![]()

![]()

![]()

![]()

- Interim Update 8th April 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The Stock Market

Valuation Update

How did the February-March crash in the US stock market affect

long-term valuation measures? Does the market now offer good value?

The answer to the first question is that the market's valuation at the

end of March was significantly more attractive than it was a month

earlier. However, the answer to the second question is that the market

remains a large distance above its long-term average value.

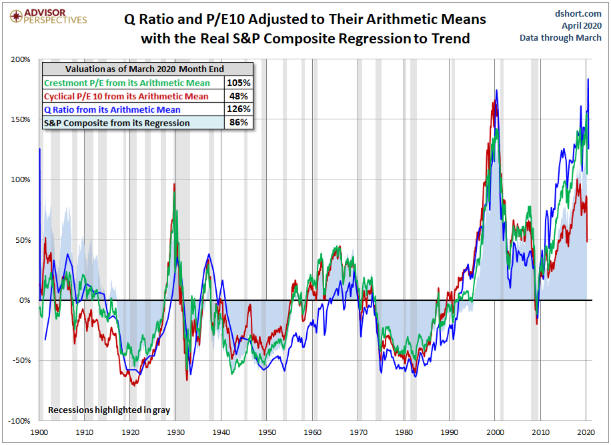

The

following monthly chart shows a few different measures of the SPX's

valuation relative to long-term averages. Of these measures, we prefer the

Cyclical P/E 10 (the red line). Of the valuation measures included on

the chart, this happens to be the one that is closest to its long-term

mean. Even so, it indicates that at the end of March the SPX was 48% above

its long-term average value, meaning that the SPX would have to fall by an

additional 30% or so to reach fair value.

Source:

dshort

It has been argued that today's extremely low interest

rates justify a much higher than average stock market valuation. One

problem with this argument is that interest rates aren't going to stay

near current ultra-depressed levels for decades to come. Actually,

considering what governments and central banks are now doing in an effort

to counteract both the immediate problem of virus-related lockdowns and

the underlying problem of excessive indebtedness, it's likely that

interest rates will commence major upward trends this year.

Before

leaving the valuation issue, it's appropriate to point out the huge

valuation difference between the present time and 1918-1919. As is the

case today, economic activity during 1918-1919 was severely curtailed due

to a pandemic. Unlike today, however, in 1918-1919 private-sector debt

levels were low and the SPX's valuation was well below its long-term

average. An implication is that we shouldn't expect something akin to the

"Roaring 20s" over the coming decade, although it's possible that the

massive depreciation of money could enable the SPX to make a new all-time

high in nominal dollar terms within the next three years.

Current Market Situation

We expected a rebound from the

March crash low that retraced about half of the crash. For the SPX, this

meant that we expected a rebound to around 2800. Wednesday's high was

2760. This could be almost as good as it gets for now, or there could be

an extension of the rebound over the coming week or so. There is no way of

knowing.

With the initial post-crash rebound having run (or almost run) its

course it is appropriate to consider what comes next. We have made it

clear that we expect a test of the crash low, but there are always

multiple realistic possibilities. Even a test of the crash low encompasses

two very different scenarios, in that the test could be successful

(meaning: the market reverses upward from either slightly below or

slightly above the March low) or unsuccessful (meaning: the market breaks

through the March low and resumes the downward trend that began in

February).

We think that the myriad of short-to-intermediate-term

scenarios can be boiled down to three main ones. They are:

1) The

SPX's initial post-crash rebound ends soon and is followed by a decline to

the vicinity of the March low. The test of the low is successful and a

larger/longer rebound gets underway.

2) There is some corrective

activity over the weeks ahead, but the SPX remains well above its March

low. That is, there is no test of the low. After pulling back, the market

resumes the short-term upward trend that began on 24th March.

3)

The same as Scenario 1, except that the test of the March low is not

followed by a tradable rally. Instead, the SPX continues downward in fits

and starts, thus confirming that we are dealing with a major bear market.

Scenarios 1 and 2 probably require the general relaxation within the

next three months of the restrictions that have been imposed by

governments to limit the spread of the coronavirus, with a large

percentage of the population returning to work before the middle of the

year. These scenarios probably also require significant progress in the

identification of existing drugs that can be used to alleviate the

COVID-19 symptoms and greatly reduce the risk of death.

We think

that Scenario 1 is the most likely, because a) crash lows are usually

tested, b) we expect that common-sense will prevail with regard to getting

people back to work in the short-term, perhaps with the mandated use of

protective gear such as masks, and c) there is already evidence that some

existing drugs are effective in speeding the recovery from COVID-19. At

this stage, however, Scenario 3 cannot be ruled out.

It should be

pointed out that Scenario 1 does not imply the resumption of the long-term

bull market following a test of the March low. It implies nothing more

than a rally lasting at least a few months. It's possible that the

depreciation of money stemming from the inflationary programs introduced

by central banks and governments will enable the SPX to reach a new

all-time high as soon as 2022, but we wouldn't have to believe that a move

to all-time high territory was underway in order to profit from the rally

that would follow a successful test of the March low.

Arguing

against a test of the March low, that is, in favour of Scenario 2, is that

the vast majority of market participants and analysts appear to be

expecting a test. This widespread expectation could mean that even if

there is going to be a test of the low, before reversing downward the

market will move high enough to draw-in many of the sceptics.

We

continue to view 2800-2900 (for the SPX) as a realistic target range for

the initial post-crash rebound and we continue to think that the odds

favour a test of the March low (a decline to anywhere in the 2100-2300

range would qualify) after the initial rebound runs its course.

In

anticipation of the aforementioned test, the SPY June-2020 $230 put option

will be added to the TSI List if it trades at US$5.00 by the end of next

week. The option ended Wednesday's session at around $6.40 and we estimate

that for it to become available at our stipulated buy price the SPX will

have to rise to around 2850.

Gold and the Dollar

Gold

In

the latest Weekly Update, we wrote:

"The price action is

non-committal, but our guess is that gold will work its way towards a

May-June correction low, just like it did during the same period last

year. Due to the chaotic financial-market environment and the 1987

comparison, the correction could entail a quick spike to a new multi-year

high."

The following chart shows what we meant by our

reference to the 1987 comparison. Notice that in December-1987 the US$

gold price spiked to a new high for the year (with silver at a much lower

high) before embarking on a multi-month decline.

The spike to a new high for the year on Tuesday 7th April currently

looks similar to the December-1987 spike. The similarity with 1987-1988

will be underlined if at some point over the next few weeks the gold price

breaks below $1560 and eliminated if gold closes above the 7th April high

anytime soon.

The fundamental backdrop remains bullish for gold, but the large

speculator net-long position in gold futures and gold's extreme

expensiveness relative to other metals suggests that the bullish

fundamentals are fully discounted by the current price. Therefore, despite

the bullish fundamentals this is a time for gold investors to be cautious.

Silver

In our most recent two commentaries we

wrote that silver's initial post-crash rebound might have peaked a couple

of weeks ago near $15, but that it was still possible for an extension to

around $16. Recall that $15.50-$16.50 was the target range we originally

had in mind for the rebound that kicked off during the final week of

March.

The silver price almost made it to $16 during the first two

days of this week and then reversed downward. There's a good chance that

the post-crash rebound has ended and that a decline to test the crash low

has begun.

Gold Stocks

As is the case with the broad

stock market, there is more than one plausible short-term scenario for the

gold mining sector. In fact, the first two scenarios outlined above for

the SPX also apply to the HUI. The scenario involving a successful test of

the crash low is the more likely, because the historical record tells us

that crash lows are almost always tested, but there is a realistic chance

that the HUI's short-term upward trend will continue for a while with only

routine pullbacks along the way.

At the moment, from our

perspective the main difference between the broad stock market's

short-term risk/reward and the gold sector's short-term risk/reward is

that "Scenario 3" does not apply to the gold sector. That is, we don't

think there is a realistic chance of the gold mining indices and ETFs

making sustained breaks below their March-2020 lows over the months ahead.

This is because the sort of economic environment that would result in

confirmation of a major equity bear market would be bullish for gold and

the related mining stocks.

Moving on, the following excerpt from

last week's Interim Update remains relevant:

"...another test

of the 200-day MA could happen within the coming week or so, but unless

the HUI is able to achieve consecutive daily closes above its 200-day MA

the prudent assumption will be that the initial post-crash rebound is

complete and that a test of the crash low is coming. Therefore, near-term

strength should be viewed as a short-term selling/hedging opportunity.

There's a good chance that the crash low will be tested and a very

good chance that if it is tested the test will be successful (the March

low won't be breached). Therefore, if the HUI drops back to the 150s at

some point over the next two months you should just grit your teeth and

buy gold mining ETFs and/or stocks."

As illustrated below,

another test of the HUI's 200-day MA (the red line on the chart) happened

during the first half of this week.

Unless the HUI achieves consecutive daily closes above its 200-day MA,

the prudent assumption will be that the next significant move is to the

downside.

The Currency Market

The Dollar

Index (DX) is chopping around near the middle of its recent wide range.

Plausible fundamental arguments can be made for both a much stronger US$

and a much weaker US$ over the quarters ahead, but we suspect that the

downward pressure on the DX being exerted by the Fed eventually will trump

(no pun intended) all other considerations. Let's put it this way: If the

Fed's actions prove to be insufficient to create general weakness in the

US$, then the Fed will do more...and more...and more...until the US$

buckles. Unlike the ECB, the Fed will not face any short- or

intermediate-term political obstacles in its efforts to inflate.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

![]()