|

- Interim Update 3rd March 2004

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The problem

with Fannie and Freddie

In a recent speech Alan Greenspan expressed

concern about the way Fannie Mae and Freddie Mac are taking advantage of

an implied government guarantee to expand their balance sheets at a phenomenal

pace. According to Greenspan, the ability of these Government Sponsored

Enterprises (GSEs) to borrow money at below the market rate is allowing

them to rapidly increase their size and power without providing any significant

benefits to homebuyers.

In our opinion, it is more than a little

disingenuous of Greenspan to call for the GSEs to be 'reined in' because

the GSEs have been the main vehicles via which Fed monetary policy has

been implemented over the past several years. In particular, the balance

sheet expansion of the GSEs has been the main engine of money-supply growth

(inflation).

The Fed relies on institutions such

as Fannie and Freddie because the Fed, itself, makes almost no direct contribution

to money supply growth. For example, when the total supply of money (M3)

increases it is not because the Fed has printed more money, it is because

the total amount of debt has increased; and the biggest facilitators of

US$ debt creation over the past six years have been the GSEs.

So, given how helpful the GSEs have

been in furthering the Fed's inflation agenda why is Greenspan now expressing

concerns about their growth?

We can think of a few possible reasons,

one being that Greenspan wants to have more control over WHEN the GSEs

ramp-up their balance sheets rather than just having them expand at the

fastest possible rate at all times. After all, there is going to come a

time when the Fed will want to temporarily STOP promoting credit expansion.

Another is that Greenspan is not really interested in doing anything

to restrict the GSEs but wants to make sure he is on the record as having

provided a timely warning at that point in future when a major problem

occurs. A third possibility is that Greenspan is genuinely concerned about

one or more of the GSEs becoming insolvent due to a sharp rise in interest

rates and is paving the way for some preemptive action.

The GSEs' extensive use of derivatives

to manage their interest-rate exposure gets a lot of press, but we doubt

that derivatives will turn out to be the biggest problem. Instead, if Greenspan

is genuinely concerned about the GSEs' ability to cope with higher interest

rates it is most likely because their assets -- the mortgages and other

debt instruments they hold on their balance sheets -- are huge in relation

to their shareholders' equity and their provisions for losses. For example,

about six months ago we read that Fannie Mae had about $1 of loss reserves

for every $2,500 of its business exposure. Fannie's management justifies

such a small loss reserve on the basis that credit-related losses over

the past few years have been very small. The thing is, the losses have

only been small because interest rates have been trending lower and credit

has been expanding at a rapid clip. However, if the monetary backdrop changes,

as eventually it must, then these loss reserves are going to be woefully

inadequate.

In any case, regardless of whether

or not Greenspan means what he says when he expresses concern about the

GSEs' growth it is extremely unlikely that any restraints will be placed

on the GSEs over the remainder of this year. This is an election year,

after all.

The US

Stock Market

The Primary Trend

Is the stock market immersed in a secular

bear market? Possibly (a good argument can certainly be made that it is),

but not definitely. If a secular bear market in US equities did commence

during 1998-2000 then it appears to be proceeding in a similar way to either

the secular bear of 1966-1982 or the long-term bear market in Japan that

started in 1990 and perhaps ended last year.

The other possibility that we've addressed

at TSI over the past year is that a secular bear market has not started

yet. Based on the performance of the advance-decline line over the past

4 years and the new all-time highs recently achieved by several important

market sectors, a good argument can also be made that this is the case.

What we do NOT think is possible is

that a major bear market ENDED at the October-2002 lows. There are a number

of reasons for this, including:

a) Bear markets are all about washing

away the excesses built-up during the preceding bull market, but many of

the excesses in the stock market and the economy were not eliminated during

the 2000-2002 downturn. In fact, the US credit bubble grew at a rapid rate

during this period and valuation levels have generally remained high.

b) Major bottoms occur after the public's

expectations of future returns become depressed, but during the final quarter

of 2002 the public was still anticipating above-average long-term returns

from the stock market (this, of course, is related to the persistently

high valuations).

c) You don't correct an 18-year bull

market with a 3-year bear market.

As far as most of our TSI recommendations

as well as our own trading/investing are concerned, though, it doesn't

make any difference whether a secular bear market has or hasn't begun because

the normal time frame for any trades we make/recommend is 3-12 months;

and during any 3-12 month period it is not unusual for the market to move

counter to its secular trend. Furthermore, this is particularly the case

when the secular trend is down.

As an aside, our readers would be well

advised to keep the above-mentioned time frame in mind when reading the

TSI commentaries and acting on any recommendation we make. In some cases

we'll note that a particular investment is suitable as a long-term (> 1

year) play and in other cases we might specifically mention something as

a short-term (0-3 month) trade, but our main objective is to catch large

swings in the markets that unfurl over 3-12 month periods. As such, although

we regularly make comments on what we see happening over the coming few

weeks the daily and weekly fluctuations in the markets are of little interest

to us except when these fluctuations are significant enough to affect our

longer-term views.

Current Market Situation

One of the challenges, at the moment,

is that there are more than the usual number of mixed signals. For example,

it looks like the S&P500 Index is immersed in a bullish consolidation

and that it is just a matter of time before we get a surge to new recovery

highs.

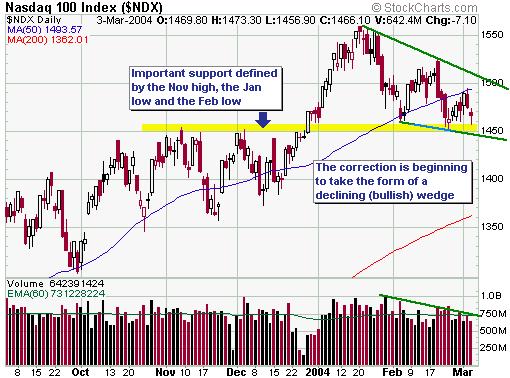

The NASDAQ100 Index, however, has been

considerably weaker, although important support held last week and the

pullback has recently started to look more like a declining wedge than

something more sinister.

The short-term technical outlook for

the NASDAQ100 Index might have improved a bit over the past week but the

price action of Intel (NASDAQ: INTC) -- the world's largest semiconductor

company and probably the most important tech stock in the world at the

present time -- looks quite bearish. In particular: INTC broke below support

at the beginning of last week, rebounded back to that former support range

(now resistance) and then reversed lower.

Note, though, that Intel is scheduled

to give a mid-quarter business update after the market closes on Thursday

so things could change a lot between now and the end of the week depending

on what Intel's management has to say. A close above $30 at the end of

the week would, for example, suggest that a correction low was already

in place.

And while the stock price of Intel

has been breaking lower the stock price of Walmart (NYSE: WMT) -- a much

larger company than Intel -- has been very strong. WMT is now very close

to an important upside breakout on the 1-year chart shown below and also

on a long-term chart. In fact, a weekly close above $61 would suggest that

WMT's 4-year consolidation was over and that a major advance had begun.

Like we said: mixed signals.

Over the past couple of months our

expectation has been that there would be two peaks during the first half

of this year: a January peak followed by another -- most likely higher

-- peak during the March-May period. There is no change to this view, but

as mentioned over the past few weeks the relatively poor performance of

the NDX makes it likely that new recovery highs in the S&P500 and the

Dow over the coming months will not be confirmed by the tech-heavy NDX.

The biggest short-term risk

As mentioned in the e-mail alert sent

to subscribers on Tuesday, a big risk at the moment is the potential for

an upward spike in the oil price related, perhaps, to civil unrest in Venezuela.

The oil price has eased back over the past two days so the immediate threat

might have passed, but if something were to cause oil to move up through

long-term resistance in the $38-$40 range then there would almost certainly

be a large negative reaction in the stock market.

USPIX

We've received several e-mails over

the past two of weeks regarding the USPIX position in the TSI Stocks List

(USPIX is a fund designed to move by twice the INVERSE of the NASDAQ100

Index each day), so now is probably a good time to review our plans for

this position.

We keep stressing that the odds favour

new highs in some of the senior stock indices over the next few months,

so we are clearly not anticipating making any money from the USPIX position

in the short-term. In fact, we really don't want to make any money

out of USPIX right now because we are heavily net-LONG the market via our

gold and commodity stocks. As such, we currently consider USPIX to be a

small hedge against a much larger long position (it would help cushion

the blow if something dreadful and unexpected happened).

When we added USPIX to the Stocks List

back in December (refer to the 10th December Interim Update for details)

our thinking was that it would represent an initial position which

would be added to at the appropriate time(s) during the first half of 2004.

Our thinking has not changed.

We expect to add one or two more USPIX

positions to the TSI Stocks List over the next few months and to also scale-out

of long positions, thus giving our overall stance a far more bearish bias.

Once we add our second USPIX position we'll start following it more closely

and might employ a trailing sell-stop, but in the mean time we'd suggest

that your exposure to USPIX not be so large that you feel the need to check

its price more than once per week.

Gold and

the Dollar

Which is leading, gold or the CRB?

In commentary posted at http://goldmoney.com/en/commentary.php

James Turk argues that gold would normally be expected to lead the CRB

Index, but due to central bank management of the gold price it is presently

lagging the CRB. He concludes, therefore, that the recent surge in the

CRB Index is presaging a surge in the gold price.

Our interpretation is quite different,

however, because the following chart comparison of the gold price and the

CRB Index indicates that the current major advance in the gold price began

about 8 months before the current major advance in the CRB Index; in other

words, it is clear that gold led at the start of the bull run so it is

really quite a stretch to argue that it is now lagging. Furthermore, stock-market

action confirms gold's leadership role because when most commodity-cyclical

stocks were bottoming in October of 2002 the AMEX Gold BUGS Index had already

been in a bull market for about two years.

In our opinion there are two ways to

reasonably explain gold's recent weakness relative to the CRB Index, both

of which involve gold being in a leadership role.

One is that an important peak is already

in place in the gold market, meaning that the CRB Index will reach an important

peak of its own over the next few months. The other is that gold is experiencing

a normal correction to its upward trend and will move to new highs for

the year once the correction has run its course. In this case the gold-market

correction could be warning us to expect a significant pullback in the

CRB Index prior to a resumption of the CRB's upward trend.

The latter explanation looks more likely.

Current Market Situation

In last week's Interim Update we explained

why 118-119 looked like a reasonable downside target for the euro futures

over the coming few weeks. Furthermore, our expectations were that the

Dollar Index would move up to the 90-91 range. So, with March euro futures

trading as low as 120.5 on Wednesday and the Dollar Index hitting 90 there

isn't much additional downside risk in the euro and upside potential in

the Dollar Index if our analysis is roughly on-the-mark (as it sometimes

is).

Rather than further significant weakness

in the euro and strength in the Dollar, what will perhaps be required before

the corrective activity comes to an end is more time. Our guess

is that the euro will drop slightly below yesterday's low and the Dollar

Index will move slightly above yesterday's high at some stage over the

coming 4 weeks, but the important point is that the euro's risk/reward

now looks attractive as far as the coming 3 months are concerned.

The way we currently think this will

go -- bearing in mind that we'll make whatever adjustments we need to make

along the way to ensure that we don't get out of synch with the market

-- is that the Dollar Index will drop to a new bear-market low over the

next 3 months, but it will be trading ABOVE its current level by year-end.

In the latest recent commentaries we

mentioned that the repeated testing of support at $395 (basis the April

contract) by the gold market made it very probable that this support level

would be breached, creating a downside target of $380 (+/-$3). Support

at $395 has now given way with April gold closing below this level on each

of the past three sessions and trading as low as $388 on Wednesday.

Our view is that you might (probably

will) get the chance to buy gold a few dollars below yesterday's low within

the coming week or so, but you probably aren't going to get the chance

to buy it at considerably lower prices.

It's possible that gold will start

to move higher immediately, but we'd be skeptical of the staying power

of any rally that began from near current levels. In our opinion, gold

will have a much better chance of making it to new highs for the year if

it first cleans out more of the weak hands by dropping down to around 380.

Furthermore, if gold were to drop to around 380 while the HUI held above

its February low of 208 we would have a very clear signal that a large

advance in both the stocks and the metal was about to begin.

We've focused on the small picture

for gold over the past couple of weeks so it is now probably a good time

to step back and take another look at the longer-term picture. As such

we've included, below, a weekly chart of the gold price covering the past

three years. Note that the advance in the gold price remains orderly; however,

major moves in the gold market generally don't end with a whimper but rather

with a large upward spike.

The HUI had bounced off the 217 level

on four occasions over the past couple of weeks, making it likely that

this level was going to be breached before a secondary low was put in place

(we say a "secondary low" because we think the HUI bottomed in early February).

The HUI traded below 217 for a short while on Wednesday before reversing

sharply higher, opening up the possibility that we've just seen a successful

test of the early February low. If gold follows our script then the HUI

might trade below yesterday's low, but we doubt that anyone is going to

have an opportunity to buy gold stocks at considerably lower levels; at

least, not within the next three months (late this year might be a different

story).

The performance of the Newmont Mining

stock price is probably more important than the performance of the HUI

at this time, and yesterday's intra-day plunge down to $41 by NEM sure

looked like a successful test of the lows (see chart below).

By the way: it might not seem this

way to anyone new to the world of gold stocks, but if we are right that

the lows for the HUI and many individual gold stocks were put in place

in early-February then this correction in the gold sector -- a correction

that we warned about repeatedly when the HUI was close to its highs in

December and January -- has been quite mild. This has probably been the

case because the overall stock market has remained reasonably firm. We

suspect that many holders of gold stocks don't view their gold stocks as

bets on a continuation of the bullish trend in the broad stock market,

but right now that's what they are. Gold stocks have been trending with

the stock market over the past 18 months and are likely to continue trending

with the stock market, although as explained many times in the past they

will probably remain strong for a few weeks after a major stock-market

peak is put in place.

Palladium

The current supply/demand picture for

palladium is quite bearish. As mentioned in a previous commentary we are,

however, long-term bullish on this metal. This is because we anticipate

a dramatic improvement in palladium's supply/demand situation over the

next few years.

Our reasoning, in a nutshell, is that

both palladium and platinum can be used in the manufacture of catalytic

converters (anti-pollution devices) for non-diesel car engines and that

there is currently an enormous gap between the prices of these two metals

(platinum is presently almost 4-times the price of palladium). This price

gap, in turn, will be a powerful incentive for car manufacturers to swap

from using platinum to using palladium when they re-tool for new models,

in the same way that an extremely high palladium price caused them to make

the opposite switch a few years ago.

The price-gap between palladium and

platinum could, of course, narrow as a result of a collapse in the platinum

price. However, while we are not bullish on platinum we doubt that there

will be a major (>30%) decline in its price because a sizeable drop in

price would bring-about an increase in the demand for platinum jewelry.

Therefore, the main impetus for a closing of the price gap over the next

few years is most likely going to come from a rising palladium price.

We don't do much technical analysis

of the palladium market and don't have any upside targets for palladium

as far as the coming 6-12 months are concerned. What we can say, though,

is that palladium appears to have less downside risk than any of

the metals we follow with the exception of gold. This is because its price

advance over the past 10 months has been very orderly (there is no sign

of an upside blow-off as there is with most of the other industrial metals)

and there is good support at $220 (less than 10% below the current price).

North American Palladium (AMEX: PAL,

TSX: PDL) was the one palladium play in the TSI Stocks List until we recently

decided to exit the stock after it doubled in a short space of time. Hopefully,

there will be an opportunity to re-enter PAL at a lower price during the

next several months.

Update

on Stock Selections

A

good update on the progress of NovaGold (AMEX: NG, TSX: NG) can be read

at http://biz.yahoo.com/bw/040301/15616_1.html. Bear in mind, when reading

this, that the company's current enterprise value (market cap plus net

debt) is only about US$200M. A

good update on the progress of NovaGold (AMEX: NG, TSX: NG) can be read

at http://biz.yahoo.com/bw/040301/15616_1.html. Bear in mind, when reading

this, that the company's current enterprise value (market cap plus net

debt) is only about US$200M.

Afrikander

Lease (JSE: AFL, Pink Sheets: AFKDY), a leveraged play on gold and uranium,

has secured enough cash through the issue of more shares and debt to complete

the purchase of the Kalgold mine from Harmony Gold. This essentially means

that the short-term danger is over for Aflease. All we need now is an increase

in the Rand gold price (we think the Rand gold price has bottomed and will

work its way higher over the remainder of this year) and for the company

to complete the process of getting its shares off the horrible "Pink Sheets"

in the US and onto a proper market.

The

senior managers at Citigold (ASX: CTO), the company formerly known as Charters

Towers, made a monumental blunder towards the end of last year when they

decided to raise money by issuing high-yielding convertible notes rather

than doing a normal equity issue; and shareholders are still paying for

this mistake as well as for the delays in finalising the issue. However,

the shares are beginning to show some signs of having bottomed. This is

a high-risk stock, but one that should do very well from current levels

if the company is able to commence production in accordance with its current

schedule, that is, by the third quarter of this year.

We wouldn't, by the way, be buyers

of the convertible notes at their issue price of 40c.

As

mentioned in Tuesday's e-mail alert, we've exited the second half of the

Western Silver (TSX: WTC) position for a profit of about 280%.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.futuresource.com/

|