![]()

![]()

![]()

![]()

- Interim Update 6th May 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Oil and Gas (O&G)

O&G production is

adjusting to the new reality

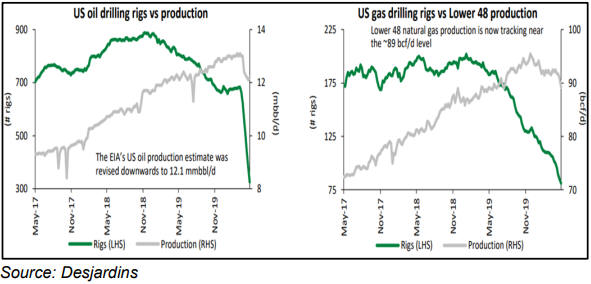

The

latest

President's Report from Peyto (PEY.TO), a mid-tier natural gas

producer, included the following charts comparing US oil and gas (O&G)

production with the number of drilling rigs in operation. Production has

declined, but the recent collapse in the quantity of drilling rigs means

that there will be a much greater decline in production over the months

ahead.

O&G demand should begin to recover over the next few months as

businesses reopen and people return to work. This demand recovery combined

with the now-entrenched downward trend in production should mean that

production and consumption move back into balance in the not-too-distant

future, after which inventories should start being drawn down.

The

coming inventory draw-down will remove the upward pressure from oil

storage prices, but inventory levels and the associated storage costs

probably will remain elevated for at least a few more quarters.

Consequently, we expect that the oil futures market will have a

larger-than-usual contango* for many months to come and that tanker

companies will generate much better earnings than the market currently

expects over the coming 12 months.

We haven't yet 'pulled the

trigger' on the tanker trade that was discussed in the 22nd April Interim

Update and the 27th April Weekly Update, but we suspect that a good

opportunity to do so will arrive by the end of this month. The optimum

time to buy the tanker stocks probably will be around the time that the

oil price recovery 'runs out of steam'.

*Meaning

that the spot price will remain further than usual below the nearest

futures price and the nearby futures contracts will trade at

larger-than-usual discounts to contracts will later expiry dates.

The recent price action

On Monday 20th April

the world was shocked when the expiring May-2020 NYMEX oil futures

contract plunged well into negative territory. The day after this

happened, the June-2020 oil futures contract plummeted from above $20 to a

low of $6.50. A rebound then began.

The rebound in the June-2020

contract was spectacular, with the price almost quadrupling from its 21st

April low of $6.50 to its 6th May high of $26.08. Very few people would

have been able to take advantage of this dramatic recovery, though,

because the only way to do so was by purchasing oil for June-2020

delivery, which would have been a very risky thing to do for anyone who

didn't have the capacity to store the oil.

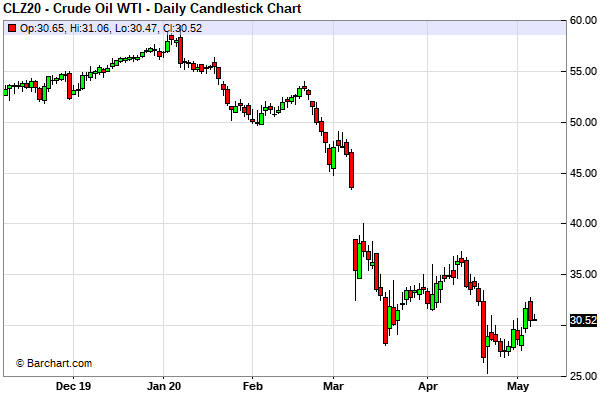

As illustrated by the

following daily chart, the rebound in the December-2020 oil futures

contract was far less substantial. This contract bottomed at $25.31 on

22nd April and has since traded as high as $32.77, for a trough to peak

gain of about 30%.

We won't be surprised if the December-2020 oil

contract moves up to the $36-$38 range within the next few weeks, but we

doubt that it will do significantly better than that before downward

forces reassert themselves.

It's possible that April-2020 will turn

out to be the cycle low for oil, but a lot will depend on the speed at

which the global economy reopens and the extent to which the stock market

retraces its March-May rebound.

We got more evidence (in the form of a sharp rise to the 200-day MA)

during the first two days of this week that the natural gas (NG) market

made a multi-month price low (potentially a cycle low) in early April. The

next pieces of the puzzle that must fall into place are a brief correction

that holds at/above the 50-day MA (currently near $1.80) and then a daily

close above the 200-day MA.

The Stock Market

Current Market Situation

The conflict between the US and China governments was 'put on the

backburner' late last year when the Phase 1 trade deal was done. It

remained a long-term risk, but it was eliminated as a short-term threat.

However, with the US government now seemingly intent on holding China's

government accountable for the COVID-19 pandemic, the conflict has

returned to centre stage.

The Trump team claims to have evidence

that the new coronavirus leaked into the wide world via an accident at a

laboratory in Wuhan, but it has not shown this evidence to any US allies

or any impartial authority. This probably means that there is no such

evidence, just reasons to be suspicious. China's government, of course,

has denied that the virus escaped from one of its own labs and is using

its giant propaganda machine to portray the Trump claim as a

politically-motivated, anti-China lie.

We have no idea what the

truth is here. First, we have no trouble believing the story that the

virus made its way into the world due to inadequate safety/security

measures at the Wuhan Institute of Virology. After all, it is a fact that

bat coronaviruses were being studied at this facility. At the same time,

the story that the virus jumped from animals to humans at a 'wet market'

in Wuhan is also very plausible. After all, history is littered with

examples of pandemics caused by viruses making the leap from animals to

humans.

Regardless of the truth, if the conflict continues to

escalate it will be, from the economy's perspective, like kicking a downed

man. It is the last thing that the US economy and the global economy need

right now.

At the moment, the stock market is ignoring the economic

risk posed by the potential escalation of the US-China conflict. It also

appears to be ignoring the fact that central bank money and credit

creation cannot replace lost production. All the central bank can do is

boost the prices at which the remaining production is sold.

At this

stage, the post-crash rebound high for the SPX is last week's high near

2950. A reversal has not been signalled yet, so last week's high could be

exceeded within the next couple of weeks. However, anything more than a

marginal break above last week's high is unlikely prior to the start of a

meaningful correction.

The start of a meaningful correction would

be confirmed by a break below the 50-day MA, but a daily close below 2800

could be taken as an early warning that a downward reversal is in the

works. A daily close below 2800 would break the SPX below its 20-day MA

and the channel drawn on the following daily chart.

A normal correction would retrace up to half of the preceding rally.

This means that if last week's high turns out to be the rebound peak then

a normal correction could result in the SPX dropping back to the 2550-2600

range.

In the latest Weekly Update we wrote that for new bearish

speculations it would make sense to focus on some of the sectors/groups

that were relatively weak during February-March. Good examples are the

transportation sector, as represented by IYT (the Transportation ETF), and

the small-cap end of the market, as represented by IWM (the Russell2000

SmallCap ETF).

The following daily chart shows that the Dow

Transportation Average (TRAN) has dropped below its 50-day MA and that the

TRAN/SPX ratio has just made a new 12-month low. This suggests that even

if the SPX experiences nothing more bearish than a normal correction

within the next couple of months, there is a good chance that TRAN will

test its March low.

The next daily chart shows that there was a sharp rise in the

Russell2000 SmallCap ETF (IWM) during the first three days of last week

that took the ETF well above its 50-day MA, and then a plunge that fully

retraced the sharp rise. It looks like a short-term top is in place for

the IWM, but as is the case with the SPX a daily close below the 50-day MA

is required to confirm a short-term trend reversal.

Bearish speculations and hedges

In the latest

Weekly Update, we wrote:

"...it would be reasonable for

experienced option traders to purchase IYT and/or IWM put options with

expiry dates in August-2020 or later during market rebounds over the

coming fortnight. Traders/investors who aren't experienced with options

could purchase bear funds or simply raise cash."

Traders/investors also could choose to tighten their stops, if that is

their preferred method of risk management.

In our own account,

there are some SPY $230 put options expiring in June-2020 that were

purchased 2-3 weeks ago and some IWM $100 put options expiring in

October-2020 that were purchased on Tuesday of this week. Our plan is to

sell the SPY puts within the next four weeks, ideally following a decline

in the SPX to 2600 or lower, and to buy more IWM put options during the

next two weeks, ideally on strong days for the underlying ETF.

In

the TSI Stocks List we have the SPY $230 put option that expires on 19th

June 2020 and we will add the IWM put option mentioned above if it trades

at US$4.00 (it ended Wednesday's session in the US$4.80s).

Note

that stocks and options are either 100% in or 100% out of the TSI List,

but when managing money it often makes sense to scale into and out of

positions. The scaling process lessens the need to be accurate with

short-term timing.

Gold and the Dollar

Gold

The

US$ gold price has pulled back to support near $1690, again. As long as

this support holds, the door will remain open to another new multi-year

high prior to a short-term top. Decisively breaching this support would

signal that a short-term top is in place.

Below is the weekly gold/SPX chart that we use as the primary

indicator of long-term gold trends. On this chart, gold bull markets are

signalled by a cross from below to above the 200-week MA (the blue line)

and gold bear markets are signalled by a cross from above to below the

200-week MA. Over the past 30 years there was one false signal, which

occurred as a result of the 1987 stock market crash.

The 200-week

MA crossover that occurred in March-2020 confirmed that a gold bull market

began in Q3-2018. Considering that this signal was the result of a

1987-style stock market crash, there is a risk that it will prove to be

false. This risk will be eliminated if gold/SPX achieves a weekly close

above its March-2020 high.

Silver

Since the second week of April the US$

silver price has drifted lower beneath its 50-day MA. From its current

level it would have to gain $1-$2 to create a short-term selling

opportunity or lose $1-$2 to create a short-term buying opportunity.

Gold Stocks

In mid-March the HUI/gold ratio

reached the bottom of a 25% moving-average envelope around its 40-day MA.

As we pointed out at the time (refer to the 16th March Weekly Update),

this suggested that a strong rebound was about to begin.

In the

27th April Weekly Update we included an update of the same chart to show

that there had been a shift of almost 180 degrees, in that the HUI/gold

ratio had almost reached the top of the same envelope. We concluded: "Although

this shows that the gold mining sector is now 'overbought' relative to

gold bullion, the historical record suggests that it is more a sign of

strength than a reason to be worried. In this respect it is similar to the

surge in the broad stock market's McClellan Oscillator."

Due

to some additional strength in the HUI relative to gold over the ensuing

1.5 weeks, the 180-degree shift is now complete. As illustrated below, the

HUI/gold ratio hit the top of its MA envelope during the first half of

this week.

On an intermediate-term basis the HUI/gold ratio's 'overbought'

condition is bullish. The historical record tells us that when the

HUI/gold ratio becomes very stretched to the upside within two months of a

multi-year low, the gold sector is in the early part of a 6-12 month

upward trend. Something similar happened in early-2016, late-2008,

early-2002 and early-2001. In each case, the HUI went on to trade much

higher within the ensuing 12 months.

On a short-term basis the gold

sector is due for a significant correction. The HUI is stretched to the

upside and testing long-term resistance defined by its 2016 top. If it

were to break above this resistance without some intervening corrective

activity then it would be even more stretched to the upside, which

obviously wouldn't improve the short-term risk/reward. On the contrary, it

would increase the risk of a failed upside breakout.

Given that the

gold sector has rallied with the broad stock market over the past several

weeks, it's reasonable to expect that gold mining stocks would get dragged

down by a sizable decline in the broad market. Not, however, to the extent

that they were dragged down during March. Due to the obviously bullish

gold mining fundamentals, we suspect that even if the SPX were to revisit

its March low within the next two months the HUI wouldn't go significantly

lower than 200.

For the HUI, a normal correction would end near

lateral support at 220 or the 50-day MA (227 and rising).

The Currency Market

The Dollar Index (DX) has

rebounded from the bottom of its recent range, but the pattern is

unchanged. A triangle continues to form.

The DX's short-term

pattern is beginning to look more like a mid-trend consolidation than a

reversal, which implies that the pattern is more likely to end in a

downside breakout than an upside breakout. A downside breakout from the

triangle would suggest a target of around 96.

As previously

mentioned, a downside breakout would be signalled by a daily close below

98.7 and an upside breakout would be signalled by a daily close above

101.0.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://www.barchart.com/

![]()