![]()

![]()

![]()

![]()

- Interim Update 7th June 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Gold True Fundamentals

Model

To paraphrase Jim Grant, gold's

perceived value in US$ terms is the reciprocal of confidence in the Fed

and/or the US economy. Consequently, what we refer to as gold's true

fundamentals are measures of confidence in the Fed and/or the US economy.

We've been covering these fundamental drivers of the gold price in TSI

commentaries for almost 17 years. It doesn't seem that long, but time

flies when you're having fun.

Note that we use the word "true" to

distinguish the actual fundamental drivers of the gold price from the

drivers that are regularly cited by gold-market analysts and commentators.

According to many pontificators on the gold market, gold's fundamentals

include the volume of metal flowing into the inventories of gold ETFs,

China's gold imports, the volume of gold being transferred out of the

Shanghai Futures Exchange inventory, the amount of "registered" gold at

the COMEX, India's monsoon and wedding seasons, jewellery demand, the

amount of gold being bought/sold by various central banks, changes in mine

production and scrap supply, and wild guesses regarding JP Morgan's

exposure to gold. These aren't true fundamental price drivers. At best,

they are distractions.

In no particular order, the gold market's

six most important fundamental price drivers are the trends in 1) the real

interest rate (as indicated by the yield on the 10-year TIPS), 2) the

yield curve (as indicated by the 10yr-2yr yield spread), 3) credit spreads

(as indicated by the ratio of a Treasury Note ETF to a junk bond ETF or

the spread between a high-yield index and the 10-year T-Note yield), 4)

the relative strength of the banking sector (as indicated by the BKX/SPX

ratio), 5) the US dollar's exchange rate (as indicated by the Dollar

Index) and 6) commodity prices in general (as indicated by GNX). Even

though it creates some duplication, we should also include the bond/dollar

ratio (as indicated by ratio of the 30-year T-Bond price to the Dollar

Index).

Up until now we have taken the above-mentioned price

drivers into account to arrive at a qualitative assessment of whether the

fundamental backdrop is bullish, bearish or neutral for gold, but we are

now making a significant change to our approach. To remove all

subjectivity and also to enable changes in the overall fundamental

backdrop to be charted over time, we have developed a model that combines

the above-mentioned seven influences to arrive at a number that indicates

the extent to which the fundamental backdrop is gold-bullish.

Specifically, for each of the seven fundamental drivers/influences we

determined the weekly moving average (MA) for which a MA crossover catches

the most trend changes in timely fashion with the least number of

'whipsaws'. It's a trade-off, because the shorter the MA the sooner it

will be crossed following a genuine trend change but the more false

trend-change signals it will cause to be generated. We then assign a value

of 100 or 0 to the driver depending on whether its position relative to

the MA is gold-bullish or gold-bearish. For example, if the yield-curve

indicator is ABOVE its pre-determined weekly MA then it will be assigned a

value of 100 by our model, because being above the MA points to a

steepening yield-curve trend (bullish for gold). Otherwise, it will be

zero. For another example, if our real interest rate indicator is BELOW

its pre-determined weekly MA then it will be assigned a value of 100 by

our model, because being below the MA points to a falling

real-interest-rate trend (bullish for gold). Otherwise, it will be zero.

The seven numbers, each of which is either 0 or 100, are then averaged

to arrive at a single number that indicates the extent to which the

fundamental backdrop is gold-bullish, with 100 indicating maximum

bullishness and 0 indicating minimum bullishness (maximum bearishness).

The neutral level is 50, but the model's output will always be either

above 50 (bullish) or below 50 (bearish). That's simply a function of

having an odd number of inputs.

Before we get to charts showing the

historical performance of the Gold True Fundamentals Model (GTFM), we

point out that:

1) The fundamental situation should be viewed as

pressure, with a bullish situation putting upward pressure on the price

and a bearish situation putting downward pressure on the price. It is

certainly possible for the price to move counter to the fundamental

pressure for a while, although it's extremely likely that a large price

advance will coincide with the GTFM being in bullish territory most of the

time and a large price decline will coincide with the GTFM being in

bearish territory most of the time.

2) The effectiveness of

fundamental pressure will be strongly influenced by sentiment (as

primarily indicated by the COT data) and relative valuation (as primarily

indicated by the gold/commodity ratio). In particular, if the fundamental

backdrop is bullish and at the same time the gold/commodity ratio is high

and the COT data indicate that speculators are aggressively betting on a

higher gold price then it is likely that the bullish fundamental backdrop

has been factored into the current price and that the remaining upside

potential is minimal. By the same token, if the fundamental backdrop is

bearish concurrently with the gold/commodity ratio being low and the COT

data indicating that speculators are pessimistic about gold's prospects

then it is likely that the bearish fundamental backdrop has been factored

into the current price and that the remaining downside potential is

minimal. The best buying opportunities therefore occur when a bullish

fundamental backdrop coincides with pessimistic sentiment and a low

gold/commodity ratio.

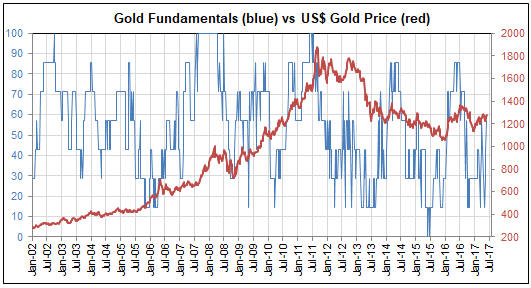

Getting down to brass tacks, here is a weekly

chart comparing the GTFM with the US$ gold price since the beginning of

2002. Unfortunately, we couldn't calculate the GTFM further back than 2002

because we don't have earlier data for some of the model's inputs.

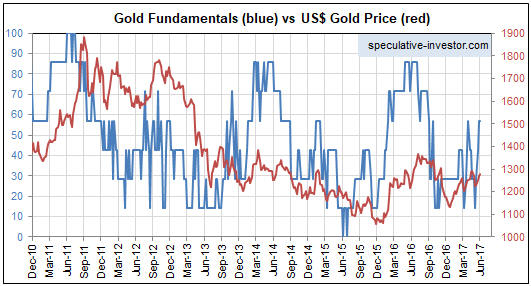

The above chart is too cluttered to see what's going on, so here's a

chart that zooms in on the period from December-2010 to last week.

It is apparent from the second of the above charts that there is a

positive correlation between the GTFM and the price, which, of course,

should be the case if the GTFM is a valid model. If you look closely it

should also be apparent that the fundamentals (as represented by the GTFM)

tend to lead the gold price at important turning points. For example, the

GTFM turned down in advance of the gold price during 2011-2012 and turned

up in advance of the gold price in 2015 (the GTFM bottomed in mid-2015

whereas the gold price didn't bottom until December-2015).

The

tendency for gold to react to, rather than anticipate, changes in the

fundamentals is not a new development, as evidenced by gold's delayed

reaction to a major fundamental change in the late-1970s. We are referring

to the fact that by the second half of 1978 the monetary environment had

already turned decisively gold-bearish, but the gold price subsequently

experienced a massive rally that didn't culminate until January-1980.

Finally, we will calculate the GTFM at the end of each week. It was in

bullish territory at the end of the past two weeks and will be in bullish

territory at the end of this week unless something dramatic happens over

the next two trading days.

The Stock Market

The US

The US stock market was as quiet as a market can get over the first three

days of this week. None of the indices we usually discuss did anything

worth commenting on, but this is an opportune time to take another look at

the steel sector. It's opportune because the VanEck Steel ETF (SLX) has

drifted downward near its channel top over the past three weeks and will

soon have to either signal an upward reversal by breaking above resistance

or signal the start of an accelerated decline by breaking below support.

The channel top is at $36.50-$37.00 and trend-defining lateral

resistance is at $38.00, so a daily close above $37.00 would warn that an

upward reversal was in the works and a weekly close above $38.00 would

confirm that the short-term trend had reversed.

Support lies at

$35.00-$35.50. A daily close below $35.00 would suggest that the

post-election rally was going to be fully retraced via a decline to $32 or

lower.

The only other point worth mentioning is that there have been two "Hindenburg

Omen" signals over the past 5 weeks, with the most recent occurring

last week. A Hindenburg Omen is a warning that a large stock market

decline will commence within the coming month and in the past it has never

failed to provide timely warning of a large stock market decline. The

problem is that most of the signals turn out to be false. In other words,

the Hindenburg Omen has generated no false negatives and many false

positives.

The Hindenburg Omen shouldn't be used in isolation, but

the recent occurrence of this signal adds to the evidence that the current

environment is high-risk.

Europe

The EURO

STOXX 50 Index (STOX5E), the European equivalent of the Dow Industrials

Index, peaked in early-May and has since pulled back to its 50-day MA. If

this is a routine correction to a short-term upward trend then the decline

should end near its current level, whereas a daily close below 3500 would

warn that the short-term upward trend was over.

Gold and the Dollar

Gold

Unsurprisingly, the US$ gold price moved up to test its April high of

around $1300 during the first half of this week. It's likely to spike

above $1300 before making a multi-week top, but the big question is: Will

there be a sustainable break above $1300 in the near future?

With the current fundamental backdrop skewed bullishly for gold a

sustainable breakout is a realistic possibility, although we remain

sceptical. The main reason is the multi-month bearish divergence between

the gold-mining sector and the bullion market, which didn't disappear as a

result of Tuesday's impressive strength in the gold-mining sector. Another

reason is that sentiment and relative valuation indicate that the

gold-bullish fundamental backdrop could already be factored into the

price.

That being said, it is now looking less likely that we will

get an important low during the June-July period. In fact, if gold is able

to end this week above $1300 then we could be looking at a June-July high

(similar to last year), which would be a good match for what we expect in

the T-Bond market and would also be consistent with a significant decline

in the US stock market within the next several weeks.

We'll have

more to say on this topic in the Weekly Update.

Gold Stocks

Current Market Situation

The

gold-mining indices and ETFs are all in slightly different positions on

the charts. Specifically:

1) The HUI began Tuesday below its

20-day, 50-day and 200-day MAs, but ended the day above all of these MAs.

It then dropped a little and ended Wednesday's session almost exactly at

its 200-day MA. Also, it remains comfortably below the downward-sloping

trend-line drawn from the February peak.

2) In addition to breaking above its 20-day, 50-day and 200-day MAs,

the XAU has broken above the downward-sloping trend-line drawn from the

February peak.

3) The chart position of the VanEck Gold Miners ETF (GDX) is slightly

stronger than that of the HUI and slightly weaker than that of the XAU. It

is above its 200-day MA and tested its downward-sloping trend-line during

the first half of the week.

4) The Global X Gold Explorers ETF (GOEX) has been hurt by the

infamous GDXJ re-balance that is due to be complete at the end of next

week. It broke decisively below its March low in early-May and has not yet

rebounded to its 200-day MA.

One thing these indices and ETFs have in common is that Tuesday's

surge possibly constituted a significant change. We'll discuss the

implications in the Weekly Update.

Note that if a short-term trend

reversal (to the upside) has occurred then at least one of the final two

trading days of this week should be up-days.

Gold stocks for a multi-month trade, update 1

In the 24th May Interim Update we mentioned 5 gold-mining stocks that

were potential additions to the TSI Stocks List as short-term trading

positions. The stocks were AKG, CNL.TO, PG.TO, RMS.AX and SAND.

Due

to company-specific developments, AKG has almost ruled itself out as a

potential trading position. We say "almost", because the information

provided by management early this week regarding the Expansion Feasibility

Study suggests that the short sellers are wrong about the company needing

to tap the capital markets within the next 12 months to sustain its

production. Unless AKG's senior management is outright lying and thus

leaving itself open to legal problems that are far more serious than the

time-wasting class-action lawsuits initiated recently by a gaggle of

ambulance-chasing lawyers, the company will remain in good financial shape

over the next year or two regardless of whether it gets additional

financing.

Based on the information we have today, AKG would be a

reasonable speculation if it were to drop back to near last week's low

(US$1.25-$1.30). It is probably worth substantially more than $1.30 in the

current gold-market environment and probably won't drop that far, but

given the risks and unknowns we'd require that price or lower to make the

risk/reward sufficiently attractive.

The other stocks have rallied

with the gold-mining sector and are now a long way above the prices at

which we had hoped to add them to the TSI List. Does this mean that we

should pay up?

How anyone responds to a changing market will always

be at least partly determined by their existing positioning. For example,

we have plenty of exposure to gold-mining stocks in the TSI List and in

our own account, so we are not inclined to pay significantly more than the

prices previously mentioned. However, we would be less stingy with regard

to new buying if our existing exposure to the gold-mining sector was

substantially less.

Keeping in mind that a major rally is probably

NOT about to begin, if you currently feel under-exposed to gold-mining

stocks you could buy the Global X Gold Explorers ETF (GOEX) for a trade in

the US$22-$23 range and set an initial stop slightly below the early-June

low (near $21). Alternatively, you could choose to take greater risk in an

effort to get much higher returns by taking positions in some junior gold

and/or silver miners that are 'oversold' and trading at relatively low

valuations.

BLK.AX and GRG.V are two examples from the TSI Stocks

List. US Gold Corp. (NASDAQ: DRAM), a stock that was briefly written-up

and added to the TSI Small Stocks Watch List in the 22nd May Weekly

Update, is also worth considering near its current ultra-depressed level

in the US$2.60s, although not as a short-term trade. DRAM's long-term

reward/risk is very attractive near its current price, but even though its

liquidity has recently improved it is still too illiquid to be a

short-term trading vehicle.

The Currency Market

It has been a very uneventful week to date in the currency market.

However, there are three events scheduled for Thursday 8th June with the

potential to generate some volatility.

The first event is the UK

election. Despite the closeness indicated by some opinion polls over the

past two weeks, the currency market and the other financial markets have

been assuming that common-sense would prevail and that Theresa May's party

would be successful in the end. Putting it another way, if the markets had

assigned a significant probability to a victory by the Corbyn-led Labour

Party then the Pound and the FTSE100 would have tanked. The financial

markets got the "Brexit" outcome completely wrong, but being completely

wrong about the election outcome would be a much bigger surprise.

The second event is the ECB Meeting. This meeting could be more important

than the average ECB get-together because it could result in the first

small step away from ultra-loose monetary policy. The currency market has

been expecting a small step in that direction, which is partly why the

euro has rallied.

The third event is the testimony to be given by

former FBI chief James Comey about the Russian government's supposed

intervention in the US election. This is a chapter in a non-story that has

been blown up by the media and Trump's political enemies into a huge story.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

![]()