![]()

![]()

![]()

![]()

- Interim Update 4th May 2016

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

US Economic Numbers

Conflicting Information

Businesses in the US have been cutting back on capital investment for the past

few years. This is an effect of the Fed's monetary policy, in that the

suppression of interest rates has encouraged stock buybacks and debt-financed

M&A at the expense of the capital investment that leads to greater productivity

and economic progress. Although GDP is a very poor measure of economic

performance, the lacklustre pace of business investment is consistent with the

unusually slow pace of GDP growth. At the same time, the lacklustre pace of

business investment is completely at odds with the reported improvement in the

jobs market.

As Jeffrey Snider pointed out in

a recent article, unless employers and businesses are now two separate

categories unrelated to each other it makes no sense to acknowledge that

businesses are cutting back on investments with a severity and at the same time

to claim that employers are ramping-up their hiring. However, many mainstream

economists and financial journalists have done exactly that -- in reaction to

the reported statistics, which, as noted above, are at odds with each other.

There are three possible explanations for the divergence between

business-investment and employment indicated by the official US economic

numbers. The first is that the investment numbers have been manipulated by the

government in an effort to make the economy look weaker than it really is. This

is completely implausible, because the government always tries to create the

impression that things are better than they are and because private-sector

numbers are consistent with the lacklustre business-investment numbers reported

by the government.

The second possible explanation is that the employment numbers have been

manipulated by the government in an effort to make the economy look stronger

than it really is. This is plausible and is probably part of the true story, but

we think that the third explanation is the most plausible.

The third explanation is that the employment numbers are completely useless as

economic indicators. The employment statistics dutifully reported each month by

the BLS contain so many dubious assumptions and sources of error that they are

little better than if they were randomly selected by a computer from within a

pre-determined range.

But please don't tell the Fed. The policy-making members of the Fed depend on

these numbers like a sailor tossed overboard into a rough sea depends on a

flotation device.

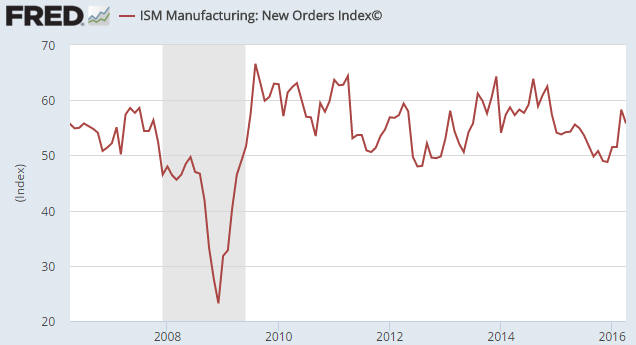

No recession signal, yet

Despite being in the sweet spot of the economic cycle, the US economy has been

sluggish for years. However, up until now it has managed to stay out of

recession territory.

After coming close to signaling a recession late last year, the ISM New Orders

Index rebounded strongly in March. The April number (published early this week)

was 2.5 points lower than the March number but was still comfortably above the

level that would point to a recession (an imminent recession is signaled by a

decline in this index to below 48).

The US economy is essentially in an economic no-man's land. It can't achieve

strong real growth, because the Fed keeps falsifying price signals and

incentivising unproductive spending. At the same time it is not in recession.

The Stock Market

The US

The NASDAQ100 Index (NDX) tested important support at 4300 last week and tested

it again on Wednesday 4th May. We are guessing that this support will hold for

now and that the decline from the April high will be partially retraced before a

much larger decline gets underway. However, if this support is breached without

there first being a 5-10 day rebound it will indicate that the market is

structurally even weaker than we think.

The SPX has been stronger than the NDX over the past month, but it too is

approaching a significant support level. For the SPX, support lies at 2040.

A breach of 2040 would suggest a near-term downside target of 2010-2015, which

is where the 200-day MA currently lies. We will be surprised if the 200-day MA

is decisively breached this month, but we are betting that it will be decisively

breached next month.

Whereas the NDX and the SPX have dropped back to significant support levels and

are well below last year's highs, the Dow Utility Average (UTIL) is in a very

different position. As illustrated below, it has moved sharply higher over the

past three weeks and is now testing its April high. Furthermore, its April-2016

high is its all-time high, so UTIL is very close to making a new all-time high.

UTIL has been lifted by strength in the bond market and the associated decline

in interest rates. It is a very risky proposition at current levels, because

even if long-term interest rates were to fall further the historical record

suggests that UTIL would be hit hard if there were a large decline in the broad

stock market.

Gold and the Dollar

Gold

In a post at

the TSI Blog prior to Wednesday's trading session we noted that the US$ gold

market was positioned in way that it could soon generate a useful clue about

future prospects. That's still the case.

Useful information would be provided by either a weekly close above last year's

high of $1308 or an intra-week rise above $1308 followed by a failure to end the

week above this level. In other words, this particular clue about the future

requires that gold at least trade briefly above $1308.

In addition, useful information about what's in store for gold could arrive on

Friday 6th May in the aftermath of the next monthly US employment report.

Regardless of what it says about the employment situation this report won't

alter gold's short-term price trend, but the gold market's reaction to the

report could provide a clue as to whether or not the short-term price trend has

reversed from up to down. For example, resilience in the gold market following a

strong employment report would suggest that the gold price was still in a rising

trend, whereas a price decline following a weak employment report would suggest

that the trend had reversed direction.

At this stage, what we have is a break above short-term resistance last week

followed by a pullback to test the breakout over the first three days of this

week (see chart below). A daily close below $1260 would clearly mark last week's

upside breakout as false, which means that a daily close below $1260 would also

be informative.

We now sit back and wait for more information.

Gold Stocks

On a short-term basis the HUI is in a similar position to gold, having broken

out to the upside last week and pulled back -- via three consecutive down-days

-- to test its breakout over this week to date. The difference is that last

week's up-move in the HUI took it above both short-term and intermediate-term

resistance, in that the 210 level for the HUI is equivalent to the $1308 level

for gold.

Last week's break above 210 suggested that the HUI could reach its 200-week MA

(a likely target for an intermediate-term top) as soon as the first half of May.

The 200-week MA is at 240 and Monday's high was 236, so the target has

essentially been reached.

With the HUI's rally from its January bottom having come very close to achieving

the most that the first intermediate-term advance in a gold-mining bull market

can reasonably be expected to achieve and with the gold-mining indices having

just experienced three consecutive down-days for the first time since the

January bottom, it's certainly possible that an intermediate-term top is in

pace. However, the evidence of a top is far from conclusive at this time. For

example, rather than this week's reversal marking a multi-month top, it could be

marking a shift to a higher-volatility final phase of the rally.

In any case, with the HUI having reversed downward after going almost as high as

the first intermediate-term advance in a bull market should go, we are now

intermediate-term neutral on the gold-mining sector. There is still a chance of

a final surge to a new high for the year within the coming few weeks, but our

guess is that the HUI will end this year within 15% of its current level.

We think that downside risk for the HUI over the days ahead is limited by

support at 190.

Before moving on it's worth noting that even if gold-mining indices such as the

HUI have already peaked on an intermediate-term basis, some individual gold

stocks will probably make new 12-month highs within the next several weeks.

The Currency Market

A potential British Pound trade

UK voters will go to the polls on 23rd June to decide whether the UK stays-in or

leaves the European Union (EU). We think that the UK will fare much better both

economically and socially over the years ahead if voters say yes to "BREXIT"

(leaving the EU), but regardless of the outcome of the vote we are becoming

interested in being 'long' the Pound for a short-term or an intermediate-term

trade. The three reasons are the chart-related evidence of an intermediate-term

bottom, the UK's relatively slow rate of monetary inflation and the volatility

that will stem from the upcoming "BREXIT" vote.

The first reason for our interest in accumulating a long position is illustrated

by the following chart, which shows that a potential base has formed over the

past four months. Ideally (to create the best set-up for a long position), the

price will pull back to around 143 to test the April breakout before resuming

its advance.

The second reason is illustrated by the following chart of the UK monetary

inflation rate (our chart uses the retail M4 number published monthly by the

BOE). This chart shows that the rate of increase in Pound supply has averaged

around 4%/year over the past 7 years (low relative to the US and the euro-zone)

and is presently near the bottom of its 7-year range, which means that a

stronger Pound is supported by the supply side of the equation.

The third reason is the potential for large fluctuations in the Pound's value

relative to the US$ in anticipation of and in reaction to the 23rd June BREXIT

vote. These fluctuations could provide opportunities to buy at depressed levels

and opportunities to take profits.

Our rough plan is to accumulate half of a full position during periods of

weakness prior to the BREXIT vote. We would then either double the position

following a sharp sell-off in reaction to a "yes" vote (although a "yes" vote

would be a long-term plus for the UK, the knee-jerk market reaction would

probably be a mini-panic out of the Pound) or take profits following a relief

rally in reaction to a "no" vote.

A position in the Pound could, for example, be taken by converting a bank

deposit from another currency to Pounds, purchasing Pound futures, purchasing

FXB (CurrencyShares British Pound ETF), or, for those who want more leverage and

are prepared to take a much greater percentage loss if the trade doesn't work

out, purchasing call options on Pound futures or FXB. Our intention at this time

is to convert part of an existing currency deposit to Pounds and to purchase

some September FXB call options.

As mentioned above, the price will ideally pull back to around 143 to test the

April breakout before resuming its advance.

The Dollar Index

In the latest Weekly Update, we wrote:

"The Dollar Index is likely to give either a bullish signal or a bearish

signal this week. A bullish signal would be generated by an intra-week spike

below the bottom of the 16-month horizontal range followed by a recovery to end

the week back inside the range (a false downside breakout). A bearish signal

would be generated by a weekly close below the bottom of the horizontal range."

The price action over the first three days of this week has opened up the

possibility of a bullish signal in the form of a false downside breakout, but

such a signal depends on the Dollar Index ending the week above 93.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Ivanhoe

Mines (IVN.TO) recently had the honour of having its Kamoa project in the

DRC named by the Mining Journal as the world's best undeveloped copper project.

This news prompted Rick Rule, the CEO of Sprott US Holdings and an IVN

shareholder, to interview Robert Friedland, IVN's CEO. You can listen to the

interview

HERE.

Ivanhoe

Mines (IVN.TO) recently had the honour of having its Kamoa project in the

DRC named by the Mining Journal as the world's best undeveloped copper project.

This news prompted Rick Rule, the CEO of Sprott US Holdings and an IVN

shareholder, to interview Robert Friedland, IVN's CEO. You can listen to the

interview

HERE.

The Rule-Friedland interview does a good job of outlining the unique speculative

opportunity represented by IVN. For example, the following points are made:

1) As noted above, the Kamoa project is arguably the best undeveloped copper

project in the world. The project is a joint venture between IVN and China's

Zijin Mining.

2) Given the deal done with Zijin and the equity/spending already contributed,

IVN is effectively financed through to production at Kamoa.

3) Kamoa will probably be economic at a copper price of $2/pound once new

discoveries are incorporated into the resource.

4) In addition to Kamoa, IVN owns the Platreef (South Africa) and Kipushi (DRC)

projects.

5) Platreef is the largest undeveloped PGM project in the world and Kipushi is

possibly the world's best undeveloped zinc project (the grade of the deposit is

an incredible 40% zinc-equivalent).

6) The company's mineral resources are the result of US$1.3B of drilling over

the past 18 years.

7) The company is debt free and almost all of its spending is discretionary.

8) Deals similar to the one that was done with Zijin at Kamoa could be done at

IVN's other projects, injecting large amounts of cash into IVN and avoiding the

need to issue new shares to finance future development.

9) Despite this remarkable portfolio of assets, the stock is being valued by the

market at only slightly more than cash value (the company has about C$0.93/share

of cash).

Assuming that commodity prices have begun to turn the corner, at some point over

the next couple of years IVN is likely to grab the investing community's

attention and experience a huge rise in market value. The main company-specific

risk is the DRC (Democratic Republic of the Congo) location of its two most

important assets (Kamoa and Kipushi).

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://research.stlouisfed.org/

![]()