![]()

![]()

![]()

![]()

- Interim Update 3rd January 2018

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Happy New Year!

I wish you the very best of luck

in 2018 and thank you for supporting TSI.

US Recession

Watch

The latest iteration of the

monthly ISM Manufacturing New Orders Index (NOI) was reported on Wednesday

3rd January. The NOI is one the three leading indicators of US recession

that we care about, the others being Real Gross Private Domestic

Investment (RGPDI) and the yield curve.

The following chart shows

that the NOI rose sharply to a 14-year high in December-2017.

Based on the overarching message from our favourite leading

indicators, over the past three months our conclusion was that there would

be no US recession until Q2-2018 or later. That's still our general

conclusion, although in response to recent developments we can be a little

more specific.

Taking into account the NOI surge (bullish), the

fact that the yield curve is still in a flattening trend (bullish) and the

decline in the monetary inflation rate (bearish), we think that:

a)

The probability that a US recession will start in Q1-2018 is 0%.

b)

The probability that a US recession will start in Q2-2018 is 10%.

c) The probability that a US recession will start in Q3-2018 is 30%.

d) The probability that a US recession will start in Q4-2018 is 50%.

Apart from the 0% probability for Q1, it's likely that the percentages

mentioned above will change as new information becomes available.

The Stock Market

Low volatility across

the financial world

Stock market volatility in the US

wasn't just low last year, it was the lowest since the birth of the

current monetary system in 1971. This is evidenced by the unprecedented

amount of time spent by the VIX below 10. It is also evidenced by these

interesting facts:

a) The SPX's average daily change in 2017 was

the smallest since 1964.

b) Although the SPX enjoyed a substantial

(22%) rise over the course of 2017 there wasn't a single trading day with

an SPX gain of more than 1.4%.

c) On a daily closing basis the SPX

has not experienced a correction with a peak-to-trough decline of more

than 3% since November of 2016. Never before has there been such a long

stretch without a decline of more than 3%.

Furthermore, the absence

of volatility wasn't restricted to the stock market. As illustrated by the

following two charts, it spread across the financial world.

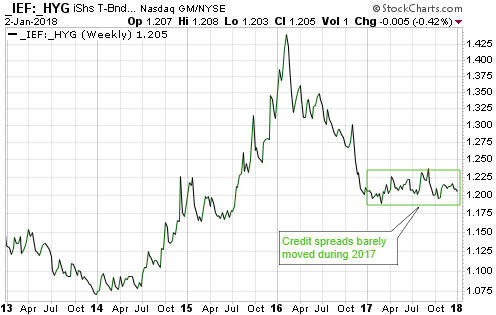

The

first chart shows that the IEF/HYG ratio, a credit-spread indicator, moved

sideways within a narrow range throughout 2017. Considering the economic

and financial-market instability caused by today's monetary system, such

performance is highly unusual.

The second chart shows the

reciprocal of the iShares TIPS Bond Fund (TIP), an indicator of what's

happening to real interest rates. This indicator was choppy within a

horizontal range during the whole of 2017 and essentially flat-lined

during the final quarter of the year.

The credit spread and the

real interest rate are inputs to our gold and our equity

fundamentals-focused models. The choppy sideways movement of these inputs

is the main reason that our models have 'whipsawed' over the recent past.

From our perspective, the lack of volatility was one of last year's

biggest surprises. A repeat performance would be an even bigger surprise.

Current Market Situation

At no time over the

past 12 months did it seem that an end to the long-term equity bull market

was imminent. That's still the case, because financial-system leverage is

still on the rise. However, there were a few occasions over the past year

when we thought that a bearish speculation, in anticipation of a 10%+

correction, was appropriate. None of these speculations worked.

Humbled but not daunted by last year's failures we are now interested in

positioning ourselves for a meaningful downward correction during the

first quarter of this year. In fact, the lack of a correction worthy of

the name and the almost total absence of volatility during 2017 make it

even more likely that 2018 will contain greater-than-average two-way

volatility in the US stock market, beginning in Q1.

In the Weekly

Update posted on Sunday we wrote that ideally the NDX would surge to a new

high during the first week of the New Year to create the opportunity we

seek to get positioned in QQQ April-2018 $150 puts. We also wrote that for

those who prefer to avoid options trading it could make sense to average

into a QID (ProShares UltraShort QQQ) trading position.

The

following chart shows that a start-of-the-year surge to a new high has

happened. This, of course, doesn't mean that the market is close to even a

short-term top, but we argue that it reduces the risk of speculating

bearishly by potentially completing a short-term pattern that did not

appear to be complete at the end of December.

For our own account an initial position in the aforementioned puts was

taken on Wednesday 3rd January, as much to hedge our exposure to non-gold

stocks* as to bet on an NDX decline. However, we won't add a new bearish

speculation to the TSI List until there is a downward reversal in the

market, because at that time risk management will become more

straightforward. Specifically, after a downward reversal has happened it

will be possible to limit the risk of loss by placing a protective stop

slightly above the recent high.

*Gold

stocks are more likely to be helped than hurt by a sizable correction in

the broad stock market.

Gold and the Dollar

Gold

The

US$ gold price has risen for 9 days in a row and on 13 of the past 14

days. Needless to say, the market is 'overbought' on a short-term basis.

A routine 1-2 week correction should begin soon. It's possible that

former resistance at $1300 will act as a floor during the coming

correction, but a pullback to as far as the 50-day MA would be normal. As

indicated by the following chart, the 50-day MA is in the high-$1270s. It

is also rising and will soon be above $1280.

Silver

Like the US$ gold price, the US$ silver

price has moved upward in almost a straight line over the past 3 weeks.

The difference is that whereas the US$ gold price has broken above its

October-November highs, the US$ silver price has not yet reached

resistance defined by these highs.

Silver has short-term resistance

in the $17.25-$17.50 range. A test of this resistance followed by a

pullback to around $16.50 would set the stage for a move up to the more

important resistance at $18.00-$18.50.

Gold Stocks

On Tuesday of this week the HUI

became the last of the gold-mining indices and ETFs to break above the

200-day MA. It then pulled back on Wednesday while holding its breakout.

However, the break above the 200-day MA has occurred with the market

stretched to the upside on a short-term basis. Therefore, it probably

won't be sustained. Instead, it's reasonable to expect that a correction

over the coming 1-2 weeks will take the HUI back below its 200-day MA and

down to the vicinity of its 50-day MA (the blue line on the following

chart).

There has not yet been sufficient strength in the HUI/gold

ratio to suggest that an intermediate-term rally is underway, but even if

it isn't the gold-mining sector probably will move above this week's high

after some 'corrective' activity. In other words, the rally from the

December low is probably about to pause for breath, not come to an end.

The Currency Market

Oil, the Yuan and the dollar-based monetary system

Some

commentators have made a big deal over the Yuan-denominated oil futures

contract that will soon begin trading in Shanghai, but in terms of effect

on the global currency market this appears to be a very small deal.

With or without a Yuan-denominated oil futures market there is nothing

preventing the suppliers of oil to China from accepting payment in Yuan.

In fact, some of the oil imported by China is already paid for in Yuan.

Having a Yuan-denominated oil futures contract may encourage some

additional oil trading to be done in China's currency because it would

enable suppliers to reduce their risk via hedging, but the main issue is

that the Yuan is not a useful currency outside China. Unless an

international oil exporter was interested in making a large investment in

China, getting paid in Yuan would create a problem of what to do with the

Yuan.

In any case, the monetary value of the world's daily oil

consumption is less than 0.1% of daily trading volume on the foreign

exchange market, and the foreign exchange market is dominated by the US$.

Despite the popular (in some quarters) notion that the US$ is in danger of

losing its leading role within the monetary system, at last count the US$

was on one side of 88% of all international transactions. The euro, the

world's other senior fiat currency, was at around 30% (and falling). The

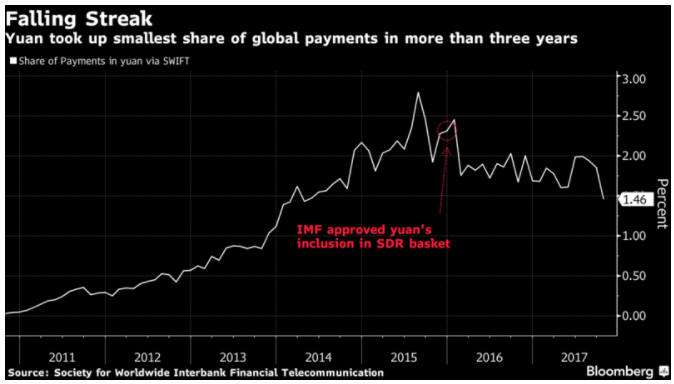

Yuan's share of the global currency market is very small (less than 3%),

and according to the following chart could be in a declining trend.

The point we were trying to make in the above paragraph is that a

change in how any country pays for its oil imports will not have a big

effect on the global currency market. Actually, the cause-effect works the

other way around. The pricing of oil in US dollars is not, or at least is

no longer, even a small part of the reason that the US$ dominates the

global currency system, but the fact that the US$ dominates the global

currency system causes most international oil exporters to demand payment

in US dollars.

The US$ sometimes rises and sometimes falls in value

relative to other currencies, but it always dominates global money flows.

Like it or not, that's the nature of today's monetary system.

The

current monetary system is US$-based and in all likelihood will remain so

until it collapses and gets replaced by something different. In other

words, it's unlikely -- we almost would go as far as to say impossible --

for the current system to persist while another currency gradually

superseded the US$. The reason is that there is no viable alternative to

the US$ among today's other major fiat currencies.

We don't have a

strong opinion on what the post-collapse "something different" will be.

One possibility is a system based on gold, but there could also be an

attempt to create a global fiat currency. The world's political leadership

and financial establishment would certainly favour the latter possibility,

but we fail to see how it could work as it would essentially be the

botched euro experiment on a much grander scale.

Current Market Situation

The euro

broke out to the downside in late-October, but in early-November it

reversed course and began to trend upward. This painted the downside

breakout as false.

Over the first two trading days of the New Year

it returned to its September peak before pulling back a little. A 1-2 week

consolidation is likely and would reduce the probability of a false upside

breakout.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.bloomberg.com/

![]()