![]()

![]()

![]()

![]()

- Interim Update 3rd October 2018

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The September Monthly

(and Quarterly) Close

The closing prices for September

provided a small amount of additional information, although on a monthly

closing basis the currency market continues to do what it needs to do to

maximise uncertainty.

The US$ gold price has now declined for 6

months in a row and has just achieved its fourth consecutive monthly close

below its 21-month MA (the blue line on the following chart). Moreover,

the 8-month MA (the black line on the following chart) has just crossed

from above to below the 21-month MA. This is long-term bearish, but it

doesn't preclude a tradable multi-month rebound.

(Note that the

following monthly charts show the situation at the end of September, that

is, the charts don't include the first few trading days of October.)

As was the case at the end of the preceding month, the September close

for the Dollar Index (DX) was noncommittal. The DX was virtually unchanged

over the course of the month and ended September marginally below critical

resistance. This means that the monthly close provided no help in

determining whether the rebound from the early-2018 low was a

counter-trend move in a new US$ bear market or the resumption of the US$

bull market that began in 2011.

The euro is in a similar position to the DX, except that whereas the

DX is challenging critical resistance the euro is challenging critical

support.

The following monthly chart shows that the euro tested

support at 115.6 during each of the past 5 months. The support has been

violated multiple times on an intra-month basis (most recently this week),

but it has held firm on a monthly closing basis despite a fundamental

backdrop that has strongly favoured the US$ over the euro.

A

monthly euro close below 115.6 would be evidence that the euro's reversal

from its Q1-2018 high marked the resumption of its multi-year bearish

trend as opposed to the start of a corrective pullback within a new

multi-year bullish trend.

Our final monthly chart is consistent with the view that a

long-term top is in place for the 30-year T-Bond. It shows a downside

breakout in January to complete a major head-and-shoulders topping pattern

and then eight consecutive monthly closes below the 84-month MA (the blue

line).

The bond market

is pushing the envelope

The market for long-dated US

Treasury securities is threatening to break out to the downside. In fact,

by some measures it has already broken out. If a downside breakout is

confirmed by the weekly close on 5th October it will be consistent with

our big picture view that a bond bear market began in July-2016, but it

will be inconsistent with our expectation for a multi-month counter-trend

rally to precede a downside breakout to new lows for the year.

For

the iShares 20+ Year Treasury Bond ETF (TLT), the breakdown level is

$116.00. This level is defined by the lows of the past three years and was

breached on a daily closing basis on Wednesday 3rd October.

For the 10-year T-Note, the breakdown level is defined by the May-2018

low near $118.

The reason we've been expecting a counter-trend rally prior to a

downside breakout is the extremely-lopsided sentiment situation indicated

by the COT data.

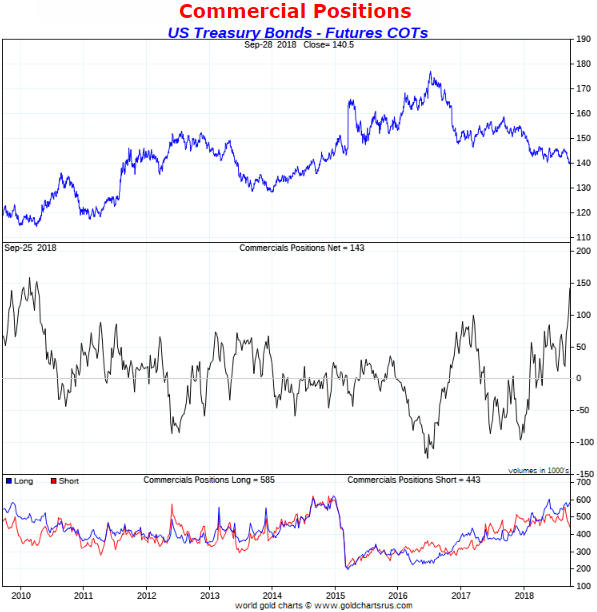

According to the following charts, the sentiment

situation became even more lopsided last week. The middle section of the

first chart shows that the commercial net-long position (the equivalent of

the total speculative net-short position) in 10-year T-Note futures

returned to its August-2018 all-time high last week, while the middle

section of the second chart shows that the commercial net-long position in

30-year T-Bond futures has just risen to its highest level since 2010.

The T-Bond and gold markets are in similar positions in that they are

both being supported by bullish sentiment and weighed down by bearish

fundamentals.

Due to the sentiment situation we expect that a

near-term downside breakout in the bond market will not have much

follow-through, at least in terms of time.

The O&G Rally

When the oil price broke above

short-term resistance at around $70.50 during the week before last it

suggested that the July high would be tested or marginally exceeded prior

to the start of a meaningful correction. On Wednesday 3rd October the July

high was marginally exceeded. The rise in the oil price to a new high for

the year could turn out to be an important upside breakout, but the

breakout must be confirmed by the weekly close to make it official.

Also worth mentioning is that there was significant strength and a

minor upside breakout in the natural gas price within the past few days.

The strength in the oil market, the strength in the stock market and

the weakness in the T-bond market appear to be linked. Moreover, each of

these markets looks stretched in the direction of its current short-term

trend, so reversals could happen at any time.

We will have more to

say about oil and gas in the coming Weekly Update.

The Stock Market

The US Bank Index (BKX) has been

very weak over the past month, both in nominal dollar terms and relative

to the broad market as represented by the SPX. This weakness is surprising

given that US bank stocks generally have reasonable valuations and the

fundamental backdrop appears to be bullish for banks. However, the global

banking system is interconnected, so it's likely that US bank stocks are

being pulled down by the problems and obvious risks in the euro-zone

banking industry.

With reference to the following daily chart, the

BKX has important support at $103-$104. This support has been tested

numerous times over the past 7 months, with the most recent test occurring

on Tuesday of this week.

A weekly close below $103 would be a

decisive breakdown.

According to the article posted

HERE, there have been 10 "Hindenburg Omen" signals over the past month

or so. A cluster of such signals appears to be a necessary, but not a

sufficient, condition for a substantial stock market decline.

The

large number of Hindenburg Omens in the recent past appears to be related

to the adverse effect of rising interest rates on the fixed-income

securities that trade on the stock market. The same phenomenon is

impacting measures of stock-market breadth. For example, the all-stocks

NYSE Advance-Decline Line (ADL) shown in the bottom section of the

following chart suggests that there has been a bearish divergence between

the ADL and the SPX since late-August, but an ADL that includes only

common stocks does not reflect the same bearish divergence.

Another concern is that on 26th September our put/call indicator

generated its first sell signal in almost two years. A sell signal occurs

when the ratio shown in the bottom section of the following chart drops

below 0.30.

Historically, put/call sell signals have been less

reliable than put/call buy signals. However, they usually work if they

occur when the market is short-term 'overbought', as is the case right

now.

The relative weakness of the banking sector, the Hindenburg Omens and

the put/call sell signal are warnings that a meaningful (5%-10%) decline

could soon get underway, but the developing downside breakout in the bond

market is by far the biggest threat to the stock market. If the bond

market extends its recent decline then the stock market will be in

trouble.

A daily SPX close below 2870 would be evidence that a

meaningful stock market decline had begun.

Gold and the Dollar

Gold

Our

Gold True Fundamentals Model (GTFM) is the best indicator of the extent to

which the fundamental backdrop is bullish or bearish for gold. A less

accurate, but simpler -- and still effective most of the time -- way to

assess gold's fundamental situation is to monitor the bond/dollar ratio

(the T-Bond price divided by the Dollar Index). Below is a weekly chart

comparing the US$ gold price with the bond/dollar ratio.

The

bond/dollar ratio is now testing its low of the past 5 years, so an

argument could be made that the US$ gold price is higher than it should

be.

A substantial gold rally cannot occur in the face of a gold-bearish

fundamental backdrop, but both the sentiment situation and the price

action suggest the potential for a significant extension of the recent

rebound.

With regard to gold's price action in US$ terms, the

50-day MA has acted as a ceiling on numerous occasions over the past three

weeks. This suggests to us that a lot of 'buy stops' will be triggered if

the US$ gold price manages to close above this MA.

Silver

The silver price lagged the gold price

as part of the bottoming action of the past two months. This is normal and

actually could be viewed as a positive sign.

Late last week the

silver price made a catch-up move and is now in a similar position to the

gold price. Like the gold price, the silver price is challenging

short-term resistance defined by its 50-day MA.

Even if we are dealing with nothing more than a counter-trend rebound,

which will be the case unless the fundamental backdrop turns in gold's

(and therefore silver's) favour, the silver price could rise as high as

$16 within the coming 6 weeks.

Gold Stocks

The good news is that the gold-mining sector, represented on the following

chart by the Gold Miners ETF (GDX), appears to be basing. This suggests

that additional gains will be made over the weeks ahead. The bad news is

that the rebound from the early-September low looks more like a

counter-trend move than an important reversal. The reason is that it has

taken 16 trading days for GDX to reach its 50-day MA, whereas the initial

up-moves following intermediate-term bottoms tend to reach/exceed the

50-day MA in 7 days or less.

If we are dealing with a short-term

rebound within an on-going intermediate-term downward trend, then GDX's

upside probably will be limited by resistance near $21.00. For the HUI,

the equivalent resistance lies at around 170.

As we first mentioned a couple of months ago, the way things are

panning out the November-December period, which has provided a tradable

low for the gold-mining sector in each of the past 5 years, could provide

a tradable high (a high that should be used for hedging or selling) in

2018. We'll see.

The Currency Market

The

much higher-than-expected budget deficit projected by Italy's government

caused a sell-off in Italian government bonds and increased the demand for

German government bonds. The additional fear-related demand for German

government bonds widened the US-Germany yield spread to a new multi-year

high in the dollar's favour, putting irresistible downward pressure on the

euro and upward pressure on the Dollar Index (DX) over the past 5 trading

days.

On Wednesday 3rd October the euro broke below lateral support

at 115.6. This suggests that the August low will be tested within the next

few weeks.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Company

news/developments for the week ending Friday 28th September 2018:

Company

news/developments for the week ending Friday 28th September 2018:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY =

Financial Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery,

MD&A = Management Discussion and Analysis, M&I = Measured and Indicated,

NAV = Net Asset Value, NPV(X%) = Net Present Value using a discount rate

of X%, NSR = Net Smelter Return, P&P = Proven and Probable, PEA =

Preliminary Economic Assessment, PFS = Pre-Feasibility Study]

*Alkane Resources (ALK.AX) is going ahead with the

development of underground mining operations at its Tomingley gold mine.

The plan is for the new underground operation to produce 93,000 ounces of

gold over a 40 month period commencing mid-2019.

Due to the high

forecast cash costs of the underground operation (A$1,100-$1200/oz), the

aforementioned 93K ounces of production won't add much cash to ALK's

balance sheet. In fact, developing the underground operation initially

will drain A$25M from ALK's cash reserve (A$80M at 30th June). However,

the underground operation will create opportunities to discover new

economic gold resources and thus extend the overall mine life.

*Blackham Resources (BLK.AX) has raised A$7.5M by issuing

a secured convertible note with a 24-month term to The Lind Partners, a

New York based institutional fund manager and a long-time investor in BLK.

This financing, along with BLK's existing cash, will be used to fully

repay A$13M of short-term secured debt owed to Orion.

The note will

be convertible into BLK shares at the lower of A$0.08 and 90% of a

volume-weighted average market price. Also, the first repayment is

scheduled for 14th February 2019, which is two weeks after the expiry date

of 534M A$0.08 options. The idea is that any proceeds received from

exercising the options will be used to repay the convertible note.

Issuing the convertible note to Lind could turn out to be a high-cost or a

reasonable-cost financing arrangement for BLK depending on whether its

stock price is above A$0.08 early next year. If it is above $0.08 then a

lot of cash will flow into the company due to the exercising of the

above-mentioned options and the note will be repaid at a reasonable cost,

but if the stock price is still well below A$0.08 when the options expire

in January then the cost of repaying the note will be high.

*Clean TeQ (CLQ.AX, CLQ.TO) has formed a JV with Ionic

Industries Pty Ltd to develop and commercialise a graphene-oxide based

water filtration membrane (GO-Membrane). CLQ will own 75% of the JV. The

goal is for the GO-Membrane to replace the existing membranes in reverse

osmosis and nanofiltration systems used for water purification (e.g.

converting seawater into drinkable fresh water). According to CLQ's press

release, the GO-Membrane manufacturing process has already been

demonstrated on commercial scale industrial equipment.

The

GO-Membrane JV is financially irrelevant to CLQ at this time, but it's an

interesting opportunity that could have significant value in the future.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

http://www.goldchartsrus.com/

![]()