![]()

![]()

![]()

![]()

- Interim Update 4th October 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

US Recession Watch

We pay close attention to three

leading indicators of US recession: Real Gross Private Domestic Investment

(RGPDI), the US yield curve and the ISM Manufacturing New Orders Index

(NOI). The latest iteration of the last of these indicators was reported

on Monday 2nd October.

The ISM NOI for September came in at 64.6.

This is very close to the top of its 10-year range and obviously a long

way above the level it would have to fall below (the red line on the

following chart) to warn of a recession.

With none of the leading indicators we care about currently warning of

recession and with the NOI having just risen to the top of its 10-year

range, the probability of a US recession beginning in 2017 is now

approximately zero. Given the tightening of monetary conditions it is

possible that a recession will begin as soon as the first quarter of 2018,

but it's more likely that there will be no recession until Q2-2018 or

later.

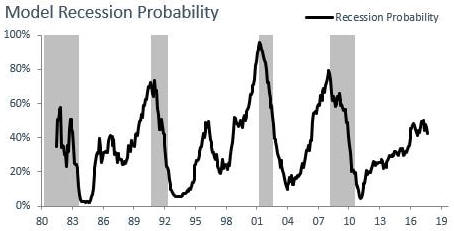

On a related matter, we mentioned a month ago that we had

discovered the web site

https://www.recessionprotect.com/. This site contains some economic

and stock-market models, one of which is the Recession Probability Model

depicted below. While this model's current reading of 43% suggests that

caution is warranted, it is well below the 70% level that was reached

prior to the starts of previous recessions.

The subscriber information at RecessionProtect.com gets updated at the

end of each quarter. An annual subscription costs $99, but the proprietor

of the site (Damon Callaghan, email damon.callaghan@gmail.com) is offering

TSI subscribers a one-year free trial.

To get the free trial,

first submit your name and contact information at

https://www.recessionprotect.com/store/p2/membership. Then in the

"Payment Info" section click on "Add coupon code", enter TSI100 as the

code and click "Next". This gives you a 12-month subscription with no

requirement to make any current payment and no obligation to make any

future payment.

We have no affiliation with RecessionProtect.com

and at this stage are unsure of its value, but it could be a useful tool

and thanks to the free trial offer it costs nothing to find out.

Could the next US

equity bear market occur in the absence of a recession?

The answer to the above question

is yes, it could, but it almost certainly won't. Both the historical

record and logic indicate that the next bear market in US equities will

almost certainly be accompanied by an economic recession.

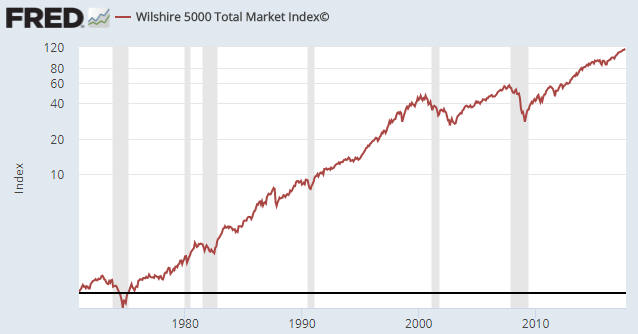

With

regard to the historical record, the following chart shows the

Wilshire5000 Total Market Index and the periods during which the US

economy was officially in recession (the shaded areas are the recession

periods). If we define a cyclical bear market as a downward trend lasting

at least 18 months and resulting in a peak-to-trough decline of more than

20% then there were four cyclical bear markets during the period covered

by the chart (1973-1974, 1980-1982, 2000-2002 and 2007-2009) and each of

these bearish cycles coincided with a recession. There were, however, two

recessions that didn't coincide with an equity bear market.

The

historical record therefore suggests that there could be a recession

without an equity bear market but not an equity bear market without a

recession.

With regard to logic, the monetary stimulus of the past several years

did a lot more to boost the stock market than the economy. The economy has

plodded forward at a snail's pace while the stock market has soared.

Ironically, this makes the economy less vulnerable than the stock market

to the removal of 'monetary support' and makes it very unlikely that the

economy will fare worse than the stock market at the conclusion of the

current cycle. Consequently, if there's a recession then there will almost

certainly be a bear market.

Also, even though the financial markets

have been distorted to a greater extent than the real economy by the

monetary machinations of the past several years, it's not realistic to

expect that the sort of general decline in leverage and pullback in

business spending that would be prompted by an equity bear market could

occur without the economy entering recession territory.

The bottom

line is that the next equity bear market and the next recession will go

hand-in-hand.

The Stock Market

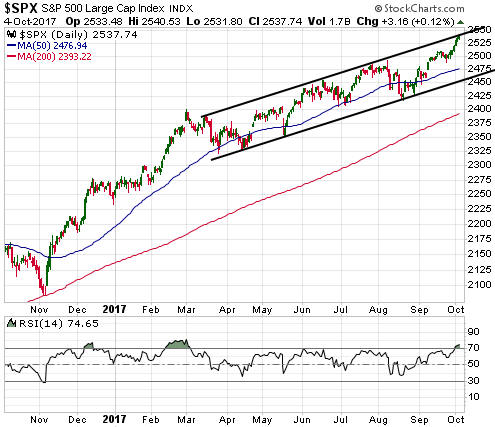

The S&P500 Index (SPX) gained

enough additional ground over the first three days of this week to reach

the top of its 6-month price channel. Also, the RSI included at the bottom

of the following chart indicates that it is 'overbought'.

The NASDAQ100 Index (NDX) has been weaker than the SPX of late and is

yet to break above its July high or become 'overbought'. However, it is

only about 0.5% from the top of the wedge pattern that it has traced out

since June.

As recently as a month ago the Russell2000 SmallCap Index (RUT) looked

like it was in the process of completing a major topping pattern, but it

then moved upward into all-time high territory in a virtual straight line.

To say that it is now 'overbought' would be an understatement given that

on Tuesday of this week its daily RSI(14) hit a 20-year high.

The above charts suggest that the US stock market is close to at least

a multi-week top in nominal terms. The chart displayed below suggests that

it is in a similar position in gold terms. At least, the following chart's

message is that the SPX/gold ratio is about to either reverse downward

from near 2.0 for the fourth time in two years or achieve a very important

upside breakout.

Whether the SPX/gold ratio reverses course without making significant

additional headway or breaks above its highs of the past 2 years will have

important implications for both the stock market and the gold market. In

particular, a solid break by the SPX/gold ratio to a new multi-year high

would eliminate the possibility that a cyclical gold bull market began in

December-2015.

Gold and the Dollar

Gold

We

think that the US$ gold price is close to a multi-week low, but that there

could be a final downward spike within the coming few days that pushes

gold's daily RSI (refer to the bottom section of the following chart) into

'oversold' territory (<30) prior to such a low being reached. The 200-day

MA near $1250 presents a realistic target for a final downward spike.

Perhaps the US monthly employment report on Friday 6th October will be

the catalyst for a trend-ending downward spike in the gold price. We can't

see a good reason for there to be a significant market reaction to

Friday's employment news, but it is often hard for us to predict how other

traders will react to news that should be unimportant.

The monthly

employment numbers are only ever important to the extent that they

influence the actions of the Fed and it's very unlikely that the numbers

to be reported this Friday will have any influence on the Fed. The reason

is that due to weather-related effects (the hurricanes) the reported

jobs-growth number is widely expected to be low, which means that a low

number will be put down to the hurricanes and will not reduce the

probability of a Fed rate hike in December. On the other hand, the futures

markets have almost fully discounted a Fed rate hike in December, so there

is very little scope for a strong number to increase the perceived

probability of such an outcome.

That is, neither a weak nor a

strong employment report on 6th October should have a significant effect

on what the Fed does over the coming few months, but that doesn't

guarantee that it won't cause some near-term gold-market volatility.

Based on the deterioration of gold's true fundamentals and the

non-supportive sentiment backdrop, at this stage we expect that gold's

rebound from an early-October low will end at a lower high (that is, below

$1362) and be followed by a decline to a lower low (that is, below

whatever low is put in place this week or next).

Gold

Stocks

Over the first three days of this week the HUI

survived another test of its 200-day MA and then moved up to its 50-day

MA. This is neutral price action.

The HUI is in a similar position

to gold. It is probably close to a multi-week low, but there could be a

final downward spike prior to such a low being reached. We think that if

there is a final downward spike in the HUI it will end at 180-185.

We would be remiss if we didn't point out that the gold-mining indices

have shown strength relative to gold bullion over the past few days. As

illustrated below, the relative strength was sufficient to push the

HUI/gold ratio above its 40-day and 150-day moving averages.

The

HUI/gold ratio has broken above its 40-day and 150-day MAs on three

previous occasions since the beginning of the year, but this is the first

time it has happened with both the HUI and gold near multi-week price

lows. That the latest HUI/gold breakout has happened with the market

closer to 'oversold' than 'overbought' improves the chance of significant

follow-through to the upside.

The Currency Market

The Dollar Index (DX) may

have completed the initial rebound from its September low, but just as

there could be a final downward spike in the gold market within the next

few days to set a multi-week price low there could be a final upward spike

in the Dollar Index to set a multi-week price high.

As illustrated

below, the DX has lateral resistance at 94. This resistance is a potential

target for a near-term upward spike. Alternatively, if it turns out that

the DX's initial rebound is already complete then the price action of the

past three days has defined the top of a channel that will be useful in

the future.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://research.stlouisfed.org/

![]()