![]()

![]()

![]()

![]()

- Interim Update 8th March 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Revisiting the

limitations of sentiment

It was only three months ago*

that we last discussed the limitations of sentiment as a market timing

indicator, but we are revisiting the topic today to mention an additional

pitfall and a more topical example.

It's important to state up

front that despite the associated pitfalls, it can definitely be helpful

to track the public's sentiment and use it as a contrary indicator. This

is because most participants in the financial markets get swept up by the

general mood. They end up buying into the idea that prices are bound to go

much higher despite valuations having already become unusually high or the

idea that prices will continue to slide despite current valuations being

unusually low. This causes them to be very optimistic near important price

tops and either very pessimistic or totally disinterested near important

price bottoms.

It will always be this way because 1) a major

price/valuation trend can't end until the fundamental story behind the

trend has been fully embraced by 'the public', and 2) the public's own

buying/selling shifts the probability of success. For example, when the

public gets enthusiastic about an investment its own buying pushes up the

price of the investment to the point where future performance is

guaranteed to be poor. Consequently, there is no chance that the investing

public can ever collectively enter or exit any market at an opportune

time.

There are, however, three potential pitfalls associated with

using sentiment to guide buying/selling decisions.

The first is

linked to the reality that sentiment generally follows price, which makes

it a near certainty that the overall mood will be at an optimistic extreme

when the price is near an important top and a pessimistic extreme when the

price is near an important bottom. The problem is that while an important

price extreme will always be associated with a sentiment extreme (extreme

optimism at a price high and extreme pessimism at a price low), a

sentiment extreme doesn't necessarily imply an important price extreme.

For example, if the price of an investment has been trending strongly

upward for many months and is at an all-time high then sentiment

indicators will almost certainly reveal great optimism even if the upward

trend still has a long way to go. It is therefore dangerous to take large

positions based solely on sentiment.

The second potential pitfall

associated with using sentiment to guide buying/selling decisions is that

what constitutes a sentiment extreme will vary over time, meaning that

there are no absolute benchmarks. Of particular relevance, what

constitutes dangerous optimism in a bear market will often not be a

problem in a bull market and what constitutes extreme fear/pessimism in a

bull market will often not signal a good buying opportunity in a bear

market. In other words, context is critical when assessing sentiment.

Unfortunately, the context is always a matter of opinion.

We have

mentioned the above sentiment issues many times over the years, but

there's a third potential pitfall that we don't recall mentioning in the

past. It mainly relates to the sentiment indicators that are based on

surveys.

Regardless of what the surveys say, there will always be a

lot of bears and a lot of bulls in any financial market. It must be this

way otherwise there would be no trading and the market would cease to

function. As a consequence, if a survey shows that almost all traders are

bullish or that almost all traders are bearish it means that the survey

has a very narrow focus. In other words, the survey must be focused on a

small fragment of the overall market.

There is no better example

of sentiment's limitations as a market timing indicator than the US stock

market's performance over the past few years. To show what we mean we'll

use the results of the sentiment survey conducted by Investors

Intelligence (II), which has the longest track record** and is probably

the most accurate of the stock market sentiment surveys.

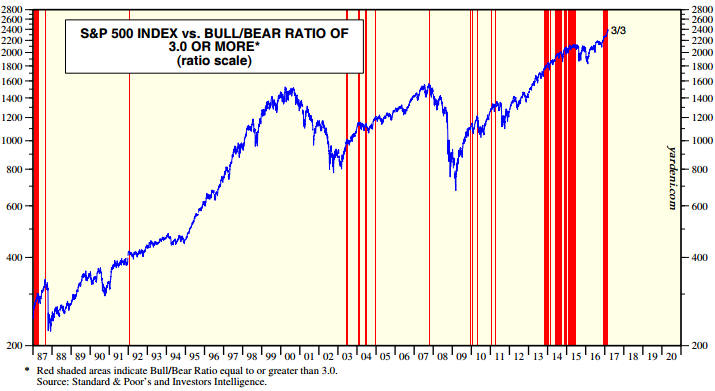

The

following chart from Yardeni.com

shows the performance of the S&P500 Index (SPX) over the past 30 years

with vertical red lines to indicate the weeks when the II Bull/Bear ratio

was at least 3.0 (a bull/bear ratio of 3 or more suggests extreme optimism

within the surveyed group).

Notice that vertical red lines

coincided with most of the important price tops (the 2000 top was the big

exception), but that there were plenty of times when a vertical red line

(extreme optimism) did not coincide with an important price top. Notice,

as well, that optimism was extreme almost continuously from Q4-2013 to

mid-2015 and that following a correction the optimistic extreme had

returned by late-2016.

In effect, sentiment has been consistent

with a bull market top for the past 3.5 years, but there is not yet any

evidence in the price action that the bull market has ended.

The bottom line is that sentiment can be a useful indicator, but it

does have serious limitations. It is just one medium-sized piece of a

large puzzle.

*In the 5th December 2016

Weekly Update

**The II sentiment data goes back to

1963

Commodity and T-Bond

prices are breaking out to the downside

Commodities

The gold price has broken below support at $1220, but gold is

fundamentally different from every other commodity and is always

considered separately in these pages. When we use the word "commodity" we

are referring to things that are consumed, such as oil or copper or

soybeans or cocoa or cotton. Our main concern is usually with what we

refer to as the industrial commodities, a category that includes the

energies (oil, natural gas, coal, etc.) and the industrial metals (copper,

zinc, etc.). Oil and copper, two of the most important industrial

commodities, have just broken out to the downside on their respective

price charts.

With regard to the oil market, this is how we

concluded a brief discussion in the latest Weekly Update:

"We

see the potential for oil to quickly move up to $58-$62 before making a

multi-month top, but we expect it to be trading substantially lower in

three months' time.

Note that a daily close above $55 would be an

upside breakout and a daily close below $51 would be a downside breakout.

A downside breakout would suggest that a multi-month top was already in

place."

A downside breakout (a daily close below $51) happened

on Wednesday 8th March. It therefore looks like oil's rally from its

November low ended last month and that an intermediate-term decline has

begun. We doubt that this decline will result in the January-2016 low

being tested, but we expect to see oil trading below $40 within the next

three months.

As an aside, oil's rally from its early-November low

was linked to the stock market's rally, so the evidence that oil's rally

is over adds to the reasons to be concerned about short- and

intermediate-term downside risk in the stock market.

With regard to the copper market, a definitive breakdown would require

a daily close below lateral support at $2.60, which hasn't yet happened.

However, the daily close below the 50-day MA on Tuesday 7th March is a

warning that a breakdown is coming.

Below $2.60 there is strong

support at $2.45 and in the low-$2.30s. We won't be surprised if the price

rebounds from $2.60 to as high as $2.70, but we suspect that an

intermediate-term decline is underway and that the price will fall at

least far enough within the coming three months to test the lower of the

aforementioned support levels.

Note that this bearish

short-to-intermediate-term outlook for copper applies to industrial metals

in general, as they are mostly in sync with each other (as is often the

case).

Treasury Bonds

In the latest Weekly Update, we

wrote:

"...the recent price action in all markets, not just the

bond market, opens up an alternative possibility. The alternative is that

there will be a plunge in TLT [the iShares 20+ Year Treasury ETF] to well

below its December low before a substantial counter-trend rally gets

underway.

With reference to the following chart, important support

lies at 118 and important resistance lies at 122. A daily close above 122

would point to a rally extension to as high as 128-130, while a daily

close below 118 would suggest that the alternative scenario mentioned

above was in play."

TLT closed slightly below 118 on Wednesday

8th March, so the alternative scenario appears to be in play.

We expect that if TLT breaches its December-2016 bottom then bond

market weakness (rising interest rates) will become a big problem for the

stock market. In other words, we could soon have even more reason to be

concerned about downside risk in the stock market.

The Stock Market

The US

Did SNAP ring a bell?

The founders

of Snap Inc. (SNAP) rang the NYSE opening bell a week ago, but the above

question pertains to whether the listing of SNAP at a blatantly ridiculous

valuation and the rocketing of the share price to a premium of 50% to the

aforementioned ridiculous valuation during the first two days of trading

marked an important top.

The absurdity of the company's market

valuation is underlined by it supposedly being worth:

a) About

65-times annual sales revenue

b) About the same as eBay

c)

About 3-times as much as Twitter

This is despite the company being

spectacularly unprofitable. So unprofitable, in fact, that for every one

dollar of sales, it loses more than one dollar (its annual losses are

greater than its annual sales revenue). And yet, the IPO was apparently

about 10-times oversubscribed!

SNAP's IPO valuation and subsequent

trading performance are such obvious signs of excess that it may well

represent the proverbial bell that rings to announce a market top. It

probably didn't 'announce' a major top, but it could well have ushered in

a top that holds for at least a few months.

Current Market Situation

The SPX

has pulled back from its 1st March high of 2401, but it has been a very

minor correction to date. It could evolve into something far more

significant, but there could also be a surge to a new high within the

coming 1-2 weeks prior to the start of a far more significant correction.

Either of these possible outcomes would be consistent with our

expectations.

Emerging Market Equities

EEM (the iShares

Emerging Markets ETF) is a proxy for "emerging market" equities in US$

terms. It reached its peak for the year of US$39.15 on 23rd February.

Interestingly and as shown on the following daily chart, the February peak

coincided with a trend-line drawn through the 2014 and 2015 peaks.

The pullback from the February peak is minor to date but will start to

look significant if there's a daily close below $37.

Downward trends in EEM tend to be driven by at least one of the

following:

1) Strength in the US$

2) Weakness in commodity

prices

3) Weakness in the US stock market

Our favoured 1-3

month scenario encompasses all three of the above, so we perceive

substantial downside risk in EEM. That's why, as mentioned in the past few

Weekly Updates, we have purchased June EEM put options for our own

account.

Our purchase of EEM puts was made primarily for hedging

(that is, insurance) purposes, but a position in EEM puts could also be a

reasonable speculation for traders who are familiar with options.

We have added an EEM June-2017 $35 put-option position to the TSI Stocks

List based on the expectation that EEM will drop to $34 or lower within

the coming three months. The closing price for this option on Wednesday

8th March was US$0.46 while the closing bid-offer spread was $0.50-$0.55.

For record purposes we'll take the middle of the bid-offer spread, that

is, $0.525, as our starting price.

It would be reasonable to set a

daily EEM close above $39.15 as an initial stop for this trade.

Gold and the Dollar

Gold

In

the latest Weekly Update, we wrote:

"...we now have a

preliminary signal that a short-term top is in place [for the US$ gold

price]. Furthermore, given the bearish divergence in the HUI/gold ratio in

the weeks leading up to last week's reversal in the gold price it's likely

that the preliminary signal of a top will be followed by a more conclusive

signal.

A more conclusive signal would be a daily close below

lateral support at $1220, which could happen as soon as this week but

might not happen until late-March or early-April."

The gold

price closed below $1220 on Tuesday and extended its decline on Wednesday,

so the more conclusive signal of a short-term top is now in place.

Both gold and silver reached their 50-day MAs on Wednesday 8th March

and the gold-mining stocks have begun to show some resilience, which

suggests the potential for a rebound over the next few days. However, this

is not something to bet on, because despite the recent sell-off the

short-term risk/reward is far from bullish. Furthermore, after shifting

far enough in a bullish direction to turn neutral a few weeks ago, the

fundamental backdrop is back to being gold-bearish thanks to the recent

rise in real US interest rates (as indicated by TIPS yields).

We

think that a better buying opportunity is coming and would view

significant near-term price strength as an opportunity to do some

additional hedging.

Gold Stocks

The HUI

extended its decline over the first three days of this week, although it

held up fairly well considering the weakness in metal prices. It has now

fallen far enough that its 50-day MA should act as a ceiling during the

next significant rebound.

A test of the December-2016 low (160) looks inevitable, but there are

many paths that could be taken to get there. For one example, with the

market now 'oversold' there could be a rebound to as high as 200 before

the downward trend resumes. In this case, the December-2016 low wouldn't

be tested until April or May. For another example, there's a risk that

panic will soon set in, leading to the December-2016 low being tested

within the coming fortnight.

Of the two possible paths mentioned

above, the latter would be the easier to trade. This is because the

intense emotions associated with a panic sell-off create buying

opportunities that are both terrific and obvious for anyone with plenty of

cash who 'keeps their head'.

The Currency Market

The Dollar Index is again challenging resistance at 102. This is the

resistance that must be decisively breached to remove the remaining doubt

that a correction low was put in place in early-February.

The stage is set for the market reaction to the monthly US Employment

Report on Friday 10th March to clearly signal whether or not the US$

correction that began in December is over. It is probably over, but a

failure to end this week above 102 would leave open the possibility of a

decline to as low as the 200-day MA (currently at 98.1) prior to a

correction low.

Note that the coming Employment Report will have to

be extremely weak or extremely strong to have any effect on market

expectations regarding the Fed's likely actions.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

![]()