![]()

![]()

![]()

![]()

- Interim Update 7th August 2019

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Currency Manipulation

In the email sent to subscribers

after the close of US trading on Monday 5th August we wrote that the

catalyst for Monday's stock market sell-off was news that the Chinese

government's retaliation to last Thursday's US government tariff decision

would include Yuan devaluation. We also pointed out that in this case it

isn't accurate to use the word "devaluation", because that implies

manipulation to weaken the Yuan relative to the US$ when in reality

China's government had -- temporarily at least -- stopped trying to

prop-up the Yuan. That is, what we were witnessing was the ceasing of

actions designed to keep the Yuan artificially strong. Finally, we noted

the irony that the removal of this manipulative force could prompt the US

Treasury to cite China as a currency manipulator.

As if on cue, a

short time later the US Treasury labeled China a "currency manipulator".

The implied message to China's government is: if you STOP manipulating

your currency in the direction we want then we will call you a currency

manipulator. Government logic at its best.

Monday's managed

weakness in the Yuan was largely symbolic, for two reasons. First, more

than 50% of the cost of the average exported item from China is accounted

for by imported goods and materials, so to use the currency to fully

offset the effect of a 10% US tariff the Yuan would have to fall by more

than 20% against the US$. The trade-related effect of Monday's 1.5% Yuan

decline is therefore negligible. Second, China's government would be well

aware that a significant decline in Yuan/USD over a short period could

precipitate the sort of financial-market upheaval that would have negative

ramifications for China's economy.

The Yuan is very over-valued and

will get a lot weaker at some point, but substantial weakness is unlikely

in the short-term for the reason mentioned directly above, that is,

because the resulting disturbance to the financial markets would be as

much of a problem for China as it would be for any other country. What

appears to have occurred early this week is a warning shot from China's

government. The warning to the US government is: if you continue to use

protectionist measures as a negotiation tactic then we will stop

propping-up the Yuan.

The Stock Market

The disconnect between

the stock market and corporate profits

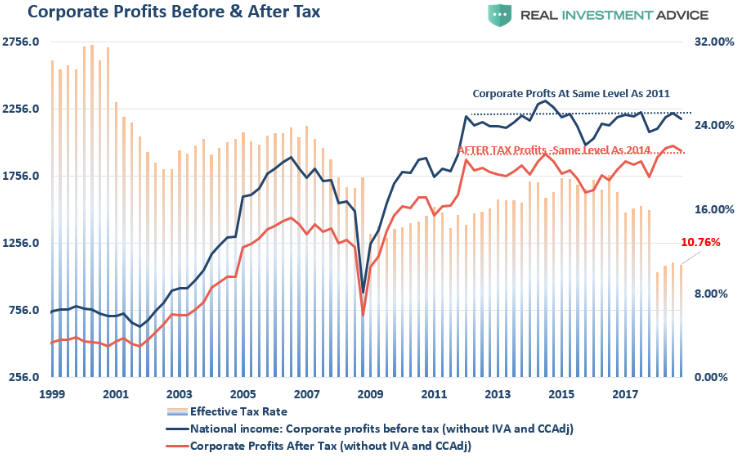

In light of the US

stock market's strong long-term upward trend, the following chart is

extraordinary. The chart shows that US pre-tax corporate profits are no

higher today, and that US post-tax corporate profits are only slightly

higher today, than they were in 2011. The implication is that the bullish

stock market trend of the past 8 years went hand-in-hand with no growth in

total corporate profitability. Given that the stock market didn't look

cheap in 2011, how could this be?

One part of the two-part answer

is that the stock market's average P/E ratio has trended upward, meaning

that 'investors' have been willing to pay increasingly-larger amounts for

the same earnings. The second and less obvious part of the answer is that

although total US corporate profits have gone sideways over the past 8

years, thanks to share buybacks there has been decent growth in the profit

per share. This is especially the case for the large-cap companies that

make up the S&P500 and NASDAQ100 indices. In 2018 alone, listed US

corporations bought back about 1 trillion dollars of their own shares.

This means that the greatest monetary stimulus in history didn't work

as intended. It was supposed to boost the sort of corporate investment

that leads to a general increase in prosperity, but instead its most

obvious effect was to boost the popularity of financial engineering. Due

to a deluge of cheap credit it has made sense for many (not all) corporate

managements to borrow money to buy back their company's own shares at

ever-higher prices, thus achieving significant earnings-per-share growth

while taking almost no risk, rather than go down the harder and riskier

path of growing the actual business.

The economic theories that

were put into practice over the past 10 years did not work as advertised.

Unfortunately, these theories are still guiding the actions of

policy-makers in all major central banks and governments.

Current Market Situation

It should go without saying that

the sort of sudden weakness in the stock market that occurred on Monday of

this week is an opportunity for the holders of bearish option positions,

such as SPY put options, to take profits. If you are an options trader and

you find yourself with a large profit thanks to dramatic market action,

then taking some money off the table should be an automatic response.

Don't wait for us or any other analyst/advisor to make the profit-taking

suggestion. In this particular case we did make a profit-taking suggestion

via email, but by then the optimum time to exit had past.

We

emailed subscribers after the close of trading on Monday to highlight the

opportunity that had been created by the day's dramatic market action.

Here's how we summed up the situation:

"For those holding

short-dated bearish speculations the most reasonable tactic would be to

take profits on half of the position now with the aim of a) exiting the

balance when the stock indices drop to lower levels late this month or

early next month, and b) using part of the aforementioned profit to add a

new short-dated bearish speculation following a significant multi-day

market rebound. That's what we plan to do in our own account, except that

we almost certainly will make a complete exit from our bearish position if

the SPX plunges to the mid-2700s within the next two days (the index ended

Monday's session at 2845). For TSI record purposes, however, we will

assume that the total position is exited now and will look for an

opportunity to add a new position within the next two weeks."

If you were holding bearish option speculations and weren't quick enough

to take advantage of the circumstances that arose early this week, it

might not matter because there probably will be an even better

profit-taking opportunity before the end of this month. Also, if the SPX

rebounds to near its 50-day MA within the next few days it should be

viewed by short-term traders as a good chance to establish a new bearish

speculation in anticipation of a near-term drop to well below Monday's

low.

As illustrated by the following chart, the SPX's 50-day MA is

at 2931 and is rising.

The Dow Transportation Average (TRAN), which yet again has led to the

downside, broke below channel support last week and has since fallen by

enough to test important lateral support at 10,000.

For the SPX, the short-term downside target we have in mind is the

early-June low (around 2730). Given the bearish fundamental backdrop it

ultimately could drop a lot further than that, but it should at least test

its June low before the next multi-month bottom is in place.

For

the TRAN we are expecting a decline to well below the early-June low prior

to the next multi-month bottom.

Gold and the Dollar

Gold

In

the latest Weekly Update we noted that gold's price action since 25th June

looked like a consolidation with a slight upward bias. That is, although

the price hadn't fallen it was fair to say that in US$ terms gold had been

in correction mode for about 6 weeks (with numerous successful tests of

the 20-day MA along the way).

At the end of last week there was no

evidence that the correction was over, leaving open the possibility of a

decline to as low as $1350 prior to the upward trend resuming. However,

the US$ gold price clearly broke out to the upside on Monday in reaction

to the Chinese government's retaliation to last week's US government

decision to impose additional taxes on China-sourced imports. The gold

market built on Monday's upside breakout over the ensuing two days.

The top of the 6-week consolidation (around $1450) is now important

support. Closing below this support would signal a short-term trend

reversal.

Due to this week's surge the gold market has achieved the upside

target we had in mind for this year (the low-$1500s). The fundamental

backdrop remains supportive and there is no evidence that the rally is

over, but the short-term downside risk is now high due to the market being

extremely stretched in both momentum and sentiment terms. It won't

surprise us if the surge continues for another 1-4 weeks, but almost

regardless of what happens over the next month there's a good chance that

the price will trade comfortably below its current level within the next

three months. Therefore, this is a time to be scaling out of gold

exposure, not adding to it.

Although there is no evidence that gold

has reached a short-term price top, one warning sign of an impending

short-term top emerged over the past few days. We are referring to the

fact that the HUI/gold ratio has not confirmed this week's upside breakout

in the gold price. As illustrated by the following chart, the ratio

remains below its mid-July high.

For the HUI/gold ratio to generate

a clear-cut bearish signal it would have to close below its 40-day MA,

which it has not done. However, any sort of divergence between the bullion

price and the gold-mining sector can be meaningful when the bullion price

is stretched to either the upside or the downside.

Silver

The US$ silver price also broke out to

the upside and thus completed its short-term correction over the first

three trading days of this week. The September silver futures contract

ended Wednesday's session at US$17.20 and only needs to finish this week

above US$16.48 to solidify its longer-term upside breakout.

Like the gold market the silver market is now stretched to the upside

in both momentum and sentiment terms, although at current prices silver is

a better candidate for new buying than gold. There remains the potential

for silver to make a big catch-up move within the next few months.

A warning that a short-term (1-3 month) top is in place would be generated

by a daily close below the 20-day MA. The 20-day MA is at $16.20 and is

rising rapidly.

By the way, at current metal prices ($1520 for

gold, $17.20 for silver and $870 for platinum) platinum is a much better

buy than either gold or silver. The platinum market is not 'stretched' to

the upside by any measure and platinum remains extremely cheap relative to

gold. As previously advised, platinum must achieve a weekly close above

US$920 to decisively break out to the upside and project a rise to at

least $1200.

Gold Stocks

The sharp rise in

the gold price to above $1500/oz on Wednesday 7th August didn't generate

much excitement in the gold-mining sector. A big part of the reason is

probably the HUI's proximity to obvious, major resistance at 220. As

illustrated by the following chart, the resistance is defined by the 2017

double top.

The HUI traded as high as 228 at one point on Wednesday before pulling

back to end the day almost exactly at 220, with a net gain on the day of

only 0.7%. This suggests to us that large, technically-oriented traders

began selling the HUI's component stocks (all of the senior and most of

the mid-tier gold producers) after 220 was reached.

Resistance for

the HUI at 220 is equivalent to resistance for GDX at $25. GDX blew

through its resistance more than a month ago and we expect that the HUI

will do the same, but not necessarily right away.

Another daily HUI

chart is displayed below. This one zooms in on the more recent price

action.

We noted in real time that both the 'oversold' extreme (in

momentum terms -- as indicated by the daily RSI) reached in August of last

year and the 'overbought' extreme reached in June of this year had bullish

implications regarding the likely performance over the coming few months.

At the moment there is a momentum divergence (a divergence between the

daily RSI and the price) involving higher highs for the price and lower

highs for momentum. This could have short-term bearish implications.

We are anticipating a sizable 1-2 month correction in the gold-mining

sector that could begin immediately but might not begin for another 2-4

weeks. We expect that this correction will be followed by a rally to new

multi-year highs.

If you have substantial exposure to the

gold-mining sector we suggest that you start taking some money off the

table. During the first half of this week we took partial profits on two

gold-stock positions and have above-the-market sell orders in place with

the aim of taking partial profits on a few other gold-stock positions.

The Currency Market

After last week's Fed

meeting the Fed Funds Futures (FFF) market was 'saying' that there

probably would be just one more rate cut before year-end. The FFF market

is now saying there is a 100% chance of two more rate cuts and about a 50%

chance of a third additional rate cut before year-end. In other words,

expectations regarding what the Fed will do are changing rapidly.

These changes are affecting the Dollar Index (DX). After poking its head

above resistance at 98.1 last Wednesday-Thursday during the hours after

the Fed's announcement the DX has since dropped back to support at around

97.2.

We guess that the 'choppy' price action will continue for at

least a few more weeks.

Almost everyone's focus this week has been on the Yuan. As illustrated

by the following weekly chart, the USD/Yuan exchange rate has broken out

to the upside. Note that a rising line on this chart indicates a weakening

Yuan. The move is too small to affect the prices paid/received in US-China

trade, but the break above an obvious demarcation level had an outsized

effect on sentiment.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

http://bigcharts.marketwatch.com/

![]()