![]()

![]()

![]()

![]()

- Interim Update 6th March 2019

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Base metals in short

supply

The reported LME (London Metal

Exchange) inventory for a base metal such as copper is not a reliable

indicator of the overall supply situation for that metal. This is because

there is a lot of supply outside the reporting warehouses and because

reported inventory levels can be manipulated by large traders to paint a

misleading picture. However, when LME inventory levels are very low for

all major base metals at the same time, as is the case right now, it most

likely does indicate a tightness of supply.

The following charts

show that the LME warehouse stocks of copper, lead, nickel and zinc are at

or near 5-year lows. Furthermore, the LME warehouse stocks of these metals

are at all-time lows when measured in terms of days of global consumption.

Base metal prices rebounded over the first two months of this year,

partly in response to the low LME inventory levels. A good example is the

copper price, a daily chart of which is displayed below. The copper price

made a marginal new 12-month low at the start of January and then began to

rally.

We expect the combination of a US-China trade deal,

tightness of supply, stock-market stability and a modicum of US$ weakness

to fuel significant additional price gains over the next three months.

As a group, the stocks of base metal producers are currently

'overbought' and acutely vulnerable to near-term weakness in the broad

stock market. In other words, they likely will experience sizable

pullbacks if there's a significant correction in the broad market in the

near future. Given that there probably will be a significant correction in

the broad market in the near future, this is not a good time for new

buying of base metal equities. However, a new buying opportunity could

emerge before the end of this month.

The Stock Market

A long-term valuation

indicator turns down from an extreme

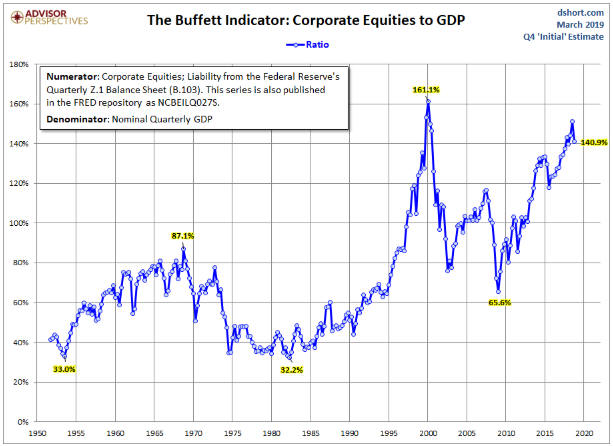

The total market

value of US equities relative to US nominal GDP is called the Buffett

Indicator (BI), because Warren Buffett expressed a liking for it at some

point in the distant past. In Q3-2018 the BI reached a level that was only

ever exceeded at the Q1-2000 bubble top. It then reversed course in

Q4-2018, perhaps marking Q3-2018 as a major valuation peak.

We have two reservations about the BI. The first is that it relies on

GDP, and GDP is not a meaningful economic statistic. The second is that

even if GDP were a valid measure of the US economy's size, it wouldn't

make sense to focus on the market value of US corporate equity relative to

US GDP. The reason is that a lot of US corporate revenue is generated

outside the US. Furthermore, the portion of US corporate revenue that gets

generated outside the US is increasing.

Due to the aforementioned

reservations and the fact that the Q4-2018 reversal in the BI could just

as easily be a 2015-style bull-market correction as the initial decline in

a bear market, we wouldn't hang any hats on the recent performance of this

long-term indicator. We are presenting it for interest's sake only.

Current Market Situation

The SPX pulled back

from lateral resistance over the first three days of this week after first

spiking to a marginal new high. The NYSE Advance-Decline Line (shown in

the lower section of the following chart) remains close to its all-time

high, so this could be nothing more than a minor multi-day consolidation.

However, as discussed below we suspect that it will turn out to be the

start of a meaningful decline.

Apart from the senior stock indices being stretched to the upside on a

short-term basis and near/at critical resistance levels, the recent

performances of the Dow Transportation Average (TRAN) and the Russell2000

SmallCap Index (RUT) suggest that the long-awaited multi-week correction

has finally arrived.

As illustrated by the first of the following

daily charts, TRAN has been moving downward for about two weeks. This is

significant because TRAN tends to lead the senior indices at important

turning points. As illustrated by the second of the following charts, RUT

has reversed course in a decisive manner after testing its 200-day MA.

We continue to expect a sizable multi-week pullback followed by a move

to a new high for the year during the second quarter.

Gold and the Dollar

Gold

From the "Gold" section of the latest Weekly Update:

"A

short-term rise to the $1400s will remain a good bet provided that

trend-defining support holds during any further corrective activity and

there isn't a pronounced bearish shift in the true fundamentals.

Trend-defining support lies at $1240, but we think that the 200-day MA

will limit the downside over the weeks ahead. Currently, the 200-day MA is

near $1250."

The US$ gold price extended its decline over the

first three days of this week and in doing so broke below its 50-day MA

(the blue line on the following chart). This increases the probability

that a test of the 200-day MA (near $1250) will occur before the

correction is complete.

Of importance to the short-term prospects of both gold bullion and the

gold-mining sector, the HUI/gold ratio remains above its 40-day MA. Refer

to the following chart for the details. Be aware, though, that it would

take only a small amount of additional weakness in the HUI relative to

gold to push HUI/gold below this demarcation line.

If HUI/gold

breaks below its 40-day MA it won't imply that a large decline is

underway, but it will be more evidence that we are dealing with a

counter-trend rebound and not a new bull market.

Gold Stocks

The Gold Miners ETF (GDX) showed

some resilience over the first two days of this week, but then fell far

enough on Wednesday to close marginally below its 50-day MA. From our

perspective this didn't change anything, as we expect a test of support at

$20.50-$21.00 prior to the end of the current correction.

On a long-term basis the gold-mining sector is counter-cyclical and

tends to perform well when the broad stock market is weak, but there are

times when the gold-mining sector is vulnerable to weakness in the broad

stock market. Because the gold-mining indices rose with the senior US

stock indices from mid-January until the second half of February, now is

one of those times.

The Currency Market

Over the past several months most of the major currencies have been

buffeted about by news but have not managed to sustain moves in either

direction. In essence, they have been trendless. Here are three examples:

The euro has traded in a very narrow range since mid-October. It has

been weighed down by the risk of imminent recession in some important

European economies, relative weakness in European equities and the

increasingly-likely possibility that the ECB will delay its first rate

hike until 2020. At the same time, it has been buoyed by the US Fed's

change of heart and a bounce in German bond yields relative to US bond

yields.

Later today the euro will react to the outcome of an ECB

meeting, which probably will involve reacting to news that the ECB intends

to introduce a new Targeted Longer-Term Refinancing Operation (TLTRO - a

program designed to promote increased bank lending).

The British Pound has been dominated by Brexit-related news. Since the

start of this year it has strengthened as the chances have improved that

either a slightly-modified Withdrawal Bill will be approved by parliament

or Brexit will be delayed beyond the 29th March deadline, that is, as the

probability of a no-deal Brexit has fallen. However, the lessening risk of

a 'hard Brexit' wasn't enough to break the Pound out of its 8-month range.

Next week is shaping up to be very important for the Pound, as it

could contain as many as three separate Brexit-related votes in the

British parliament. The tentative schedule is for: A vote on 12th March to

approve a modified Withdrawal Bill (essentially the same bill that failed

to gain approval in December, but perhaps with added wording regarding the

"Irish

backstop"). If that fails, a vote on 13th March to approve a no-deal

exit from the EU. And if that fails, a vote on 14th March on whether to

postpone the date for leaving the EU.

If the third vote is

successful, the risk (from the perspective of the pro-Brexit camp) is that

the delay will be used to hold another referendum.

The uncertainty

regarding Brexit makes it difficult to buy the Pound, but we continue to

think that the currency's intermediate-term risk/reward is skewed towards

reward.

The Australian dollar (A$) has been trying to bottom since October.

There was an attempt to establish an upward trend in November that failed

in December in response to extreme weakness in the prices of industrial

commodities. A second attempt to establish an upward trend failed in

February in response to the feared economic ramifications of political

conflict between Australia and China.

The aforementioned conflict

began with last year's decision by the Australian government to ban

China-based Huawei, the world's largest supplier of telecoms equipment,

from being involved in the roll-out of Australia's 5G network. It also

encompasses allegations of Chinese spying on Australian politicians. Quite

possibly -- albeit not officially -- in retaliation to the actions of the

Australian government, at the beginning of February news hit the wires

that

the Chinese government had imposed restrictions on Australian coal at

the northern Chinese port of Dalian. This was potentially important

because coal is Australia's largest export (in dollar terms) and buyers in

China are collectively the biggest customers of Australia's coal

producers. Then, to make matters worse, about 1.5 weeks ago

China's government announced that it was preparing to slap hefty tariffs

on barley imported from Australia.

A disproportionately large chunk

of Australia's total exports go to China, so any crimping of trade between

the two countries could weaken both the Australian and Chinese economies.

Therefore, it isn't surprising that the coal and barley news put downward

pressure on the A$. Adding to the downward pressure on Wednesday of this

week was news that Australia's GDP growth rate was lower than expected

during the latest quarter.

However, it's bullish that the recent

stream of bad news failed to push the A$ below the bottom of its 6-month

trading range.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://www.kitco.com/

![]()