![]()

![]()

![]()

![]()

- Interim Update 8th July 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Industrial Commodities

The Natural Gas 'double

bottom'

A week ago we wrote that the natural gas (NG)

price had just reversed upward after testing its April low, which was

preliminary evidence that it may have set a cycle low via a double bottom.

Some additional upward progress has since been made, but the price remains

within its 6-month trading range. Additional preliminary evidence that a

cycle low is in place would be provided by a daily close above the 200-day

MA (slightly above US$2.00 on the following chart), while a weekly close

above the early-May high would be definitive.

The current rebound in the NG price is happening in the face of

bearish fundamentals. In particular, the large contango in the NG futures

market tells us that currently there is a substantial surplus of the

physical commodity in the US. However, we continue to anticipate a

tightening of the market within the next several months. This is partly

due to an increase in demand as the economy opens up and as government

efforts are made to boost economic activity ahead of the November

election, but it is mainly due to the decline in production that should

stem from the large decline in drilling activity that has already

occurred.

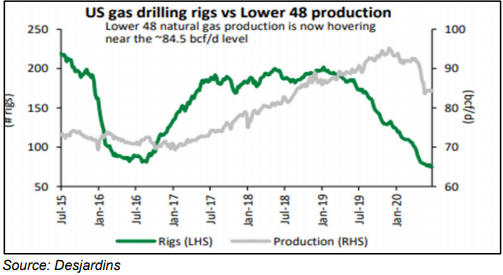

Displayed below is a chart from the latest Peyto

Exploration and Development (PEY.TO)

President's Report showing the trends in NG production (the grey line)

and the number of drilling rigs (the green line). Notice that the grey

line follows the green line with a substantial lag. NG production began to

decline late last year and, based on the drilling rigs trend probably will

decline over the remainder of this year.

Oil threatens to break out to the upside

The

oil price and the US stock market have been positively correlated over the

past 2-3 years. This relationship is illustrated by the following daily

chart, which shows the oil price in black and the S&P500 Index (SPX) in

red.

The chart reveals two notable 4-6 week divergences. The first

occurred during January-February when the SPX continued to rally while the

oil price began to trend downward, and the second occurred in March-April

when the oil price crashed to a new multi-year low while the SPX extended

its upward trend. However, after each of these divergences the markets

quickly moved back into line with each other.

We are revisiting the oil-SPX relationship today because it relates to

our short-term (1-3 month) outlook for oil.

The following daily

chart shows that the oil price essentially has traded sideways since

rising to the $40-$42 resistance range in early-June. We are expecting

resistance at $42 to hold and for the market to experience a $5-$10

correction in the short-term, but for this to happen there probably will

have to be a meaningful short-term correction in the US stock market. If

there isn't and instead the SPX makes a solid break above its early-June

high, then the oil price probably will breach resistance at $42 and rise

to the mid-to-high $40s.

Is the uranium correction over?

In mid-April

we wrote that uranium (and the associated mining stocks) probably had

commenced a cyclical bull market, and near the end of April we wrote that

a short-term correction was likely. The first short-term correction in a

new bull market often ends near the 50-day MA, although it isn't uncommon

for the price to fall as far as the 200-day MA before the longer-term

upward trend resumes.

In the 22nd June Weekly Update we noted that

Cameco (CCJ), the world's second-largest uranium producer, had reached its

50-day MA and may have completed its correction, but at that time there

was still a risk that the short-term price decline would extend to the

200-day MA. There will be room for uncertainty until CCJ makes a solid

break above US$11.00, but over the first two days of this week the

probability increased that the correction is complete. If it is complete

then resistance at US$13 is a logical short-term target.

Due to the preliminary evidence that the uranium correction is over we

are going to add a new uranium-related speculation to the TSI List. We

have chosen Energy Fuels (NYSE: UUUU, TSX: EFR), because the company:

a) Has a strong balance sheet, with US$35M of working capital and no

long-term debt.

b) Offers leverage to an increase in the uranium

price by virtue of its ability to quickly ramp up production in response

to a higher uranium price and its substantial in-ground resources.

c) Immediately benefits financially from a higher uranium price due to

having 520K pounds (worth about US$17M at today's price) of saleable

uranium in its inventory.

d) Is based in the US, which puts it in a

position to benefit from US government efforts to increase the security of

uranium supply.

e) Offers exposure to vanadium in addition to

uranium.

The company has conventional uranium mines and the only

fully-functional conventional uranium mill in the US. It also owns ISR (in

situ recovery) uranium projects in the US. However, it has no current

production due to having placed its operating mines on

care-and-maintenance pending a higher price for the commodity.

The

company has 115M shares outstanding, giving it a market cap of US$185M at

Wednesday's closing price of US$1.61.

The following daily chart

shows that UUUU has been in correction mode since late-April. There is no

evidence in its price action that the correction is over, but if CCJ's

correction is complete then so, in all likelihood, is UUUU's.

UUUU

has been added to the TSI List at US$1.61 as a trade with an expected

duration of 6-12 months. We will use a 20% trailing stop loss (TSL), which

means that the initial daily-closing stop will be at US$1.28.

At current prices the lowest-risk way to obtain exposure to uranium is

to buy the Uranium Participation Fund (U.TO), a fund that holds physical

uranium. At its closing price of C$4.93 on Wednesday 8th July this fund

was trading at a 15% discount to its net asset value.

The Stock Market

Our Equity True Fundamentals

Model (ETFM), which had been bearish since February, shifted to neutral at

the end of last week. Given the magnitude of the stock market's rally from

the March-2020 low this is a belated signal, but it supports our view that

the SPX will not revisit its March-2020 low over the remainder of this

year and that the realistic worst-case scenario is a correction that

retraces about half of the March-June up-move.

Depending on which

market proxy you use, you could make the case that the US stock market has

been in correction mode for about a month or is yet to enter correction

mode. For example:

1) The NASDAQ100 Index (NDX) made its most

recent all-time high on Tuesday of this week and clearly has not yet begun

to 'correct'. Notice that all pullbacks since late-April have ended

at/near the 20-day MA, so a solid break below the 20-day MA will signal

that a correction has begun.

2) The S&P500 Index (SPX) pulled back to its 200-day MA last month and

remains below the rebound high made in early-June, but it is yet to

experience a correction worthy of the name.

3) The Dow Industrials Index broke below its 200-day MA about a month

ago and appears to be in correction mode.

4) The NYSE Composite Index (NYA), a better proxy for the overall

market than any of the indices mentioned above, barely made it up to its

200-day MA last month before reversing course. At the close of trading on

8th July it was 15% below its January-2020 all-time high and 5% below its

June-2020 post-crash rebound high.

We expect further corrective activity, or in the case of the NDX the

start of a correction. However, it's possible that due to additional

support from both the Fed and the government over the next few months,

instead of getting significant weakness in the broad market we will get a

rotation involving a shift from 'growth' (best represented by the NDX) to

some of the sectors that already experienced meaningful corrections (for

example, banks and energy).

Gold and the Dollar

Gold and Silver

The Ratio

Gold is more

money-like and silver is more commodity-like. Consequently, the

relationships that we follow involving the gold/GNX ratio (the gold price

relative to the price of a basket of commodities) also apply to the

gold/silver ratio. In particular, gold, being more money-like, tends to do

better than silver when inflation expectations are falling (deflation fear

is rising) and economic confidence is on the decline.

Anyone armed

with this knowledge would not have been surprised that the collapse in

economic confidence and the surge in deflation fear that occurred during

February-March of this year was accompanied by a veritable moon-shot in

the gold/silver ratio*. Nor would they have been surprised that the

subsequent rebounds in economic confidence and inflation expectations have

been accompanied by strength in silver relative to gold, leading to a

pullback in the gold/silver ratio. The following charts illustrate these

relationships.

The first chart compares the gold/silver ratio with

the IEF/HYG ratio, an indicator of US credit spreads. It makes the point

that during periods when economic confidence plunges, the gold/silver

ratio acts like a credit spread (credit spreads rise (widen) when economic

confidence falls).

The second chart compares the silver/gold ratio

(as opposed to the gold/silver ratio) with the Inflation Expectations ETF

(RINF). It makes the point that silver tends to outperform gold when

inflation expectations are rising and underperform gold when inflation

expectations are falling.

We are expecting a modest recovery in economic confidence and a big

increase in inflation expectations over the next 12 months, meaning that

we are expecting the fundamental backdrop to shift in silver's favour. As

a result, we are intermediate-term bullish on silver relative to gold. We

don't have a specific target in mind, but, as mentioned in the 16th March

Weekly Update when the gold/silver ratio was 105 and in upside blow-off

mode, it isn't a stretch to forecast that at some point over the next

three years the gold/silver ratio will trade in the 60s.

Be aware

that before silver commences a big up-move in dollar terms and relative to

gold there could be another deflation scare. If this is going to happen it

probably will do so within the next three months, although we hasten to

add that any deflation scare over the remainder of this year will be far

less severe than what took place in March.

*The

gold/silver ratio hit an all-time intra-day high of 133 and daily-closing

high of 126 in March of this year. This was one of the many unprecedented

market/economic events of 2020.

The

recent price action

The following daily chart shows that the

US$ gold price has broken above lateral and round-number resistance at

$1800. Surprisingly, this happened to minimal fanfare. Almost all

attention, it seems, is focused on the likes of Amazon (AMZN) and Apple

(AAPL). This is a plus because it implies that the 'unwashed masses',

which obviously don't include any TSI subscribers, are yet to become

enamoured of gold.

The retail investing herd becoming enamoured of

gold is something that's likely to happen over the next 12 months --

beginning after the FAANG bubble springs a leak. We expect that during the

same period the herd also will become very enthusiastic about industrial

and agricultural commodities. In fact, on an intermediate-term basis we

are more bullish on the likes of zinc and nickel than we are on gold, but

the short-term risk/reward favours gold.

Note that the break above

US$1800 still has to be confirmed by the weekly close. It also has to be

confirmed by the euro gold price, which is still below its April high.

Our guess is that the US$ gold price will make a multi-week top within

the coming week or so, pull back to either its 20-day MA or its 50-day MA,

and then resume its upward trend.

The US$ silver price has

achieved a daily close above resistance at $19.00. This resistance capped

the upside in January, February and May of this year, so the breakout is

significant. But as is the case with gold, the breakout requires

confirmation from the weekly close.

Gold Stocks

The HUI closed above long-term

resistance at 286 (the 2016 high) on Tuesday of last week and above

short-term resistance defined by its May-2020 high on Tuesday of this

week, meaning that it has just made a new 7-year high. This is more

evidence that we are dealing with the completion of a long-term base that

projects much higher prices over the coming year or two, regardless of

what happens over the next few weeks.

Importantly, this week's move to a new multi-year high was confirmed

by the HUI/gold ratio. The following daily chart shows that the HUI/gold

ratio held above its 150-day MA during the May-June decline, thus keeping

the decline within the bounds of a routine short-term correction, and has

just (on Wednesday 8th July) moved above its May high.

With regard to the HUI's short-term prospects, our guess is the same

as it is for gold bullion. We suspect that there will be a multi-week top

within the coming week or so followed by a pullback to either the 20-day

MA or the 50-day MA, after which the upward trend should resume. Downside

risk will become much greater if the upward trend continues until

September with only minor interruptions along the way, but we'll cross

that bridge if/when we come to it.

The Currency Market

The Dollar Index (DX) made a minor downside breakout over the first

three days of this week. We are referring to the break below the bottom of

the short-term channel drawn on the following daily chart. However, on a

risk/reward basis there hasn't been a significant change.

We expect

that over the next two months the DX will trade 'choppily' between 94.5

(its March-2020 low) and 98.5. In other words, we expect that it will

trade at its current level +/- about 2 points. This is due to the likely

effects of countervailing forces, with a shift away from risk putting

upward pressure on the DX at some point and the on-going profligacy of

both the Fed and the US government maintaining downward pressure on the

DX.

The direction of the next big move is more likely to be down

than up due to the downward forces mentioned above as well as the US stock

market becoming a global laggard.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

![]()