![]()

![]()

![]()

![]()

- Interim Update 6th December 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The yield curve and the

boom-bust cycle

The central bank is not the root

cause of the boom-bust cycle. The root cause is fractional reserve banking

(the ability of banks to create money and credit out of nothing). The

central bank's effect on the cycle is to extend the booms, make the busts

more severe and prevent the investment errors of the boom from being fully

corrected prior to the start of the next cycle. Consequently, there are

some important relationships between interest rates and the performance of

the economy that would hold with or without a central bank, provided that

the practice of fractional reserve banking was widespread. One of these

relationships is the link between a reversal in the yield curve from

flattening to steepening and the start of an economic

recession/depression.

Unfortunately, the data we have at our

disposal doesn't go back anywhere near as far as we'd like, where "as far

as we'd like" in this case means 150 years or more. For example, the data

we have for the 10year-2year spread, which is our favourite indicator of

the US yield curve, only goes back to the mid-1970s.

For a

longer-term look at the performance of the US yield curve the best we can

do on short notice is use the Fed's data for the 10year-3month spread,

which goes back to the early-1960s. However, going back to the early-1960s

is good enough for government work and is still satisfactory for the

private sector.

As explained in many previous commentaries, the

boom phase of the cycle is characterised by borrowing short-term to

lend/invest long-term in order to take advantage of the artificial

abundance of cheap financing enabled by the creation of money and credit

out of nothing. This puts upward pressure on short-term interest rates

relative to long-term interest rates, meaning that it causes the yield

curve to flatten.

At some point, usually after the boom has been in

progress for several years, it becomes apparent that some of the

investments that were incentivised by the money/credit inflation were

ill-conceived. Losses start being realised, the quantity of loan defaults

begins to rise, and the opportunities to profit from short-term leverage

become scarcer. At this point everything still seems fine to casual

observers, central bankers, the average economist and the vast majority of

commentators on the financial markets, but the telltale sign that the

cycle has begun the transition from boom to bust is a trend reversal in

the yield curve. Short-term interest rates begin to fall relative to

long-term interest rates, that is, the yield curve begins to steepen.

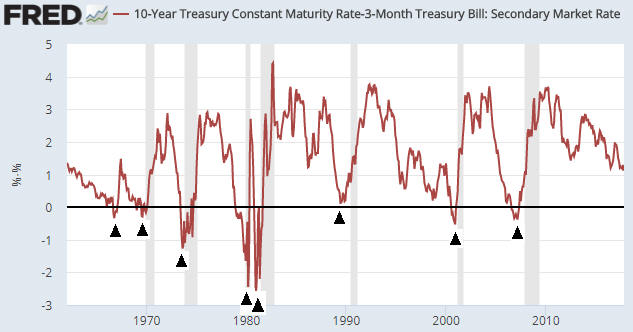

The following monthly chart of the 10year-3month spread illustrates

the process described above. On this chart, the boom periods roughly

coincide with the major downward trends (the yield-curve 'flattenings')

and the bust periods roughly coincide with the major upward trends (the

yield-curve 'steepenings'). The shaded areas are the periods when the US

economy was officially in recession.

The black arrows on the chart

mark the major trend reversals from flattening to steepening. With two

exceptions, such a reversal occurred shortly before the start of every

recession.

The first exception occurred in the mid-1960s, when a

reversal in the yield spread from a depressed level was not followed by a

recession. It seems that something happened at that time to suddenly and

temporarily elevate the 10year yield relative to the 3month yield.

The second exception was associated with the first part of the famous

double-dip recession of 1980-1982. Thanks to the extreme interest-rate

volatility of the period, the yield spread reversed from down to up

shortly before the start of the recession in 1980, which is typical, but

during the first month of the recession it plunged to a new low before

making a sustained reversal.

Due to the downward pressure being maintained on short-term interest

rates by the Fed, the yield curve reversal from flattening to steepening

that signals an imminent end to the current boom probably will happen with

the above-charted yield spread at an unusually high level. We can't know

at what level or exactly when it will happen, but it hasn't happened yet.

Copper tanks

There was a false upside

breakout in the copper price in mid-October. We mentioned in the 30th

October Weekly Update that something similar happened early in the year

when the copper price broke above its November-2016 high and then almost

immediately resumed a downward correction. Our view was that the

corrective process probably wouldn't end until the price had dropped to

near its 200-day MA.

The copper price plunged on Tuesday of this

week, but it is still about $0.15 above its 200-day MA. Also, the 200-day

MA now coincides with lateral support in the low-$2.80s, which makes the

low-$2.80s a reasonable target for a correction low.

Tuesday's price plunge was blamed on reduced Chinese demand for

copper, but it was more likely related to the liquidation of speculative

long positions. Speculative buying pushed up the prices of both copper and

nickel to levels that weren't supported by underlying demand for the

physical metals, so there is no reason to point to economic developments

in China to explain the recent price declines.

Also, the commodity

world is immersed in a broad consolidation that may extend into

January-February. This should be taken into account before looking for

news to explain the price weakness in any single commodity.

The Stock Market

The temporary suspension of the

US debt ceiling that was agreed in September ends on Friday 7th December,

meaning that the US federal government won't be able to add to its total

quantity of borrowings from 8th December until a new agreement (another

temporary suspension or the lifting of the ceiling) is reached.

The

stock market doesn't appear to be concerned about the risk of a US

government shutdown, and there's no reason it should be. The debt ceiling

will be lifted eventually and in the meantime the Treasury has the ability

to keep the wheels of government turning for at least two months by

drawing down its cash reserve ($178B at last count) and using some

accounting tricks.

In any case, with the US stock market stretched

to the upside by every measure and with the true fundamentals having

deteriorated over the past month it won't take a specific event to bring

on a multi-month correction. It will happen of its own accord.

The

increasing 2-way volatility of the past several days could be a warning

that the trend is in the process of changing, but with the upward trend

having extended so far into the year it would be no surprise if it

continued until year-end. In this case there would be a good chance of a

correction beginning in early-2018.

Gold and the Dollar

Gold

Revisiting the 15-year cycle

In

last week's Interim Update, we wrote:

"If the pattern (major

low followed by relatively minor low followed by major low and so on)

continues then 2015 was akin to 1985 and the next major [gold] rally will

begin around 2030."

And:

"The 15-year cycle low of

1985 was followed by a rally that lasted 2 years and nine months. If we

are now dealing with something similar then the rally that began in

December-2015 will end during the second half of next year."

Bearing in mind that a lot more emphasis should be placed on real-time

analysis of fundamentals, sentiment and technicals than on historical

comparisons, we thought it would be interesting to consider this 'what if'

scenario: What if the gold rally from the December-2015 low is evolving in

a roughly similar manner to the gold rally that began in March-1985?

The twists and turns of the 1985-1987 rally and the post-December-2015

rally don't have much in common, but in broad-brush terms the current

situation is potentially equivalent to either Q2-1986 or Q1-1987.

The argument in favour of Q2-1986 revolves around the position of the

price relative to the long-term downward-sloping trend-line. Specifically,

in Q2-1986 the gold market was immersed in its first significant

correction following a break above the trend-line dating back to the 1980

high, and it could be argued that the gold market is presently immersed in

its first significant correction following a break above the trend-line

dating back to the 2011 high. Refer to the following charts for more

detail.

The argument in favour of Q1-1987 is stronger. It revolves

around the amount of time that has lapsed since the 15-year cycle low and

the performances of inter-related markets. Specifically, Q1-1987 was 2

years after the 15-year cycle low, which is where we are today, and also

when a multi-quarter surge in interest rates got underway, which could be

where we are today.

Our gold market analysis won't be based in any way on the 1985-1987

comparison unless the gold price moves above its 2017 high within the

coming few months, at which point the comparison could be very relevant.

Current Market Situation

We've

been warning that before the next substantial gold rally gets underway

there may have to be a sharp decline -- likely to the low-$1200s -- to

flush out the leveraged speculators who have stubbornly clung to their

long positions. It looks like the flushing-out process has begun, although

the gold price continues to hold above support in the low-$1260s. This is

probably because the fundamental backdrop remains slightly supportive.

We'll take the evidence as it comes, but our guess at this time is

that the next multi-month bottom for the gold price will happen during

January or February of next year. However, if there's a sharp decline

ahead of or in the immediate aftermath of the Fed's 13th December

rate-hike announcement (a December rate hike has been a foregone

conclusion for at least the past 2 months) then a multi-month price bottom

could occur as soon as next week.

Silver

Gold is not yet 'oversold' in momentum terms, but that's not the case with

silver. The silver price is now sufficiently 'oversold' to suggest that

some sort of bottom is close at hand, at least in terms of time. That

being said, during the April-May sell-off the silver market became far

more 'oversold' than it is today.

Right now silver is on a 7-day

losing streak and has a daily RSI(14) of 30.8, whereas at the multi-week

price bottom in early-May it had just fallen for 11 trading days in a row

and had a daily RSI of only 17.4. Significant additional near-term

weakness is therefore well within the realm of possibility.

We'll be paying close attention to silver's COT data over the weeks

ahead in an effort to identify a tradable low. A 2-3 week price rebound

could occur without a bullish signal from the COT data, but to set the

stage for a multi-month rally there probably will have to be a complete

sentiment reset.

Gold Stocks

From the

latest Weekly Update:

"We don't see a good reason to believe

that a general increase in demand for gold-mining stocks is about to

happen. Instead, a general increase in demand probably requires a

preceding capitulation -- the capitulation of bullish speculators in gold

futures and the capitulation of gold-mining investors who are holding in

expectation of the big rally that is supposed to begin in December."

A capitulation has begun. Looking at the glass as being half full,

although this results in short-term pain it is good news because it gets

us closer to the point where the stage is set for a tradable rally.

In last week's Interim Update and again in the latest Weekly Update we

noted that a break below the bottom of the HUI's recent 5-point range

(185) probably would lead to a quick decline to near the July low (177)

and could also pave the way for a test, within the ensuing 1-2 months, of

the December-2016 low (160).

The bottom of the 5-point range was

breached on Monday of this week and the July low is already being tested.

In fact, on Wednesday 6th December the HUI fell below its July low to a

new low for the year.

There appears to be channel support at around

172 (see chart below), but the next clear-cut support is the December-2016

low at 160. We think that this support defines the short-term downside

risk.

The waters are muddied a little by a conflict between the chart

patterns of the HUI and the Gold Miners ETF (GDX). Whereas the HUI made a

new low for the year on Wednesday, GDX is still comfortably above support

defined by its May and July lows. Also, at this time it doesn't look like

GDX has a realistic chance of falling as far as its December-2016 low

($18.50) prior to a multi-month bottom.

Although it's hard to believe that the gold-mining indices and ETFs

will bottom prior to the bullion market making a sustainable low, the way

things currently stand a December low is a more likely prospect for the

gold-mining sector than for gold bullion.

The Currency

Market

The following chart compares the euro (the blue

line) with the interest-rate differential that exerts the greatest

influence on the euro/US$ exchange rate. The message is that the euro is

presently a lot higher than it should be given the current difference

between Germany and US 10-year bond yields.

We expect the euro to

trade significantly lower within the next two months.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://research.stlouisfed.org/

![]()