![]()

![]()

![]()

![]()

- Interim Update 3rd May 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Almost everything

commodity related is weakening

Commodity 'plays' in general,

including the industrial metals, oil, the commodity currencies and most

commodity-related equities, have been persistently, albeit not

dramatically, weak since February. In many cases important support levels

are being tested or have already been breached.

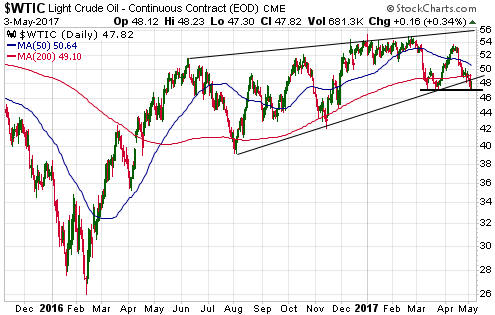

For example, the

oil price broke below intermediate-term trend-line support during the

first two days of this week and is now testing lateral support at $47. A

weekly close below $47 would eliminate any remaining doubt that an

intermediate-term decline is in progress.

For another example, it looks like copper is preparing to test

intermediate-term lateral support at $2.45.

For a third example, the Metals and Mining ETF (XME) broke below

intermediate-term lateral support at $29.00 on Wednesday 3rd May.

Commodity plays in general are also now short-term 'oversold'. This

probably means that interim lows will be put in place and 1-3 week

counter-trend rebounds will get underway within the coming few trading

days, but be aware that sharp declines could occur before these interim

lows are in place.

How

to know for sure that gold has commenced a cyclical bull market

We are almost alone among

long-term gold bulls in NOT believing that gold commenced a new cyclical

bull market in December-2015. Not that it really matters from a practical

perspective.

As we explained in a

recent blog post, while assertions to the effect that an investment is

in a bull or bear market can make for colourful commentary, in the real

worlds of trading and investing it's best not to get hung up on bull and

bear labels. For example, in January-2016 it wasn't necessary to believe

that a gold bull market was getting underway to determine that an

excellent opportunity to buy gold-mining stocks had arrived. All that was

required was objective, well-informed analysis of sentiment, price action

and inter-market relationships. It will be the same at the next excellent

buying opportunity.

That being said, there is a signal that always

gets generated in the early phase of a gold bull or bear market and that

generally doesn't get generated at other times. This signal can be used as

confirmation that a shift from bear to bull or bull to bear has happened.

The signal is a cross by the gold/SPX ratio (the US$ gold price

divided by the S&P500 Index) from above to below or below to above its

200-week moving average (200WMA). Since the early-1970s and with only one

brief exception (in 1976), not long after the start of a gold bull market

the gold/SPX ratio has moved above its 200WMA and remained above it until

the bull market ended. Also, since the early-1970s and with only one brief

exception caused by the 1987 stock-market crash, not long after the start

of a gold bear market the gold/SPX ratio has moved below its 200WMA and

remained below it until the bear market ended. Putting it more succinctly,

over the past 45 years a 200WMA cross by the gold/SPX ratio has reliably

indicated the start of a new cyclical gold trend early enough in the new

trend to be useful.

The following weekly chart shows the gold/SPX

ratio and its 200WMA (the blue line) since 1980. The December-2015 low was

more than 16 months ago and yet gold/SPX remains comfortably below its

200WMA. This is not where it should be if a cyclical bull market began in

December-2015.

At some future time the gold/SPX ratio will move above its 200WMA.

Unless it does so as the result of a 1987-style stock-market crash, when

it happens it will be confirmation that gold has commenced a cyclical bull

market.

What is a correction?

"Correction" is a commonly-used

term in the financial markets, but it is also a vague and somewhat strange

term. It is vague because whether or not a market move is a correction is

a matter of both opinion and timescale. It is strange because it suggests

that the market price was wrong and had to be put right (corrected).

A correction involves retracing part (occasionally all) of a move that

occurred in the direction of the main trend, but it is only with the

benefit of hindsight that it can be known whether a price move was a

correction to an on-going trend or a new trend. In real time, stating that

a market has begun a correction will always be stating an opinion rather

than a fact. Also, a trending move in one timeframe will usually be a

correction in a larger timeframe, and vice versa. We'll use silver's price

action to further explain.

When the silver price began to decline from its early-April high it

could have been 'correcting' the rally that began in March, but due to the

price having dropped below its March low we now know that the 'corrective'

move was actually the rally that began in early-March and not the decline

from the early-April high. In fact, it could be said that everything

that's happened since the late-February high is part of a correction, but

even this would just be an opinion because it would be based on the

assumption that the overall upward trend from the December-2016 low did

not end in February-2017. This assumption might not be valid, in that the

rally from the December-2016 low could be nothing more than a 2-3 month

correction to the downward trend that began in July of last year. In other

words, the December-February rally could be an interruption to the

intermediate-term downward trend that began in July-2016 rather than the

start of a new intermediate-term upward trend, in which case the decline

from the February-2017 high constitutes the resumption of the

intermediate-term downward trend.

Stepping further back, the rally

from the December-2015 low to the July-2016 high could be a correction as

opposed to the first leg of a new major trend; that is, it could be a very

strong counter-trend rebound within a continuing bear market. At this

stage, stating that it was the first leg of a new bull market is stating

an opinion, not a fact. And it's an opinion that, in our opinion, is

probably wrong.

Always be aware when a commentator is stating an

opinion that could be wrong rather than a fact that, by definition, must

be right. In the world of financial-market punditry, a lot of statements

that are presented as facts are actually opinions.

The Stock Market

Sometimes it really is

different

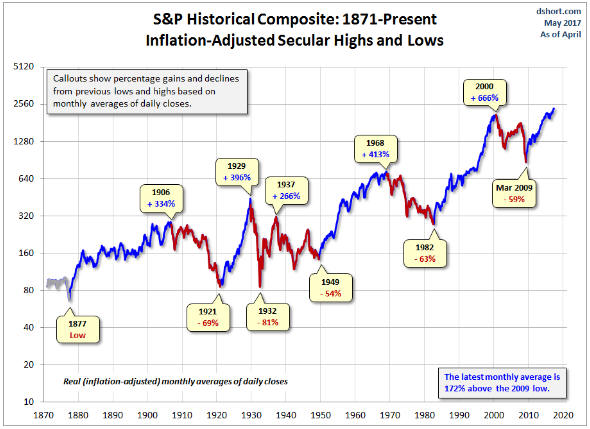

The following chart shows the

"inflation"-adjusted S&P from 1871 to the present, using monthly averages

of daily closing prices. We found the chart in the article posted

HERE. As explained in the article: "The implicit rule we're

following is that blue shows secular trends that lead to new all-time real

highs. Periods in between are secular bear markets, regardless of their

cyclical rallies. For example, the rally from 1932 to 1937, despite its

strength, remains a cycle in a secular bear market. At its peak in 1937,

the index was 29% below the real all-time high of 1929."

Due

to having reached new all-time highs in 'real' terms, the rally from the

March-2009 bottom is indicated on this chart to be a secular bull market.

The article doesn't specify how the inflation-adjusting was done, but

we assume that the CPI was used. If so, the 'real' gains during the

current cycle have been greatly magnified by virtue of US$ depreciation

being underestimated. Using our own method of inflation-adjusting, the

February-2017 high (the monthly closing high to date for the rally that

began in 2009) was below the October-2007 high, which, in turn, was below

the December-1999 high.

New all-time highs in inflation-adjusted

terms or not and a new secular bull market or not, the stock market rally

of the past several years has been extraordinary. Furthermore, it has been

different in one very important respect: it began at a much higher

valuation than any other comparable long-term rally in the US stock

market. Which goes to prove that the widely-ridiculed saying "it's

different this time" is sometimes correct.

The unprecedented

behaviour of central banks is the reason it has been different this time.

Here we are almost 8 years into a US economic expansion and the Fed is

still aggressively encouraging investors to take-on additional risk. And

compared to the ECB and the BOJ, the Fed looks downright prudent!

The Emerging Markets Equity ETF (EEM) refuses to buckle

Our bearish EEM speculation is not working. As illustrated below, EEM

made a new 12-month high during the first half of this week.

For emerging-market equities, the worst of all worlds involves

strength in the US$, weakness in the US stock market and weakness in

commodities. We expected that by now we'd have all three of these bearish

forces, but all we've currently got is the third one.

That being

said, we still like the bearish EEM trade, because we suspect that the US$

is only a few days from a bottom, that there is significant additional

price weakness in store for commodities, and that the US stock market is

not about to run away to the upside. Furthermore, EEM has established a

bearish momentum divergence over the past two months, with rising price

tops in parallel with declining tops in the daily RSI.

For new

money we would, however, prefer the September $35 EEM put options to the

June puts previously suggested. The June puts could still work, but the

probability of a substantial decline happening by mid-September is much

higher than the probability of a substantial decline happening within the

next 6 weeks.

Gold and the Dollar

Gold and Silver

On a short-term basis the silver market is now very 'oversold'. This

is evidenced by the price having fallen on 11 of the past 12 trading days

and by the daily RSI(14) shown at the bottom of the following chart. The

daily RSI's current level of 22 is unusually low. In fact, we have to go

back to 2014 to find a lower reading.

That the silver market is now

very 'oversold' should not, however, be construed to mean that a

sustainable low is not far away. We suspect that an interim low will be

put in place over the final two days of this week or the first half of

next week, but that the market is not yet close to what we would view as a

tradable low (a low that is followed by a multi-month rally).

As

mentioned in the Weekly Update, a sustainable/tradable price low probably

won't be in place until after at least half of the speculative bullish

positions in the futures market have been liquidated.

In the latest Weekly Update we wrote that we would take profits on our

silver hedges (SLV put options) if the silver price dropped to near its

March low of $16.80 this week. This happened on Monday, so our silver

hedges have been removed with a plan to establish a new hedge position

following a rebound.

Given that the silver price continued to

decline after we exited our SLV puts, our timing wasn't ideal. However, we

figured that with the silver/gold ratio even more 'oversold' than the US$

silver price (the daily RSI for the silver/gold ratio is at its

second-lowest level of the past 5 years), the only way the silver price

could extend its decline would be if the gold price fell sharply, in which

case our gold hedge position in the form of GLD put options would come to

life.

As illustrated below, the gold price broke below support at

$1260 on Monday 1st May and then followed through to the downside. This

means that gold bullion has finally acknowledged the warning signs that

the gold-mining sector has been flashing for some time.

Our guess is that gold, like silver, will reach an interim price low

within the coming few days.

Gold Stocks

After performing dismally relative to gold bullion over the preceding two

weeks, over the first three days of this week the HUI held up well in the

face of a downside breakout in the gold price. This is consistent with the

view that interim lows will soon be in place for gold and silver.

The HUI has support at 180 and then at 160. It looks like the higher of

these support levels will hold if tested in the near future, but we

suspect that the lower support will be breached before the start of the

next multi-month rally.

Recall the two short-term HUI scenarios mentioned last week. These

scenarios could be called "capitulation now" and "capitulation later", in

that one involves a capitulation within the next few days and the other

involves 1-2 months of back-and-forth price action between the March low

and the April high prior to a capitulation. Both scenarios remain in play,

although time has almost run out for the first one.

The

Currency Market

Since dropping to a marginal new low for

the year during the two trading days following the first round of the

French Presidential election, the Dollar Index has drifted in a narrow

range near its 200-day MA. This looks like a consolidation prior to what

we think will be a trend-ending downward spike.

A trend-ending

downward spike will potentially happen early next week if, as seems

extremely likely, Macron wins France's Presidential election run-off on

Sunday 7th May.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

![]()