![]()

![]()

![]()

![]()

- Interim Update 3rd June 2015

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

No sign of a US

recession, yet

As we've noted in the past, it's

unlikely that an official US recession will begin until after the ISM (Institute

of Supply Management) New Orders Index has broken solidly below 50 (say, to 48

or lower). In March the Index was only marginally above 50, but in April it

ticked upward by a couple of points and the May figures released early this week

showed another up-tick of a couple of points.

The message of this reliable economic indicator is therefore unchanged from last

month. The US economy remains sluggish, but it isn't in immediate danger of

entering recession territory.

The Stock Market

The US

Valuation

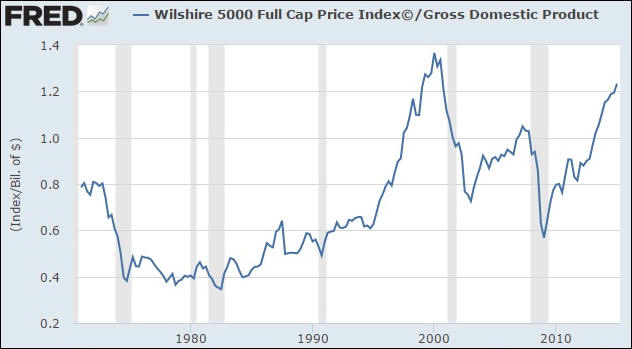

With the exception of a 12-month period around the March-2000 stock market peak,

the Wilshire5000 Index, the broadest US equity index, is higher today relative

to US GDP than it has ever been. In particular, the Wilshire/GDP ratio is much

higher today than it was at the major peaks of 2007 and 1972. Refer to the

following chart for details. Given this fact, it's strange that there is an

on-going vigorous debate about whether or not the market is over-valued. We have

some sympathy for the view that an over-valued market can always become more so

and that a major top could therefore still be a considerable distance away, but

we have nothing but contempt for the view that the market is currently not

expensive.

We've presented the above chart in previous commentaries, but there is an

interesting aspect of this chart that we haven't previously mentioned (because

we were too focused on the chart's market-valuation message to notice anything

else). We are referring to the fact that since 1970 the Wilshire/GDP ratio has

always peaked about two quarters prior to the start of an official recession.

For example, the most recent official recession began in December of 2007 and

the Wilshire/GDP ratio peaked in Q2-2007.

Now, the GDP numbers are issued quarterly, so the most recent point on the above

chart is for Q1-2015. When the Q2-2015 GDP number is published in July it will

possibly show that Q1-2015 was the peak for the ratio, but even in this

worst-case scenario the historical relationship would suggest that the start of

the next US recession was still a few months away.

Margin Debt and the Bull Market

Over the past year we've reported on the NYSE Margin Debt situation every 1-2

months. For many months it looked like a major margin-debt peak had been put in

place in February of 2014, but margin debt made a new all-time high in March.

Due to the lead-lag relationship between the long-term trends in margin debt and

the S&P500 Index, this suggested that the US equity bull market was still at

least a few months from its end.

Just to be clear, an unusually-high level of margin debt points to substantial

long-term downside risk, but in the past the shift from bull-market to

bear-market has followed the peak in margin debt by at least a few months. As

long as leverage is still increasing, as indicated by new highs in margin debt,

the end of the bull market probably isn't imminent.

The NYSE margin debt figures for a month are always reported about 4 weeks after

the end of the month, which is why it took until late last week to find out what

happened to this measure of leverage in April.

As illustrated by the following chart from the article posted

HERE, NYSE margin debt was sharply higher in April. This increases long-term

risk, but, paradoxically, reduces the probability that the bull market is ending

right now. As mentioned above, the reason is that the general leverage of market

participants is still expanding.

An additional multi-month extension of the US equity bull market involving a

shift in favour of commodity stocks continues to be one of the two

highest-probability intermediate-term scenarios. This scenario is consistent

with the April surge in margin debt. The second scenario is that we have just

witnessed the same type of short-lived breakout to new highs in senior stock

indices that marked major tops in 2000 and 2007.

If the second scenario is playing out then the S&P500 Index should not make a

new weekly closing high, that is, the S&P500 should not end a week above 2126,

from now on. At least, that's the 'stop' that we will be using for bearish

speculations in our own account. The S&P500 ended Wednesday's session at 2114,

so it would only take a minor amount of strength from here to prompt us to exit

our bearish US stock-market position -- a position that was averaged-into over

the past three weeks.

Gold and the Dollar

Gold

The first three trading days of this week provided nothing in the way of new

information about gold's short-term prospects. For example, gold rebounded to

$1200 early in the week, but, as noted in the latest Weekly Update, a rebound of

this magnitude would not be surprising even if gold had embarked on a short-term

downward trend. The gold price then reversed course, but has remained within the

narrow range of the past two months.

One of two things is almost certainly going to happen this month to 'break the

deadlock'. The gold price is either going to move solidly below support at $1180

and drop back to the vicinity of its November-2014 low, or it is going to move

solidly above $1220 and confirm that no further testing of the 2014 low will be

required. We are leaning towards the former outcome, but not with conviction.

The gold market might 'tip its hand' on Friday in the aftermath of the monthly

US Employment Report.

What is the probability that gold will break well below its 2014 low?

Such probabilities are always unknowable, but we will be surprised if it

happens. Here's why:

1) Gold's fundamentals are not bullish at this time, but they aren't bearish

either. They remain 'mixed, with some (the yield curve and the US dollar's

exchange rate) having recently become more bullish and others (real interest

rates and the banking sector's relative strength) having recently become more

bearish.

2) The price action since mid-2013 appears to be part of a long-term bottoming

pattern in the form of a wedge. Refer to the following weekly chart for details.

This pattern allows for a marginal new bear-market low prior to the start of the

next tradable rally, but it doesn't allow for a more bearish short-term outcome.

3) The sentiment backdrop, as indicated by the COT data, is currently neutral or

slightly-bullish for gold and bearish for silver, but if prices retreated to

their 2014 lows it would probably turn unequivocally bullish due to the

liquidation of speculative 'longs'.

Gold Stocks

The HUI has done very little so far this week and remains slightly above

trend-line support in the low-160s. A break below this support, which could

happen in reaction to Friday's US employment data, would likely be followed by a

decline to the more important support that lies at 145-150.

Of course, a decline to 145-150 is not a foregone conclusion. It's possible, for

example, that support in the low-160s will continue to hold and that the next

move of significance will be higher.

As advised in the latest Weekly Update, we would now view a weekly close above

185 as a clear-cut sign that the HUI was going to avoid another test of its

November-2014 bottom.

The Currency Market

So far this week the currency market has mostly been about Greece. In

particular, the Dollar Index pulled back sharply over the past two days, but

this US$ decline was almost entirely due to strength in the euro on the back of

a growing belief that Greece and its official-sector creditors will soon do a

deal that maintains the status quo. In other words, the US dollar's weakness was

not broad-based.

We confess to being unable to find anything resembling logic in the

publicly-stated negotiating positions of either the Greek government or its

official-sector creditors.

The Greek government now appears to be aiming for a deal that continues the game

of "extend and pretend", after being committed to a more permanent and realistic

solution early this year. From our perspective it is holding almost all the

cards, in that it could simply default and stay in the monetary union. However,

it has been acting like it has a very weak hand.

For their part, the creditors are trying to make it as difficult as possible for

the Greek government to get access to additional financing, but the only reason

the Greek government needs additional financing is to pay the same creditors. In

effect, the creditors have been threatening to cut off the flow of money to

themselves. Putting it in more colourful terms, the negotiating position of the

Greek government's official-sector creditors appears to be: "If you refuse to

play ball, we will shoot ourselves in the foot!"

The financial markets are currently discounting more "extend and pretend" with

regard to Greece's government debt, which is why gold wasn't helped by the

decline in the Dollar Index over the past two trading days. Gold, the ultimate

safe haven, benefits from the perception of increasing problems with the

monetary and banking systems.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://research.stlouisfed.org/

![]()