![]()

![]()

![]()

![]()

- Interim Update 6th June 2018

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Industrial metals in

rally mode

Copper breaks out to the

upside

In the 28th May Weekly Update under the heading

"The copper market is coiling", we wrote:

"The copper price is

working its way into the apex of the triangle drawn on the following daily

chart. For this coming week, a daily close above $3.15 or below $3.05

would be a breakout from this 'coiling' pattern.

A daily close

above $3.15 would suggest that copper was on its way to new multi-year

price highs. A daily close below $3.05 would point to a re-test of

intermediate-term lateral support at $2.95, but triple bottoms are rare so

it's likely that the next test of this support will fail."

The

copper price broke out of its 'coiling pattern' to the upside on Tuesday

of this week and then built on its breakout on Wednesday. This suggests

that significant additional gains will be made within the coming two

months, although with the market now short-term 'overbought' we won't be

surprised if a 1-2 week top is put in place this week.

Zinc resumes its bull market

Early this year

the per-pound zinc price traded in the US$1.60s -- its highest level in

more than 10 years. It then pulled back and last month it broke below

support at US$1.40 to reach its lowest level since August-2017. This

prompted us to ask (in the 7th May Weekly Update): Is this a normal

correction or the start of a major decline?

Our answer was: "At

this time there's no way of knowing ... but given the continuing bullish

term structure in the LME futures market we think it will turn out to be a

normal correction of similar magnitude to the correction that occurred

during the first half of last year. If so, the short-term downward trend

has almost run its course."

The price has since recovered to the mid-US$1.40s. This is a

preliminary sign that the downward correction has ended.

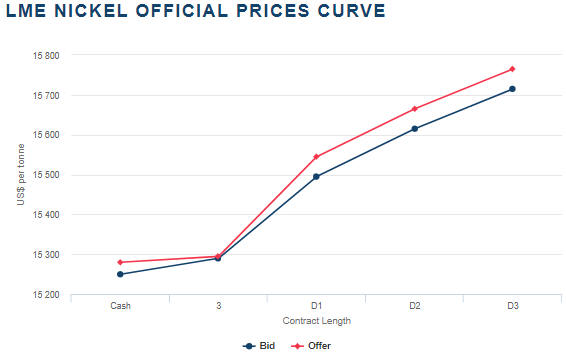

EV-related speculation boosts nickel

The nickel price has

trended upward since July of last year and during the first half of this

week reached its highest level since late-2014.

The rally in the nickel price has been driven in part by the

substantial decline in the reported LME nickel inventory that began in

November of last year. Refer to the following chart for details. The

decline in this high-profile inventory creates the impression that

physical supply is becoming tight relative to demand.

The impression of a growing nickel shortage is most likely false,

because the upward slope of the LME futures curve (see below) indicates

that the market is well supplied. Instead of a tightening supply

situation, what could be happening here is the relocation of physical

nickel from reported to unreported inventory as part of an attempt to

manipulate the price upward. In any case, the declining LME inventory

provides a 'fundamental' justification for bullish speculation.

Another fundamental justification for bullish nickel speculation is

the rise in nickel demand that will stem from the increasing popularity of

electric vehicles (EVs). The cathodes of most lithium-ion EV batteries are

made from nickel, cobalt and either manganese or aluminium, and due to the

potential problems with future cobalt supply there is a major effort by

battery manufacturers to simultaneously reduce the amount of cobalt and

increase the amount of nickel. For example, Tesla's latest shareholder's

letter states:

"Cells used in Model 3 are the highest energy

density cells used in any electric vehicle. We have achieved this by

significantly reducing cobalt content per battery pack while increasing

nickel content and still maintaining superior thermal stability. The

cobalt content of our Nickel-Cobalt-Aluminum cathode chemistry is already

lower than next-generation cathodes that will be made by other cell

producers with a Nickel-Manganese-Cobalt ratio of 8:1:1."

Even

if most EV battery manufacturers can get the cobalt percentage in their

cathodes down to 10% or lower, as Tesla is claiming to have done, it's

likely that the price of cobalt will have to move a lot higher over the

next few years to maintain the supply-demand balance. However, the nickel

mining industry is shaping up to be the main beneficiary of the drive to

reduce the cobalt content of EV batteries.

TSI exposure to

industrial metals

Currently, the TSI Stocks List has

exposure to nickel via Clean TeQ Holdings (CLQ.AX, CLQ.TO) and, to a

lesser extent, Cobalt 27 Capital (KBLT.V). Nevsun Resources (NSU) provides

the only exposure to copper and zinc.

Oil breaks out to

the downside

About two weeks ago (in the 28th

May Weekly Update) we wrote: "...we think that the largest oil-market

correction since mid-2017 has begun. At this time the most plausible

target for a correction low is lateral support near $58."

The

oil price has since broken below its 50-day MA and short-term lateral

support at $66.50.

Intermediate-term lateral support near $58 is still the most plausible

target for a correction low, but the market is now a little 'oversold'.

Our guess is that it will rebound by a few dollars from whatever low is

made this week before resuming its downward trend.

The Stock Market

Current Market Situation

Over the past two weeks it looked as if the NASDAQ100 Index (NDX) was

preparing to test its year-to-date high. The test has just happened.

The NDX actually made a new all-time high on Wednesday 6th June, but

at this time the rise into new-high territory is too marginal to be

classed as a breakout. Furthermore, the NDX is now short-term

'overbought', so there's a good chance that this week's marginal new high

will be followed by a 1-2 week consolidation.

A routine

consolidation would do no more than take the price down to around 6900.

A decline that is more serious than the Q1-2018 correction probably

will begin during the second half of this year. At least, that's what we

expect. Also, it's possible that this larger decline will begin from a

July high, but a downturn that is more than a short-term correction should

be preceded by 'market internals' diverging bearishly from the senior

indices.

There is no sign of such a divergence at this time, so

there is no good reason, yet, to prepare for a large decline in the US

stock market.

Tesla (TSLA) Update

A few

weeks ago we wrote that while it still appeared that bankruptcy was

Tesla's long-term destination, the short-term risk/reward no longer

favoured the bears and it no longer made sense to be short the stock.

The main problem for bearish TSLA speculators was that the short

position had become so large that there was regular support from short

covering and no room for new shorts to get involved in a big way (you

can't sell short if you can't borrow the stock). Moreover, there would be

an uncomfortably (for short sellers) high risk of a strong rebound as long

as support in the mid-$270s continued to hold. The support we are

referring to is defined by the bottom of the channel drawn on the

following daily chart.

Support was successfully tested again about

two weeks ago and the price then began to crawl upward. The crawl turned

into a sprint on Wednesday of this week when the stock price gained 10% in

response to the positive vibe generated by the company's shareholder

meeting.

When the short position is massive it doesn't take much in

the way of good news to precipitate a rapid price rise.

We may be interested in placing a new bet against TSLA (via put

options) within the next few weeks, but now is not the right time.

Gold and the Dollar

Gold

Since returning to former support (now resistance) at $1309-$1310, the US$

gold price has essentially marked time. However, there are signs that it

is beginning to strengthen. With reference to the following daily chart,

these signs are the upturn in the Price Momentum Oscillator (PMO) shown in

the lower section of the chart and the move above the top of a short-term

downward-sloping channel.

Gold must get above the aforementioned

resistance on a weekly closing basis to signal that a short-term bottom

was put in place last month.

Gold Stocks

The first of the following daily

charts shows that the HUI has been drifting lower within a 40-point

channel since early last year. The second chart shows that over the past 8

weeks the HUI has drifted lower within a 7-point channel. No wonder it

feels like nothing is happening in the gold-mining sector!

The 8-week downward drift looks like a consolidation within a

short-term upward trend. If this is the correct interpretation then within

the next few weeks the HUI should break out to the upside and quickly move

up to 190-200.

A quick move up to 190-200 by the HUI obviously

would be good for our gold-mining shares for a short time. However, a

rally that gets underway prior to a wash-out decline would have a high

risk of being just another rebound within the 17-months-and-counting

downward drift illustrated by the first of the above charts.

In any

case, we won't have to worry about the possibility that a near-term rally

to 190-200 is just another counter-trend rebound until the rally actually

happens. If it happens then we can review the facts at the time to

determine whether it is more likely to be a short-lived rebound or the

start of a much larger advance.

The Currency Market

The Australian dollar (A$) has broken above its 50-day MA and lateral

resistance at 0.765. This increases the probability that a multi-month

rally is underway. If so, then for the next couple of weeks the 50-day MA

should limit the downside during any 'corrective' activity.

We

expect that the 200-day MA, which is at 0.775 and slowly falling, will act

as a temporary obstacle on the way up.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Alkane

Resources (ALK.AX) reported the results of an

updated engineering and financial study on the Dubbo Project (DP), the

most recent previous study having been completed in 2015.

Alkane

Resources (ALK.AX) reported the results of an

updated engineering and financial study on the Dubbo Project (DP), the

most recent previous study having been completed in 2015.

The DP is

fully permitted and slated to produce zirconium, hafnium, niobium and

REEs. At current commodity prices the approximate revenue split would be:

Zirconia products: 46%

REEs: 34%

Niobium: 14%

Hafnium: 6%

The published results of the new study were disappointing, for three main

reasons:

1) The company had previously advised that using a

modularised construction process the pre-production capex could be reduced

and the economics could be improved. Specifically, in a press release in

October-2016 ALK advised that by using a modular construction method, with

much of the construction happening off site, it should be possible to

reduce the total capital cost of the DP from US$930M to US$840M and reduce

the up-front capital cost to US$480M. However, in the Staged Build plus

Modular Construction scenario considered as part of the latest study, the

total capex is estimated to be US$1.1B and up-front capital is estimated

to be US$610M. As a result, the economics of the staged/modular scenario

are worse than the economics of the base case scenario.

2) The

prices for the commodities that will be produced by the DP are on average

significantly higher now than they were when the 2015 study was completed,

leading to a 14% increase in the forecast annual revenue. However, the

profitability boost that should have stemmed from the higher selling

prices has been totally offset by higher operating expenses.

3) As

it did in the 2015 study, ALK only quoted the DP's pre-tax economics.

There was no mention of post-tax economics, but unless the company has

figured out a way to avoid paying tax it's the post-tax numbers that are

important.

Despite higher commodity prices and the financial

benefits that were expected to be achieved via a modular construction

approach, the estimated economics of the DP are almost identical now to

what they were three years ago. The most attractive scenario is the "Base

Case", which is the non-staged approach involving the construction of a

1Mtpa operation at a cost of A$1.3B. At the assumed commodity prices, this

scenario results in a pre-tax NPV(8%) and IRR of A$1.24B and 17.5%,

respectively.

There is nothing wrong with these numbers.

Furthermore, the A$1.24B NPV compares very favourably with ALK's current

enterprise value of around A$70M. The market reacted negatively, though,

because ALK's management had led 'everyone' to believe that the numbers

would be much better.

It would be impossible for a company of ALK's

size to fund the DP's A$1.3B capex without massively diluting the shares

and/or taking on an unwieldy amount of debt. However, it may be possible

to enlist a much larger company as a partner, with the larger company

funding the construction in exchange for a 50%+ stake in the project.

ALK's management is looking into doing exactly that, in that it

describes the top-priority funding solution as:

"Sale of

Project Interest to Strategic Investor: The Company continues to meet with

potential product off-take partners and investment funds with mandates

targeting investment in the key products of the Dubbo Project,

organisations considered to have the best strategic alignment with the

Company."

The other three funding options under consideration,

in priority order, are financing from Export Credit Agencies, traditional

equity and debt financing, and other financing methods such as selling

royalties and streams.

A positive aspect of the updated Study is

the leverage it reveals to changes in commodity prices. For example, if

all else remains the same then a 20% increase in selling prices boosts the

Base Case pre-tax NPV(8%) by almost 80% -- from A$1.3B to A$2.3B. This is

important because the prices of the DP's outputs should continue to trend

upward.

Although the worse-than-expected numbers in the updated DP

Study caused a 10% decline in ALK's stock price as opposed to the bounce

that we were hoping for, it remains clear that the per-share value of

ALK's assets is vastly greater than the current share price. There's huge

valuation-related upside potential, but realising this potential is going

to require more patience than originally expected.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.kitco.com/

http://www.lme.com/

![]()