|

- Interim Update 6th July 2005

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Is a rising oil price inflationary or deflationary?

Interestingly, both the

inflation and the deflation camps routinely portray a high and rising

oil price as being supportive of their respective cases. Those who are

anticipating ever-increasing amounts of inflation, for instance, argue

that the higher cost of energy will ripple through the economy and push

up prices across the board, whereas those who believe that deflation is

imminent argue that the higher cost of energy will restrict the

abilities of consumers and businesses to borrow and spend.

As usual, most participants in the debate talk as if inflation were an

increase in the general price level and deflation were a decrease in

the general price level, thus making the entire debate rather

meaningless. Inflation and deflation are purely monetary phenomena, so

a rising oil price is neither inflationary nor deflationary. It is

simply a rising price. The effect that this price rise has on the

economy will, in turn, be determined by the actions of the central

bank.

For example, in the situation where the central bank is taking steps to

reduce the rate of growth in the money supply then, all else being

equal, higher prices for energy will have to be offset by lower prices

in some other part of the economy. In this situation it is reasonable

to say that the rising oil price could have a deflationary effect

because under such monetary conditions, and with total private-sector

debt already at a very high level, it is probable that less money will

be borrowed into existence in the future. But all else is never equal

and it's distinctly possible that any reduction in private-sector

borrowing stemming from rising energy prices will be offset by an

increase in public-sector borrowing.

Now consider the example of a rising oil price in an environment where

the central bank is working to increase the rate of money-supply

growth. In this case the central bank will effectively be monetising

the increase in the oil price and there will likely be no associated

reduction in borrowing/spending. It wouldn't, however, be reasonable to

say that the rising oil price was inflationary since it would be the

central bank, not the oil market, that was driving the increase in the

money supply and the economy-wide reduction in the purchasing power of

money.

As things currently stand the Fed is acting to REDUCE the rate of

money-supply growth in the US, so the high/rising oil price will

potentially have a deflationary effect. We say "potentially" because,

thanks to the continuing housing-related borrowing frenzy associated

with long-term interest rates languishing near generational lows, it

hasn't YET had a deflationary effect. Of course, if the high cost of

energy did start to have a significant deflationary effect then the Fed

would do an about-face and begin to work towards increasing the

money-supply growth rate; so even in this case the probability of

deflation actually occurring would be extremely low.

Greenspan's last days

...the

Fed isn't likely to do anything different simply as a result of

Greenspan being in his final months as Fed chief. However, we expect

that the transition to someone new will have an adverse effect on

financial market confidence...

Alan Greenspan's term as a Federal Reserve governor ends early next

year, so unless a special arrangement is made to allow him to stay

longer there will be a new Fed Chairman in about 6 months time. This

raises the following questions: First, does Greenspan being in his

final months as Fed chief have any implications for US monetary policy

over the remainder of this year? And second, what will be the effect on

the financial markets of the transition from Greenspan to someone new?

There's a school of thought that Greenspan, concerned about how he will

be remembered, will do whatever he has to do to ensure that the US

economy and stock market appear to be in good shape on the day he hands

over the reins at the Fed. We don't have a lot of time for this view,

though, because history won't judge Greenspan's 18 years as Fed

chairman based on how things look on the day of his retirement. More to

the point, we doubt that Greenspan believes that his legacy will be

determined by how things look on his final day. Therefore, it's not

reasonable to expect the Fed to be any 'easier' over the coming two

quarters than would have been the case if Greenspan were not retiring

early next year. In fact, we think it's more reasonable to argue that

the Fed will be 'tighter' than would otherwise have been the case

because Greenspan will know that he won't be the one responsible for

cleaning up the mess resulting from the collapsing of multiple bubbles.

But it's most reasonable, we think, to expect the Fed to behave in a

way that is consistent with its traditional modus operandi; in

particular, to expect Greenspan and Co. to persist with their

rate-hiking until either a) the Fed Funds rate has reached what they

perceive to be 'neutrality', or b) the stock and/or commodity markets

cave in.

Our view, as you know, is that the stock and commodity markets will

cave in long before the Fed reaches what Greenspan and his cohorts

consider to be a neutral Fed Funds Rate.

Further to the above, the Fed isn't likely to do anything different

simply as a result of Greenspan being in his final months as Fed chief.

However, we expect that the transition to someone new will have an

adverse effect on financial market confidence and that this will cause

the Fed to be more accommodative during 2006-2007 than it might

otherwise have been. The reason is that additional uncertainty is

likely to be generated by having 'the devil you don't know' at the helm

of the Fed, especially if downward trends are already entrenched in the

stock and commodity markets.

The high probability of there being a new Fed Chairman early next year

actually meshes very well with our 1-2 year outlooks for various

markets, particularly our view that a new bull market in the gold

sector will get underway late this year.

Evidence of falling growth

An important component

of our intermediate-term outlook is that there will be a ramping down

of global growth expectations during the second half of this year and

much of next year. This lowering of growth expectations should

initially be evidenced by declining prices for cyclical commodities

such as the industrial metals and later -- most likely beginning in the

final quarter of this year -- by considerable strength in

counter-cyclical investments such as gold and gold shares.

As things stand today global stock markets are refusing to buckle and

are therefore not yet confirming the intermediate-term outlook

summarised above. However, significant support for our bearish outlook

on economic growth is coming from other markets and indicators. For

example, the chart at http://www.investmenttools.com/futures/bdi_baltic_dry_index.htm

shows that the Baltic Dry Index -- an index comprising the ocean-going

freight rates on 11 major shipping routes -- has now fallen by around

60% since last December's peak. This crash in freight rates is no doubt

partially due to an increase in the supply of ships, but it's unlikely

that such a precipitous fall could have occurred unless there had also

been a pronounced reduction in global trade.

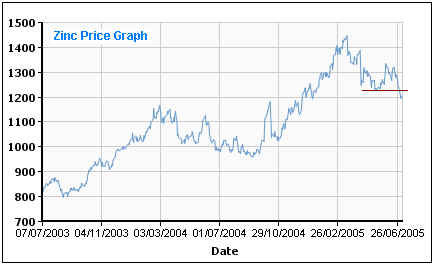

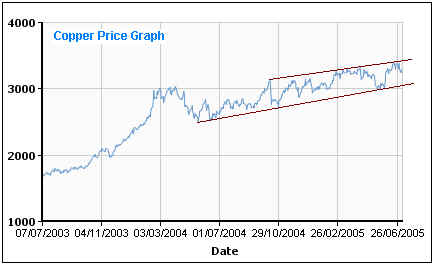

In general, industrial metal prices have also begun to support our

view. The below charts, for example, show that there have been

significant downward moves in the prices of aluminium, nickel, zinc and

lead. Copper is now the lone 'hold out', probably because it is a

speculative favourite of hedge funds. A daily close below

US$3,000/tonne in the 3-month buyer's price for copper on the LME

(London Metal Exchange) would be a clear sign that an intermediate-term

peak was in place in the copper market.

The last piece of

evidence we'll mention is the recent drop in the Australian Dollar

relative to the euro. A$/euro, a chart of which is included below,

tends to move with the US stock market and with global growth (the A$

is widely perceived to be a growth-oriented currency). It is generally

quite volatile so taken in isolation the plunge that has occurred over

the past fortnight is not necessarily significant, but taken alongside

the weakness in metal prices and the on-going decline in the Baltic Dry

Index it constitutes additional evidence that the downturn we've been

anticipating is underway.

The US

Stock Market

Current Market Situation

If

the market continues to decline over the next few weeks then a bullish

divergence will become possible, but only if the Dow drops below 10,000

while the NDX holds comfortably above 1400.

Over the past several years the divergences that have occurred between

the Dow Industrials Index and the NASDAQ100 Index (NDX), whereby a move

to new extreme for the year by the Dow was not confirmed by the NDX,

have turned out to be important. For example, the below chart shows

that there have been two such divergences over the past year -- a

bullish divergence in October-2004 (point A on the chart) when a move

to a new low by the Dow was accompanied by a substantially higher low

by the NDX, and a bearish divergence in March-2005 (point B on the

chart) when a move to a new high by the Dow was accompanied by a

substantially lower high by the NDX.

If the market continues to decline over the next few weeks then a

bullish divergence will become possible, but only if the Dow drops

below 10,000 while the NDX holds comfortably above 1400. The point is,

if such a divergence does occur it will be a good idea to exit, or at

least to reduce exposure to, bearish positions. In fact, if such a

divergence occurs we will seriously consider entering some trades on

the 'long' side. By the same token, there would be no reason to reduce

exposure to bearish positions if a drop below 10,000 by the Dow WAS

confirmed by the NDX dropping below 1400.

The market is yet to

tip its hand as far as what we can expect over the coming weeks in that

a rebound to test the June highs looks almost as likely as a drop to

test the April lows. A daily close below 10,250 in the Dow would,

however, shift the odds in favour of a drop to test the April lows.

By the way, there was an interesting divergence on Wednesday between

the oil price and the prices of oil-related equities. Specifically,

both the AMEX Oil Index (XOI) and the Oil Service Index (OSX) were weak

in absolute terms and relative to the S&P500 Index even though the

oil price surged $1.70 to a new all-time high. The major oil producers

are no doubt going to announce extremely strong earnings results later

this month, but it's quite likely that these results are already

factored into current stock prices and that the good earnings news will

be taken as an opportunity to sell. We don't want to read too much into

a single day's action, but perhaps yesterday's surprisingly weak

performance by the oil shares was due to some traders anticipating just

that (a sell-off later this month in the wake of good earnings news).

Gold and

the Dollar

Gold Stocks

The below chart shows that the AMEX Gold BUGS Index (HUI) has spent the

past 14 trading days oscillating within a 10-point range. We suspect

that an upside breakout from this range would quickly be followed by a

move up to 210, but not much more than that. And as noted in previous

commentaries, we would consider a close below 192 to be a clear signal

that the rebound was over and that the next downward leg had begun.

Gold stocks continue

to perform quite well relative to the gold price and we haven't yet

seen any solid evidence that a rebound peak is in place. About the only

short-term bearish sign that we're aware of is this week's drop below

support by Newmont Mining (see chart below). A pullback in NEM to test

June's upside breakout would have been par for the course, but the

stock has dropped a bit further than it ideally should have done. We

wouldn't, however, put a lot of weight on NEM's minor breakdown in the

absence of a close below 192 by the HUI; or a close below 90 by the

XAU; or significant weakness in gold stocks relative to the metal.

Current Market Situation

Last year's peak of around 92 has been, and continues to be, our target

for the FIRST upward leg in the Dollar Index's rally (see chart below).

We expect that this target will be reached within the next 6 weeks.

Support at just below 89.5 should hold during any near-term pullbacks.

Below is a daily chart of August gold futures.

Despite the fact that gold stocks still appear to have the potential to

move to new rebound highs over the coming days/weeks it looks like a

rebound peak is already in place for gold. If this proves to be the

case it will be a strange turn of events because the gold sector of the

stock market tends to reverse downward, or to at least show relative

weakness, PRIOR to significant peaks in the bullion market.

Critical support for August gold lies at $417, but given that the gold

price has just fallen by $20 in very quick time we'll be surprised if a

break below this support happens within the next 1-2 weeks. However, we

continue to expect that this support will be broken and that gold will

trade below $400 before it embarks on the next major advance in its

long-term bull market.

Update

on Stock Selections

The

managements of Aflease Gold and Uranium (JSE: AFL, OTC: AFLUY) and

Southern Cross Resources (TSX: SXR) are planning to merge the two

companies to create SXR Uranium One, a company that will be listed on

the Toronto Exchange under the symbol SXR. Although the merger will be

carried out by SXR issuing 0.9 of its shares for every Aflease share --

the equivalent of 9 SXR shares for every Aflease ADR -- it is

effectively a takeover by Aflease of the smaller SXR because Aflease

shareholders will end up owning 83% of the new company. If everything

goes according to plan the merger will be complete by October. The

managements of Aflease Gold and Uranium (JSE: AFL, OTC: AFLUY) and

Southern Cross Resources (TSX: SXR) are planning to merge the two

companies to create SXR Uranium One, a company that will be listed on

the Toronto Exchange under the symbol SXR. Although the merger will be

carried out by SXR issuing 0.9 of its shares for every Aflease share --

the equivalent of 9 SXR shares for every Aflease ADR -- it is

effectively a takeover by Aflease of the smaller SXR because Aflease

shareholders will end up owning 83% of the new company. If everything

goes according to plan the merger will be complete by October.

This merger provides a way for Aflease to obtain a listing on a major

North American market (it currently only trades on the horrid "Pink

Sheets" market in the US) and a way for Aflease to obtain easier access

to equity financing as it works towards bringing its huge South

African-based uranium project into production. As far as we can tell,

though, it's an expensive way to achieve these ends because the assets

that SXR brings to the table don't appear to be worth what Aflease is

paying for them. What SXR brings to the table are the fully permitted

Honeymoon project in South Australia with its 9.3M-pound uranium

resource and potential production of 880K pounds/year, the Goulds Dam

project in South Australia with its 12.3M-pound uranium resource (4.4M

pounds indicated plus 7.9M pounds inferred), and a few early-stage

exploration projects in Australia and Canada.

In a press release issued to announce the companies' plans it was

pointed out that the merger terms were based on current market prices,

but in our opinion current market prices were under-valuing Aflease and

over-valuing SXR.

Further to the above we think that having Aflease listed on the TSX is

a significant positive, but that the deal, as announced, is a better

one for SXR shareholders than for Aflease shareholders.

We still like Aflease as a long-term investment, but as a result of

this planned merger and a soon-to-occur US$20M financing we would not

be buyers at the current price. Instead, we'd prefer to wait for a

pullback to around US$6.00 before doing any new buying.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.futuresource.com/

www.lme.com

|