![]()

![]()

![]()

![]()

- Interim Update 2nd September 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The August-2020 Monthly

Closing Prices

Today we will review monthly

charts for gold, the HUI, the S&P500 Index (SPX), the Dollar Index and the

Australian dollar, starting with gold.

In last month's review of

monthly closing prices, we wrote:

"...the US$ gold price ended

the month of July-2020 above its 2011 high. This means that there is

nothing but blue sky above the current price, but it doesn't ensure that

the market will continue along its recent upward path. A downward

correction in the gold price should accompany the next meaningful upward

correction in the Dollar Index, which looks set to get underway soon."

A meaningful upward correction in the Dollar Index (DX) didn't get

underway in August, but a downward correction in the gold price may have

commenced early in the month following a spike up to around US$2100.

The following monthly chart shows that during August the US$ gold

price traded well above and well below its July-2020 close before ending

the month with a small net loss. This sort of price action after a strong

rally can mark a top. As discussed in recent TSI commentaries, a

multi-month top would be confirmed by a weekly close below US$1920.

As mentioned in previous discussions of monthly prices, critical

monthly-closing support for gold's intermediate-term upward trend is

defined by the 8-month MA (the black line on the following chart). That

is, a monthly close below the 8-month MA would indicate that a top that

holds for more than a few months is in place. This MA continues to rise

and should be near $1800 a month from now.

Ideally (from a

long-term bull's perspective) there will be a test of or an intra-month

spike below the 8-month MA, but not a monthly close below the 8-month MA,

at some point over the next two months as part of a 'corrective' process.

The next monthly chart shows that the HUI's performance during August

was similar to gold's, except that the HUI ended the month with a small

net gain. The implication is the same, in that the upward spike in

early-August potentially marked a multi-month top.

A correction

within the next two months could take the HUI down to the mid-200s and

could even test the 21-month MA (the blue line on the following chart),

but despite this short-term risk the intermediate-term risk/reward remains

very bullish.

The US stock market's post-crash rebound continued in August and the

SPX just achieved a monthly close above its February-2020 high. This means

that for the SPX the Q1-2020 crash was an intermediate-term bull-market

correction rather than the first leg of a bear market. However, broader

indices that are not dominated by a handful of mega-cap tech stocks are

well below their all-time highs, so the overall market's long-term trend

is not clear.

The summary of our 1-2 year outlook included in each

of our past two discussions of monthly closing prices still applies. Here

it is again: We think that the March-2020 low will NOT be tested over the

remainder of this year or the first half of next year, but that it will be

tested in parallel with another recession during 2022.

By early-June we were confident that the US$ had made a long-term top,

but it wasn't until 31st July that almost all remaining doubt was removed

via a monthly close by the Dollar Index (DX) below its March-2020 low.

It is highly probable that the DX is about 5 months into a 1-2 year

downward trend, but there will, of course, be significant rebounds on the

way to much lower levels. It looks like such a rebound is about to begin.

The coming DX rebound could be strong, but assuming it's a

countertrend move it shouldn't achieve a monthly close above the 20-month

MA (the blue line on the following chart).

The Australian dollar (A$) has managed five big consecutive up-months

since bottoming in March-2020. Over the past 15 years, the only other time

it has done anything like this was in the early part of the 2.5-year

cyclical bull market of 2009-2011. Therefore, it's fair to say that the

price action remains consistent with our view that the A$ commenced a

cyclical bull market in March-2020.

From here on, significant

corrections in the A$ probably will be limited by the 20-month MA (the

blue line on the following chart). It's likely that the A$ will experience

such a correction in parallel with the next meaningful stock market

decline.

By the way, our outlook for the Canadian dollar (C$) is

similar to our outlook for the A$, although we expect the C$ to

underperform the A$ over the coming two years. The main reason is that the

C$ tends to be weak relative to the A$ during multi-year periods when the

Dollar Index is weak. This is probably because of the closeness of the

Canada and US economies.

The shortest US

recession ever, update

Three months ago we wrote that

the National Bureau of Economic Research (NBER), the official arbiter of

US recessions, could determine that the 2020 recession was over by July,

making it the shortest US recession ever. We also wrote that there was so

much 'rot' in the economic foundations that the US economy would recover

only 80%-90% of what it lost during the first half of this year before

turning back down. Two months ago we wrote that the spectacular rise in

the ISM New Orders Index (NOI) suggested that the recession actually ended

in June, a view that was reiterated a month ago.

The latest NOI was

published on Monday of this week and there is now almost no doubt that the

recession ended in June. As shown below, the NOI continued its rapid rise

in August and has reached its third highest level of the past 20 years.

The rise in the NOI to its third highest level in 20 years doesn't

imply that the US economy is now very strong. It indicates that a

substantial majority of the purchasing managers who are surveyed by the

ISM are seeing improvement in order flow. This means that it indicates

widespread improvement from a very low level as opposed to widespread

strength. That being said, the lead-lag relationship between the ISM NOI

and Industrial Production (IP) suggests that a strong recovery in IP will

be underway by the first quarter of next year.

The continuing surge

in the ISM NOI is bullish for industrial commodities and bearish for gold

and T-Bonds. This is consistent with our view that the industrial metals

will outperform gold over the coming 6-12 months, or, to put it more

accurately, that the industrial metals will continue to outperform gold

for another 6-12 months (gold peaked relative to the Industrial Metals

Index (GYX) in April). However, beyond the next 12 months we are more

bullish on gold, because the problems caused by this year's efforts to

prop-up the economy and asset prices should ensure that the US economy

slumps back into official recession territory during 2022.

The Stock Market

Current Market Situation

The "implied" volatility measured by the VIX, that is, the volatility

implied by options prices, has risen over the past several days.

However, rarely has actual price volatility been lower. As illustrated

below, the Russell2000 ETF (IWM) has worked its way upward at a slow pace

along its 20-day MA over the past 8 trading days and has spent the past 18

trading days within a 3% range.

There are no signs of trouble except for the market's bad breadth, but

the bad breadth is potentially important. We are referring to the fact

that the bulk of the recent upside in the highest-profile stock indices is

due to strength in a small number of mega-cap stocks.

The breadth

issue is evidenced by the following comparison between the SPX and the

NYSE Advance-Decline Line (ADL). Specifically, by the fact that the SPX

has moved well into new-high territory over the past two weeks while the

ADL has remained well below its early-August high.

The bearish

divergence between the SPX and the ADL could be eliminated over the weeks

ahead via a broadening-out of the rally, which probably would be of

greatest benefit to commodity-related equities. However, it also could be

eliminated by a sizable correction in the SPX. Our 'core' exposure

positions us for the former possibility and we have used options to hedge

against the latter possibility.

The short-term risk is substantial and increases with every new high

in the senior stock indices, but there is no reason that the relentless

rise can't continue for a few more weeks.

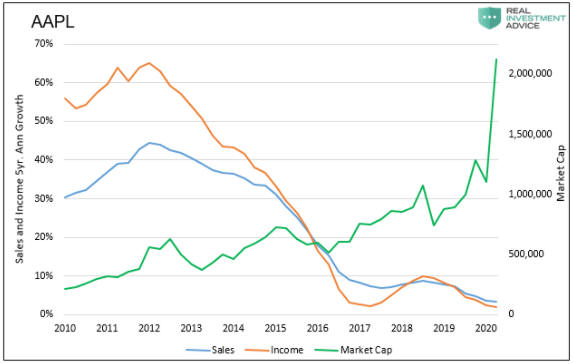

Apple Mania

The following chart from the article posted

HERE does an excellent job of illustrating the absurdity of Apple's

stock-price performance over the past several months. The chart shows that

Apple's sales and income have barely grown at all over the past 5 years

while the company's market capitalisation has exploded.

Gold and the Dollar

Gold and Silver

In the latest Weekly Update, we wrote:

"We continue to

think that a multi-month top for the US$ gold price was set in

early-August, but a weekly close below US$1920 is required to confirm this

view. Also, even if a multi-month top is in place, as part of a topping

process there could be a rise to the mid-US$2000s within the coming

fortnight. This would be signalled by a daily close above the 20-day MA."

The short-term chart pattern didn't change over the first three days

of this week. The gold price spiked up to $2000 on Tuesday but didn't

manage to close above its 20-day MA. On Wednesday the price fell by almost

2% but held above support at $1920.

So, it still looks like a

multi-month top was set in early-August and there is still a chance,

albeit a diminishing one, of a rise to the mid-US$2000s within the coming

1-2 weeks as part of a topping process.

At this stage we think that

October is the most likely time for a short-term price low and the

resumption of the longer-term upward trend.

Regarding silver, here's what we wrote in the latest Weekly Update:

"A daily close by silver below its 20-day MA would be a

preliminary signal that the next meaningful decline has begun, while a

daily close below short-term lateral support at US$26.00 would be a more

conclusive signal.

Once the start of a decline is signalled as

outlined above, the 200-day MA will become a reasonable target for a

correction low. This MA should be at or above US$19.00 during October,

which is the most likely month for a correction low."

Despite

a 4.4% decline in Wednesday 2nd September, the US$ silver price held above

its 20-day MA on a daily closing basis (by the slimmest of margins).

Therefore, nothing has changed.

If a) you have substantial exposure to gold and silver bullion and/or

the associated mining stocks and b) you are experienced with options

trading, then you could hedge your exposure via GLD and/or SLV and/or GDX

put options expiring in October or later. FYI, we have been accumulating

SLV $23 put options and GLD $170 put options expiring on 16th October

2020.

Gold Stocks

Since the end of last

week there has been a net change of only 2 points in the HUI and there

have been no big price swings, so the situation is unchanged. It's still

the case that the most likely direction of a sustained breakout from the

trading range of the past month is down, as this would be consistent with

the August-September cycle and the strong potential for a US$ rebound.

However, it's also still the case that a short-term inflationary blow-off

cannot be ruled out.

The Currency Market

We sent an email to

subscribers after the close of US trading on Monday 31st August. The main

purpose of the email was to confirm that, for TSI record purposes, profits

were being taken on the Taseko Mines (TGB) position, but we also wrote:

"This is a critical short-term juncture in the financial world

because we are about to get either a downside breakout or an upward

reversal in the Dollar Index (DX). It's a good bet that the former would

lead to upward acceleration in the prices that have been trending higher

over the past few months, while the latter would usher-in significant

corrections in the markets that have rallied over the past few months. We

think it's important to be hedged against the latter possibility while

maintaining core exposure in line with the US dollar's cyclical bearish

trend."

On Monday the DX closed exactly at its mid-August low

of 92.1, which also was its low for the year. On Tuesday the DX traded at

a new low for the year and then reversed course to end the day with a

small gain. It gained additional ground on Wednesday.

The price

action of the past two days is very preliminary evidence of a reversal in

the DX's short-term trend from down to up. A daily close above 93.5 would

generate more conclusive evidence and a daily close above 94 would leave

little room for doubt that a short-term bottom (a bottom that holds for

1-3 months) is in place.

If the DX's short-term trend has reversed,

then within the next three months it should trade at least as high as

95.5-96.0 and could rise as far as resistance at 97.5-98.0.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

![]()