![]()

![]()

![]()

![]()

- Interim Update 4th January 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

2017 Surprises

Following the lead of Byron Wien

and Doug Kass, near the beginning of the past two years we presented a

list of potential financial-market surprises for the year ahead. These are

events/developments that are expected by very few market participants and

commentators, but in our view have either a greater than 50% chance of

happening or at least a high-enough probability of happening to be worthy

of serious consideration. Partly for fun and partly because it's a

worthwhile exercise to consider the potential outcomes that are both

realistic and widely ignored (the best money-making opportunities are

created by outcomes that have a much higher probability than most people

believe), we are doing the same this year.

Before we get to this

year's list of potential surprises, some words about last year's list are

in order. Specifically, of the ten 2016 surprises included in the 11th

January 2016 Weekly Update, which ones happened and which ones didn't?

Here are the 2016 surprises that happened or came close:

Surprise #3: "Commodity indices such as the CRB and the GNX bottom

during the first quarter of the year and have an upward bias over the

remainder of the year."

This is exactly what happened.

Surprise #4: "Following a Q1 capitulation, emerging-market equities

(as represented by EEM) begin to strengthen relative to developed-market

equities (as represented by the SPX). The EEM/SPX ratio ends the year with

a gain, which is a huge surprise to the many analysts who remain convinced

that US economic fundamentals are vastly superior to emerging-market

economic fundamentals."

This one was close enough. The EEM/SPX

ratio began to strengthen after making an early-2016 bottom and ended the

year with a very small gain. However, the percentage gain would have been

in double digits if not for dramatic post-election strength in the US

market.

Surprise #6: "The "FANG" stocks (Facebook, Amazon,

Netflix and Google), the focal points of investment demand and the leaders

to the upside over the past two years, are relatively poor performers."

This happened, as the 7.1% average gain in the FANG stocks was well

below the 12% gain in the S&P500 ETF.

Surprise #7: "The oil

price bottoms during the first quarter of the year and, despite on-going

concerns about a supply glut, experiences a trough-to-peak gain of more

than 70% on the back of increasing instability in Saudi Arabia and other

important oil-producing nations."

This happened, although the

main reason for the strong oil-price rebound wasn't increasing instability

in the Middle East.

Surprise #8: "The Yen is the strongest

major currency."

This one was close enough. Despite its large

September-December decline, the Yen out-performed every major currency

over the course of 2016 with the exception of the Canadian dollar.

Relative to the Canadian dollar it was flat.

Surprise #9: "Gold

has a 'choppy' upward trend as part of a long-term basing pattern, but the

big story is the performance of the gold-mining sector. The gold-mining

indices outperform gold by a wide margin."

Gold's rise was

certainly 'choppy' and the gold-mining indices did, indeed, outperform

gold by a wide margin.

And here are the speculated 2016 surprises

that didn't come close:

Surprise #1: "The US economy enters a

recession during the first quarter of 2016, although, as per its normal

practice, the NBER (the official recession adjudicator) doesn't officially

confirm the recession's early-2016 start until about 12 months later."

The NBER is definitely not going to record a recession as having begun

in 2016, so this didn't happen.

Surprise #2: "The S&P500 Index

(SPX) suffers a peak-to-trough decline of more than 20% and ends the year

with a loss of more than 10%."

This and Surprise #10 were

furthest from coming to pass.

Surprise #5: "...The US 10-year

T-Note, which yielded 2.13% at the end of last week, finishes the year

with a yield of more than 3%, while euro-zone government bonds perform

much worse and experience much larger yield increases."

Due to

impressive rebounds in government bond yields during the second half of

2016 this surprise was closer to happening than seemed possible at

mid-year, but the 10-year yield ended 2016 about 0.5% below 3% and

Germany's 10-year Bund yield ended the year slightly lower than it began

the year.

Surprise #10: "The uranium price rises above

$50/pound."

Uranium ended up being surprisingly weak rather

than surprisingly strong.

Now, in no particular order here's our

list of potential 2017 surprises:

1) Despite some first-half

weakness due to more "Brexit" uncertainty, the British Pound ends the year

as the strongest major currency.

2) Natural gas (basis the nearest

US futures contract) trades above $5 (current price: $3.27) and the

oil/natgas ratio (the oil price divided by the natgas price) drops from

its current level of 16.3 to below 8.

3) The Chinese Yuan loses

more than 10% of its value and makes a new 10-year low relative to the

US$.

4) The S&P500 Index (SPX) trades below 2000 within the first

half of the year; in other words, at some point during the first half of

2017 the SPX trades at least 11% below its 2016 closing level.

5)

The general perception that "inflation" is a problem emerges during the

second half of the year.

6) The 10-year Treasury yield is

unexpectedly volatile, falling below 2% during the first half of the year

in response to stock-market weakness and constructive sentiment and then

rising above 3% before year-end in response to the emerging fear of

"inflation".

7) Due to financial-market volatility, the Fed makes

only one rate hike.

8) The "FANG" stocks (Facebook, Amazon, Netflix

and Google) continue to underperform the broad market.

9) Trump

becomes increasingly erratic over the course of the year as he finds out

that his ability to control economic and financial-market outcomes is

minimal. A consequence is that there are multiple high-profile

resignations from his cabinet.

10) Greece has one of the world's

best-performing stock markets.

US Recession Watch

The ISM Manufacturing New Orders

Index (NOI) is the most reliable short-term leading indicator of US

recession, which is why it is one of the few economic data points that we

regularly discuss at TSI.

The latest NOI (the number for

December-2016) was reported on Tuesday of this week. As illustrated by the

following chart, it rose to a 2-year high and is now well above the level

it would have to drop below (the red line on the chart) to warn of an

imminent start to a recession.

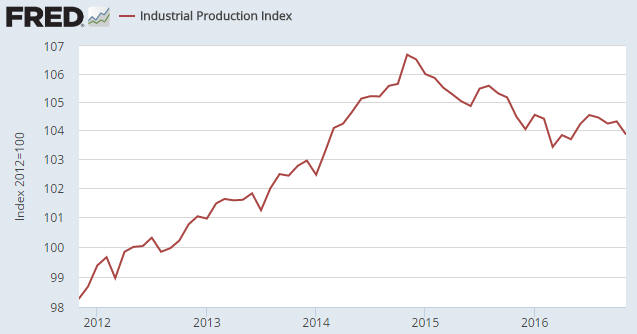

The ISM Manufacturing NOI tends to lead the Industrial Production

Index (chart included below) by about 6 months at turning points. The

strong rebound in the NOI since bottoming in August of last year therefore

suggests that US industrial production, which is presently not far from a

3-year low, will begin to rebound by March of this year.

The message of the ISM Manufacturing NOI, the most reliable short-term

recession indicator, is that a US recession will not begin EARLIER than

the second quarter of 2017. At the same time, the message of Real Gross

Private Domestic Investment (RGPDI), the most reliable long-term indicator

of US recession, is that a US recession will not begin LATER than the

second quarter of this year.

The combined message of the two

indicators could therefore be interpreted as: a recession should begin

during the second quarter of this year. However, we aren't confident that

this is the correct interpretation. The reason is that due to the

extraordinary interventions on the monetary front and the likelihood that

-- for the first time ever, as far as we can tell -- "fiscal stimulus"

will be implemented in the US with the economy in the late stages of an

expansion, the time from a downward reversal in RGPDI to the start of a

recession could be longer during the current cycle than during any

previous cycle.

The Stock Market

The US

When the NASDAQ100 Index (NDX) closed below 4900 at the end of December it

opened up the possibility that the preceding upside breakout was false. It

rebounded over the first two trading days of January and is back above

4900, but this doesn't tell us much. It now needs to either close below

its end-December low to confirm the short-term bearish signal or above its

December high to indicate that the short-term upward trend that began in

early-November is intact.

Short-term momentum and sentiment indicators are neutral, so there is

scope for significant moves to the upside or the downside over the next

few weeks. Sorry we can't be more definitive, but that's the way it is.

Although we don't have a strong opinion on which way the market will

break over the weeks ahead, it is fair to say that we are short-term

bearish on a risk/reward basis. In other words, we think there is greater

short-term downside potential following a break below the late-December

low than upside potential following a break above the December high. This

is due to our longer-term concerns about sentiment (the likelihood that at

some point over the next few months the realisation will take hold that

Trump's policy choices will not bring about a significant economy-wide

improvement in corporate earnings) and valuation. At some point, long-term

issues become short-term issues.

Emerging Markets

The Emerging Markets Equity ETF (EEM) has rebounded from support at

$34 to slightly below a confluence of resistance at $36. If it gets past

resistance at $36 then it will probably test the 2016 high near $38.

We will be surprised if EEM gets through resistance at $36 and even

more surprised if it breaks above $38 within the next two months. That

amount of short-term strength in EEM would probably be associated with a

strong broad-based rally in commodity prices, which certainly wouldn't

create a problem for us (many of our equity positions would benefit from

such an eventuality) but is not the most likely short-term outcome.

We think the most likely short-term outcome involves market moves that

help our gold-related equity exposure and hurt our non-gold equity

exposure. These moves would include weakness in industrial commodity

prices and general stock-market weakness, with "emerging-market" equities

potentially getting hit harder than developed-market equities.

We

are therefore going to buy some EEM put options with a March-2017 expiry

date to hedge our non-gold equity exposure. If these put options don't

turn out to be profitable it will probably mean that our non-gold equity

positions have better short-term performance than we currently anticipate.

Gold and the Dollar

Gold

The

US$ gold price is continuing to slowly rebound from its mid-December

bottom. This rebound is expected to at least result in a test of lateral

resistance near $1200. If that resistance is breached it will mean that a

rise to the vicinity of the 200-day MA is probably in store.

Gold Stocks

The HUI's decline from its Q3-2016

peak is clearly defined by the channel drawn on the following chart. It

closed above the top of this channel on Wednesday 4th January.

Wednesday's breakout is marginal at present. It would, however, be

solidified by an additional gain of at least a few points on Thursday 5th

January.

If the HUI can make it up to 195-200 before the end of

this week then the channel top would be positioned to act as support

during a subsequent multi-day correction. This would set the stage for a

rise to at least 220 and potentially as high as 250 within the first

quarter of 2017.

We continue to expect a Q1-2017 move up to at

least 220.

Bolstering the view that there is significant additional upside in

store for both the gold-mining sector and gold bullion over the weeks

ahead is the recent strength in the gold-mining indices relative to gold

bullion.

As illustrated by the following chart, the HUI/gold ratio

has broken decisively above its 40-day MA (the blue line on the chart). A

breakout in the HUI/gold ratio above its 40-day MA doesn't always lead to

substantial strength, but following a large decline it is a prerequisite

for substantial strength. In other words, it doesn't necessarily imply

that a lot more strength is coming, but there is definitely not going to

be a lot more strength without it.

The Currency Market

The Euro

The currency market is drawing out the suspense

with regard to whether the euro will follow-through on its break below

major support at 105 or paint the downside breakout as a false signal and

rally for 1-3 months. We are leaning towards the latter scenario, but it

will take a daily close above 106 to indicate that this scenario is in

play.

On Wednesday 4th January the euro closed right at the 105

breakdown level, having probed the top and bottom of its recent narrow

range over the preceding two trading days.

The Yuan

China's currency, the

Yuan, has been steadily working its way downward relative to the US$ for

almost three years. The Yuan's total peak-to-trough decline relative to

the US$ is about 12%.

However, over the same period the Yuan gained about 14% relative to

the euro and is flat relative to the Yen. It is therefore not fair to say

that the Yuan has been a weak currency over the past few years.

According to Donald Trump, the Chinese Government has been trying to

manipulate its currency downward, that is, lower the Yuan/USD exchange

rate, to obtain an unfair trade advantage. This is demonstrably false, as

it's a fact that China's Government has been trying to counteract the

downward pressure on the Yuan stemming from large capital outflows by

selling-off its US$ reserves. Far from trying to manipulate the Yuan/USD

rate downward, China's Government has been trying to prop it up.

The Yuan looks 'oversold' on the above chart and could rebound for a

while, but eventually a point will be reached when China's Government

tires of 'throwing good money after bad' and lets the Yuan/USD ratio fall

to a level at which the Yuan is not substantially over-valued and can be

supported at a low cost. There's a decent chance that this point will be

reached during 2017.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://bigcharts.marketwatch.com/

![]()