasibility Study is anticipated to be complete

by mid-2004 with a production decision shortly thereafter. Permitting would

likely take 12 months or less, so construction could then begin in mid-2005

with the first gold production in late 2005.

Concurrently, NRI is reviewing restarting

gold production on its Nome Gold Project. The deposit hosts 2.3 million

ounces of gold that is anticipated to begin production at 50,000 ounces

per year with by-product sand-and-gravel production. The project would

be very scalable with increased production easily added. An independent

engineering evaluation is currently underway with results anticipated to

be ready by fall 2003. With positive initial results Feasibility engineering

work could be completed in early 2004. A Production decision, final permitting

and construction could then be possible by late 2004 or early 2005.

NovaGold is also working with TNR Gold

on the 1 million ounce Shotgun project south of Donlin Creek to expand

the current resource and target the potential for a multi-million ounce

Donlin Creek type system.

A lot of junior gold companies have

great potential, particularly given the very bullish outlook for the gold

price, but they are too risky to be considered 'investment grade' (an investment

grade opportunity is one where the upside potential is good and

where the downside risk is sufficiently low that making a sizeable commitment

is feasible). Companies that have yet to establish a proven resource base

are especially risky. Such companies sometimes provide their owners with

spectacular profits, but the risk of failure is so high that they are only

ever suitable for small speculations. Near its current price NRI, in our

view, represents an investment-grade opportunity.

Update

on Stock Selections

The

Feasibility Study(FS) for Desert Sun's Jacobina gold project in Brazil

is due to be complete by mid August. If the current FS confirms the resources

and reserves that were previously established for this project then Desert

Sun (TSXV: DSM) is dramatically under-valued at its current stock price.

For example, using the US$30/ounce figure mentioned in the NRI discussion

above for Feasibility-stage resource ounces, the 3M ounces at Jacobina

would be worth around US$90M (C$120M) assuming a successful outcome for

the FS. DSM's fully-diluted share count is 36M, so this suggests a potential

stock price of C$3.30 following completion of the FS. There is more risk

associated with Brazil than North America, but a stock price in excess

of C$2.00 certainly seems reasonable for DSM over the next several months

assuming no increase in the gold price. The

Feasibility Study(FS) for Desert Sun's Jacobina gold project in Brazil

is due to be complete by mid August. If the current FS confirms the resources

and reserves that were previously established for this project then Desert

Sun (TSXV: DSM) is dramatically under-valued at its current stock price.

For example, using the US$30/ounce figure mentioned in the NRI discussion

above for Feasibility-stage resource ounces, the 3M ounces at Jacobina

would be worth around US$90M (C$120M) assuming a successful outcome for

the FS. DSM's fully-diluted share count is 36M, so this suggests a potential

stock price of C$3.30 following completion of the FS. There is more risk

associated with Brazil than North America, but a stock price in excess

of C$2.00 certainly seems reasonable for DSM over the next several months

assuming no increase in the gold price.

One

of the most under-valued gold stocks at the present time is Northgate Exploration

(TSX: NGX). In fact, the market appears to be assigning almost no value

to NGX's 6.6M ounce Kemess North resource (Kemess North is currently in

the pre-feasibility stage). We have no idea what the NGX stock price is

going to do in the short-term, but expect NGX to be one of the best-performing

mid-tier gold producers over the next 12 months.

NovaGold

Resources (TSX: NRI) will be added to the Stocks List using yesterday's

closing price of C$3.25 for record purposes.

In

May we said we would add International Paper (NYSE: IP) to the Stocks List

if it traded down to around $34 (a level that roughly corresponds to the

uptrend-line shown on the below chart). IP is a company that stands to

benefit from the on-going inflation and US$ weakness, so a long position

in this stock is consistent with our overall thesis. IP hasn't yet pulled

back to its ideal 'buy level', but we are going to add it to the List now

because the risk/reward looks attractive. We'll place an initial sell stop

at $30.90 (just below the October-2002 low).

Not

all the stocks in the TSI Stocks List are a 'buy' at any given time. However,

if a stock is in the List then it was considered to be a 'buy' when it

was added and is certainly still considered to be a 'hold' (note that when

we say hold we really do mean hold, unlike in 'Wall St speak' where a hold

recommendation means 'get out now because the stock price is about to plummet').

What we have been doing over the past

few months, and will continue to do, is point out when one of our favourite

stocks has dropped to a level where we think new buying is appropriate.

For example, over the past 3 months we've mentioned DSM on 2 or 3 occasions

when its price dropped to support in the C$0.80-0.85 range, WTC when it

was trading in the C$2.70-3.00 range, the Wheaton River warrants on at

least 3 occasions when they were trading in the C$0.50-0.57 range, GPXM

at US$0.23 and then at 0.28, AQI initially at C$0.26 and then in the 0.30-0.40

range, CBD below C$2.50, and NRI at C$2.95 last week. In general, our goal

is to buy stocks in a bull market (in this case gold stocks) after they

pullback to near important support and to avoid chasing stocks after they've

broken out to the upside.

As an aside, at the current time it

is dangerous to trade the junior gold stocks with the aim of sidestepping

the normal pullbacks in the market because the upside risks are so much

greater than the downside risks. For example, all of the stocks in the

TSI List are either fairly valued or under-valued assuming a gold price

of $325, so there is no speculative excess built into their prices. As

such, although we think the odds favour a pullback into August anyone who

sells these stocks with the aim of buying back at a lower price over the

next few months is taking what we think is an unnecessary risk.

If

your equity-market portfolio has been constructed roughly in line with

what has been suggested at TSI, then you would:

a) Be long the Japanese stock market

via an index fund such as EWJ

b) Be long a couple of commodity-oriented

stocks

c) Have a large long position in the

gold sector with particular emphasis on the junior gold stocks (you would

own at least 7 junior gold stocks)

d) Be out of the stock market apart

from the specific areas mentioned above

e) If you happen to be an experienced

options trader, have a small bearish position on the US stock market via

some put options

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.futuresource.com/

|