![]()

![]()

![]()

![]()

- Interim Update 5th August 2015

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

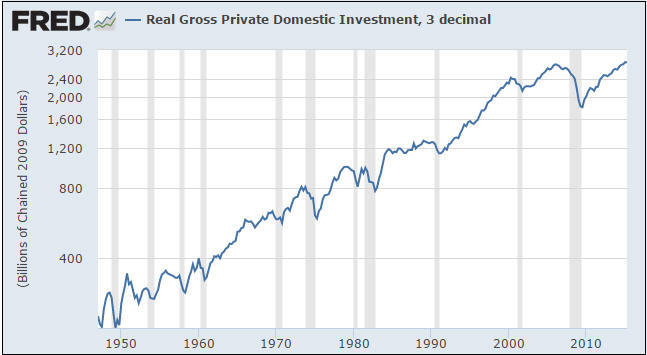

US Recession Update

Real Gross Private Domestic

Investment (RGPDI) is a leading indicator of US recession that has a perfect

record over its 67-year history, meaning that it has never generated any false

positive or false negative signals. It has always reversed its trend from up to

down in advance of a US recession and has otherwise never reversed its trend

from up to down. Strangely, in light of its record, its performance is not

widely followed or reported.

A problem is that RGPDI only gets updated quarterly. For example, prior to last

week the most recent RGPDI data was for the first quarter of this year. However,

given the fact that it usually turns down at least 1-2 quarters prior to the

start of a recession it can still be useful as a leading indicator.

Data released last week showed that RGPDI made a very-marginal new high in its

post-2009 trend (a marginal new all-time high, actually) during the June-2015

quarter, which tells us that the next official US recession is unlikely to start

prior to the final quarter of this year. The starting time could be much later

than that, but will probably not be earlier.

As noted above, RGPDI's drawback is that it only gets updated quarterly. For

example, the next RGPDI update won't happen until late-October. We therefore

need a shorter-term indicator to fill in the gaps, which is where the monthly

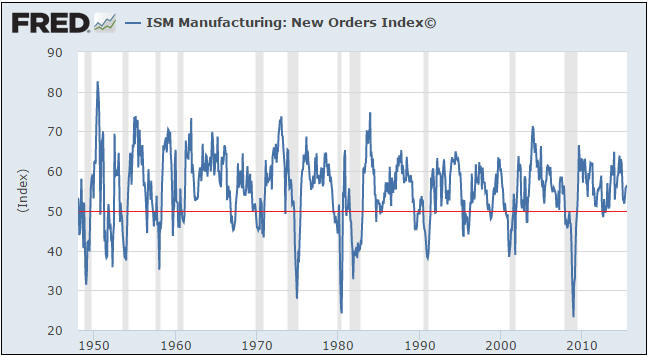

ISM (Institute of Supply Management) New Orders Index comes in.

With one exception, the ISM New Orders Index has turned down and broken solidly

below 50 ahead of every US recession of the past 65 years. The one exception was

1973-1974, when this index didn't break solidly below 50 until after the

recession was well underway. As a recession indicator it has therefore generated

only one false negative. However, it does generate the occasional false

positive, meaning that sometimes it breaks solidly below 50 and a recession does

not soon follow. We count 9 such instances in the index's long history.

The historical record therefore suggests that a) when the ISM New Orders Index

breaks solidly below 50 (to 48 or lower) there is a better than even-money

chance that the US economy has either just entered a recession or will enter a

recession within the ensuing few months, and b) when the ISM New Orders Index is

comfortably above 50 there is only a small probability that the US economy has

entered or will soon enter recession territory.

The latest monthly ISM data were released early this week and showed that the

New Orders Index ticked up from 56.0 to 56.5 in July. This tells us that the US

economy is not currently in recession and is unlikely to enter a recession in

the near future.

We realise that other economic statistics are at levels that would typically be

associated with a recession and that the US economy is most definitely not doing

well at this time (which is hardly surprising given the Fed's relentless

distortion of interest rates and other price signals). Due to the weakness being

exhibited by other economic indicators we would be willing to discount the

message of the ISM New Orders Index if not for the fact that the New Orders data

are consistent with RGPDI, the most reliable of all recession indicators.

Our conclusion is that the US economy is lacklustre, but is still growing and

probably at least a few months away from entering its next recession.

The commodity bust in

two charts

We normally use the Continuous

Commodity Index (CCI) as our proxy for commodity prices in general. The CCI and

the CRB Index data are identical prior to 2005, but in 2005 the CRB's

composition was changed. We prefer the CCI to the CRB simply because the CCI

reflects the price performance of an unchanged basket of commodities.

In the latest Weekly Update we showed that the "inflation"-adjusted CCI had just

fallen to its lowest level since the 1940s. This is bad enough, but the CRB

Index has actually fared even worse. As illustrated below, the CRB Index is not

far from a 30-year low in nominal dollar terms. More specifically, the nominal

(meaning: not adjusted for the effects of inflation) CRB Index is now testing

its 1986, 1992 and 2009 lows and is within 10% of its 1999-2001 low.

Our second commodity-related chart shows that the XAU, an index dominated by a

few large gold-mining stocks and one large copper-mining stock (FCX), is now

below its 1986 and 1998 lows and is within spitting distance of its

November-2000 all-time low.

These charts prompt the following comments:

1) In the commodity markets and the gold-mining sector we are getting another

lesson about the weakness of market sentiment as an indicator: when it comes to

sentiment, there are no absolute benchmarks. The related lesson is that the most

extreme monetary intervention in history can lead to new sentiment extremes in

both directions. Does this mean that the flipside of the current situation will

be equivalent extremes in the opposite directions within the coming few years?

Yes, it probably does.

2) There's a high probability that the global consumption of commodities will be

higher in 5 years' time than it is today and there's no chance that the entire

gold-mining industry is heading for the financial scrapheap. Given these

realities and current price levels, does it make more sense to be bullish or

bearish regarding the prospects for commodity and gold-stock prices over the

coming few years?

The Stock Market

The US

We saw the following chart in a

post at Ritholtz.com. It isn't directly related to the stock market, but we

are reproducing it here because a) it is interesting and b) nothing worthy of

comment happened to the senior stock indices over the past few days.

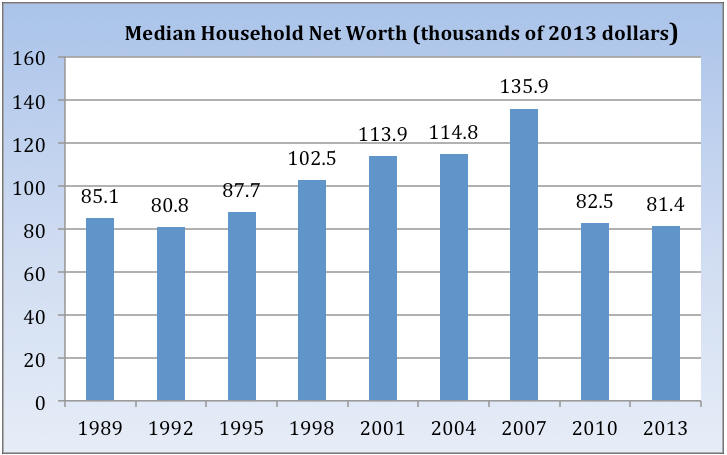

The chart was put together by David Rosenberg using data from the Federal

Reserve's Survey of Consumer Finances (SCF). These data are only published every

three years, which is why the latest bar on the chart is for 2013.

We knew that the stock market's large gain was unrepresentative of the average

American's financial performance, but we were shocked by the magnitude of the

disparity revealed by this chart. The chart shows that in constant dollar terms*

the net worth of the median US household fell by about 40% from 2007 through to

2013 and was a little lower in 2013 than it was way back in 1989. In contrast,

from the end of 1989 through to the end of 2013 the CPI-adjusted S&P500 Index

rose by about 170%.

In other words, the constant-dollar net worth of the median US household fell

slightly over a 24-year period during which the constant-dollar S&P500 gained

about 170%. It takes a lot of monetary meddling to generate a wealth-performance

mismatch of this magnitude. Take a bow, Greenspan, Bernanke and Yellen.

*We assume that the Fed uses the official CPI or something

similar to adjust for "inflation".

Gold and the Dollar

Gold

The monthly US Employment Report has an effect on the financial markets in

general and the gold market in particular that is way out of proportion to the

usefulness of the information contained in the report. The reason for the

outsized effect is that the economics illiterates who run the Fed place a lot of

importance on the monthly employment data.

The next monthly Employment Report will be published prior to the start of US

trading this Friday. As we've previously mentioned, it's prudent not to have any

leveraged short-term gold positions -- either long positions or short positions

-- when this report is published, because the gold-price action tends to be

volatile and unpredictable in the immediate aftermath of the report.

Having said that, the following table (an update of the table that was presented

and discussed in detail in our 4th May 2015 weekly commentary) shows that the

last four monthly Employment Reports were associated with minimal volatility in

the days leading up to the report and on the day of the report.

| Date of Employment Report | Gold price at end of day before report | Gold price 6 trading days before report | $ difference (neg means fell during 5 days before rpt) | Gold price at end of Empl Rpt day | $ chge on Empl Rpt day |

| 07-Aug-15 | 1087.3 | ||||

| 02-Jul-15 | 1167.8 | 1174.2 | -6.4 | 1165.2 | -2.6 |

| 05-Jun-15 | 1176.4 | 1188.6 | -12.2 | 1171.8 | -4.6 |

| 08-May-15 | 1183.8 | 1183.5 | 0.3 | 1187.2 | 3.4 |

| 03-Apr-15 | 1202.5 | 1203.6 | -1.1 | 1214.5 | 12 |

| 06-Mar-15 | 1197.5 | 1209.3 | -11.8 | 1168.2 | -29.3 |

| 06-Feb-15 | 1265 | 1258.7 | 6.3 | 1233.3 | -31.7 |

| 09-Jan-15 | 1183.2 | 1208.9 | -25.7 | 1223.4 | 40.2 |

| 05-Dec-14 | 1198.1 | 1206 | -7.9 | 1192.6 | -5.5 |

| 07-Nov-14 | 1199 | 1141.3 | 57.7 | 1178.7 | -20.3 |

| 03-Oct-14 | 1222.5 | 1214.8 | 7.7 | 1191.1 | -31.4 |

| 05-Sep-14 | 1290 | 1261.7 | 28.3 | 1269.3 | -20.7 |

| 01-Aug-14 | 1294.2 | 1283.1 | 11.1 | 1295.2 | 1 |

| 03-Jul-14 | 1319.3 | 1328 | -8.7 | 1320.4 | 1.1 |

| 06-Jun-14 | 1254.6 | 1253.2 | 1.4 | 1252.4 | -2.2 |

| 02-May-14 | 1290.6 | 1284.7 | 5.9 | 1300.7 | 10.1 |

| 04-Apr-14 | 1291.3 | 1286.6 | 4.7 | 1302.3 | 11 |

| 07-Mar-14 | 1331.7 | 1350.4 | -18.7 | 1339.9 | 8.2 |

| 07-Feb-14 | 1243.3 | 1258.1 | -14.8 | 1267 | 23.7 |

| 10-Jan-14 | 1222.3 | 1226.8 | -4.5 | 1248.5 | 26.2 |

| 06-Dec-13 | 1237.4 | 1224.3 | 13.1 | 1230 | -7.4 |

| 08-Nov-13 | 1322.5 | 1307.2 | 15.3 | 1289 | -33.5 |

| 22-Oct-13 | 1272.8 | 1315.7 | -42.9 | 1340.3 | 67.5 |

| 06-Sep-13 | 1406.8 | 1367.3 | 39.5 | 1391 | -15.8 |

| 02-Aug-13 | 1333 | 1308.8 | 24.2 | 1312.8 | -20.2 |

| 05-Jul-13 | 1224.3 | 1251.5 | -27.2 | 1212.7 | -11.6 |

| 07-Jun-13 | 1412.7 | 1412.1 | 0.6 | 1384.3 | -28.4 |

| 03-May-13 | 1466.3 | 1467.6 | -1.3 | 1469.9 | 3.6 |

| 05-Apr-13 | 1597.1 | 1553.3 | 43.8 | 1580.8 | -16.3 |

| 08-Mar-13 | 1579.8 | 1577 | 2.8 | 1576.4 | -3.4 |

| 01-Feb-13 | 1667.7 | 1664.7 | 3 | 1557.6 | -110.1 |

| 04-Jan-13 | 1663.8 | 1664 | -0.2 | 1658.4 | -5.4 |

| TOTAL | 82.3 | -192.4 |

There has been minimal volatility in the gold price over the past few days, with

the price oscillating between the low-$1080s and the $1090s. However, this

'coiling' sets the stage for a breakout in one direction or the other in

reaction to the employment data. In fact, strong data could possibly result in

breakouts in both directions -- a downside breakout in a knee-jerk reaction to

the news followed by a reversal and a subsequent upside breakout.

Gold Stocks

Despite the directionless trading in the gold market, the gold-mining indices

extended their declines over the first three days of this week. This is

extraordinary considering the extent to which they were already stretched to the

downside.

Part of the problem is that the senior gold producers continue to report poor

operational performances. The rest of the problem is sentiment. For example,

electric car manufacturer Tesla (TSLA) hemorrhages cash quarter after quarter,

but up until now the stock market has rewarded this company with a very high

valuation because it likes the story. The gold story, on the other hand, is

extremely unpopular at the moment.

This week's price action has maintained the HUI/gold ratio extreme that we

mentioned in the 27th July Weekly Update. We are referring to the fact that the

HUI/gold is at the bottom of its 40/20 MA envelope (a 20% envelope around the

40-day MA), a very rare occurrence. It happened at the bottom last November and

near important bottoms in 2008, 2002 and 1998. Here's the relevant chart again.

Over the past three months the junior gold stocks have generally held up better

than the senior gold stocks. This has enabled GDXJ to remain above its July low

for now and caused the upward trend in the GDXJ/GDX ratio illustrated by the

bottom section of the following chart. However, relative strength is small

consolation when it involves substantial absolute weakness.

Although it could happen, we do not expect to see a bullish divergence between

the gold-mining indices and gold bullion prior to an important price low.

Bullish divergences, entailing the gold-stock indices making higher lows while

the gold price makes a new low, tend to occur around short-term or

intermediate-term correction lows within cyclical bull markets. At major lows

the gold-stock indices tend to be relatively weak until the day of the final

bottom, at which point they become relatively strong. For example, based on the

performance of the HUI/gold ratio the outlook for gold-mining looked dismal the

day before the major bottom in November-2000.

The Currency Market

Not much has happened of late in the currency market. The euro, for example,

continues to chop around just above its lows of the past three months. It needs

to close above 111 or below 107.5 to signal the most likely direction of its

next multi-week move.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://research.stlouisfed.org/

![]()