![]()

![]()

![]()

![]()

- Interim Update 8th August 2018

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The Stock Market

More Tesla (TSLA)

Tesla CEO Elon Musk may be going insane. On Tuesday he 'tweeted' that

he was considering taking TSLA private at $420/share and that the

financing for such a transaction was secured. This drove the share price

up 11% to about $380, a price area that coincides with the stock's

all-time high. This is a sign of insanity on Musk's part because a) if he

doesn't follow through and show that financing actually is in place then

he will have opened himself up to a class action lawsuit from

short-sellers and charges from the SEC, and b) there is almost no way that

such a transaction could be financed, even in the current easy-credit

environment.

Leveraged buyouts can only work if the company being bought has strong

positive cash-flow to cover the interest payments on the debt. TSLA is

therefore not candidate for such a buyout. However, perhaps Musk has found

some large investors who would buy the equity without saddling the company

with additional debt. It's hard to imagine that anyone with access to the

many billions of dollars required for such an endeavour (at $420/share

TSLA's market cap would be about $72B) would be dumb enough to buy this

floundering, cash-hemorrhaging company, although the Saudi royal family

can't be ruled out as a potential buyer.

In any case, from our

perspective TSLA remains in the 'too hard basket'. It is too risky to buy

and too risky to sell.

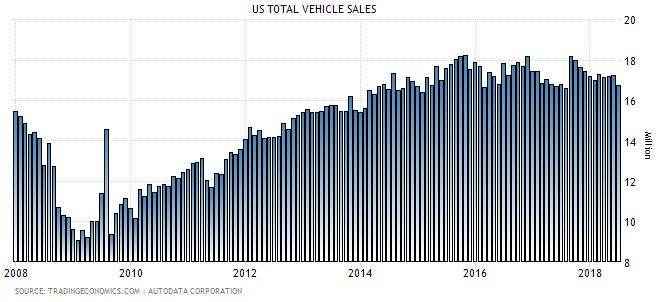

Peak Autos?

Tesla is

unique in many ways and is absurdly expensive relative to other

US-domiciled car manufacturers, but even the ones that look cheap based on

traditional valuation measures probably should be avoided. The reason is

that US motor vehicle sales may have reached a cyclical peak last year.

As illustrated by the following chart, monthly US vehicle sales have

been trending downward since last September and are no higher today than

they were during the first half of 2014. And with interest rates now in a

long-term upward trend the opportunity no longer exists for car makers to

attract legions of new customers with low-cost financing deals.

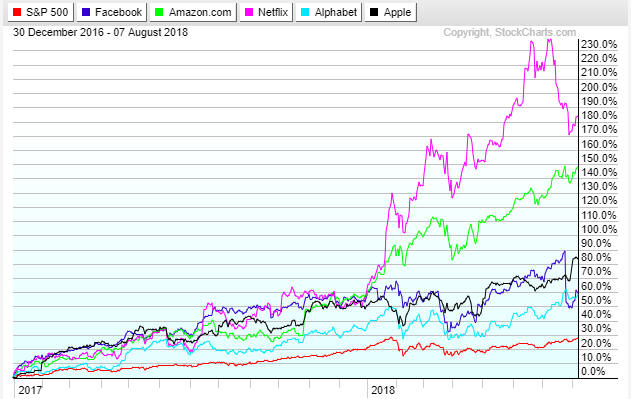

Current Market Situation

Over the past two

years the US stock market has been dominated by a small group of stocks

affectionately known as the FAANGs (Facebook, Amazon, Apple, Netflix and

Alphabet (Google)). The following chart compares the performances of these

five stocks with the S&P500 Index (SPX) since the beginning of 2017. The

SPX is the red line.

Notice that over the past month two of the

FAANG stocks (Netflix and Facebook) have plunged. This could be

significant, because when the leaders of a major upward trend start to

fall away it usually means that the market's upward trend is almost over.

The SPX has moved back to within 1% of its January high and its

channel top. It therefore can't rise much further without invalidating our

interpretation of the overall market situation.

By the way, the

bottom section of the following SPX chart shows the Common-Stocks-Only

NYSE Advance-Decline Line. This measure of the market's internal strength

barely skipped a beat during the January-February market correction and

made a new high as recently as Tuesday of this week. This is evidence that

the bull market is intact, but it doesn't preclude a tradable 1-3 month

decline.

The NASDAQ100 Index (NDX) has just risen for seven days in a row

without managing to exceed its July high. To validate our current view of

the world a downward reversal must happen very soon.

Gold and the Dollar

Gold

Another look at gold market sentiment

When analysing financial markets and the economy it is possible to

have too many indicators. The optimum number to have is the smallest

number that enables an accurate assessment of the situation being

analysed. Once you have enough indicators to reliably get an accurate

appraisal, adding more will muddy the waters. In simple terms, more

information is not always a good thing.

For example, when assessing

the probable timing of the next US recession we only care about three

indicators. These indicators, when taken together, have a near perfect

record over at least the past 60 years. There are countless other economic

indicators that can provide interesting and potentially-useful

information, but incorporating any of these other indicators into our

analysis will not be helpful if our sole objective is to figure out the

most likely timing of the next recession.

For another example, when

assessing gold market sentiment we take into account the results of two

surveys and certain aspects of the COT (Commitments of Traders) reports.

That's it. We are aware of many other gold-market sentiment indicators and

always remain open to the possibility that there are better tools out

there than the ones we are using, but we won't take an indicator seriously

unless it has proved itself over a long period under various market

conditions.

The above discussion leads us to the main point we want

to address. Due to it recently having reached an extreme, we have

revisited a gold-market sentiment indicator to which we normally don't pay

close attention. We are referring to an aspect of the COT data called the

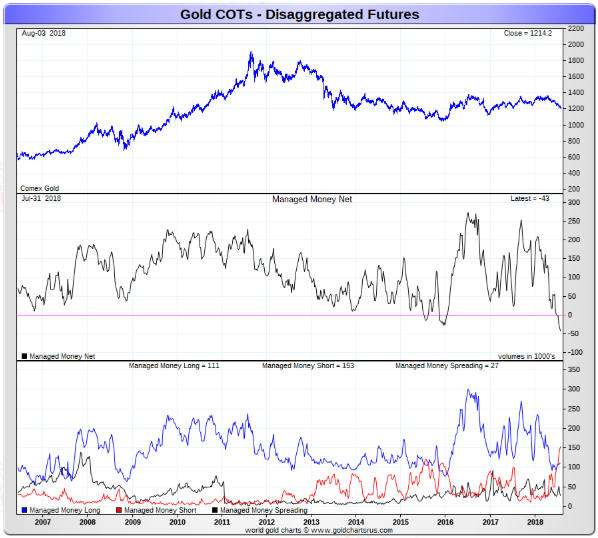

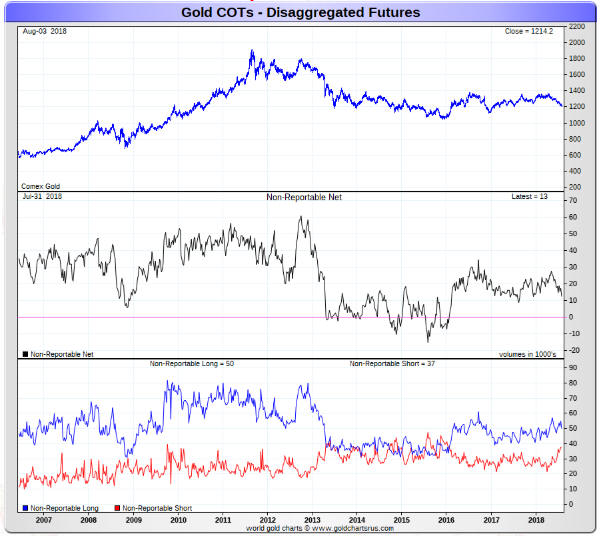

"Managed Money"* net position.

The black line in the middle section

of the following chart shows that the "Managed Money" net-long position in

gold futures, which tends to move up and down with the gold price, hit a

10-year low last week. This suggests that money managers, as a group, were

even more bearish on gold last week than they were at the December-2015

multi-year price bottom.

With sentiment being a contrary indicator, does this mean that the COT

situation is more bullish now than it was in December-2015?

No,

because the middle section of the next chart shows that the

"NonReportable" traders (the proverbial dumb money) are nowhere near as

negative towards gold as they were at the December-2015 price bottom. Back

then they were net-short by about 8K contracts whereas last week they were

net-long by 13K contracts.

Also, it's worth mentioning that the "Managed Money" net-long position

in silver futures hit a 10-year low in early-April. This was a misleading

signal because, as noted in TSI commentaries at the time, the overall COT

situation for silver was no better than neutral back then (and, by the

way, is currently no better than neutral). That silver failed to do

anything interesting on the upside over the ensuing four months is

therefore consistent with the message from the COT data.

When it

comes to economics and other fundamentals we want our use of an indicator

to make sense based on both logic and historical performance, but when it

comes to measuring sentiment we only care about historical performance.

Based on what we've seen to date, the "Managed Money" net position adds no

value to what we get from other aspects of the COT data. In fact, it can

be misleading, possibly because managed money isn't inherently 'dumb

money'.

It so happens that the COT situation for gold became

decisively bullish last week for the first time this year. It is not as

bullish as it was in December-2015, but it is as bullish as it has been at

any point over the past 2 years. Furthermore, as at the end of last week

the Consensus-inc Bullish Sentiment Index for gold was only 24%, which is

a 14-year low.

*For

the purpose of the COT reports, a "money manager" is defined as a

"registered commodity trading advisor (CTA); a registered commodity pool

operator (CPO); or an unregistered fund identified by CFTC. These traders

are engaged in managing and conducting organized futures trading on behalf

of clients."

Current Market

Situation

It is fair to say that the sentiment backdrop is

now strongly supportive of the gold price. This means that there will be

plenty of fuel -- in the form of speculative short-covering and

long-accumulation -- to drive the price upward once the short-term price

trend reverses. This will be the case even if gold's true fundamentals

remain bearish, although there will not be anything more than a strong

short-term rebound in the gold price until the fundamental backdrop makes

a sustained move into bullish territory.

The immediate problem is

that there is no evidence of a reversal in the short-term price trend.

Since bottoming at US$1210 on 19th July the gold price has traded sideways

within a narrow range, leaving open the possibility that a plunge to a new

12-month low will precede the start of a tradable up-swing.

A daily

close above $1240 would signal a reversal. Also, a daily close above the

20-day MA (the black line on the following chart) would be an early

warning that an upward reversal was in the works.

Gold Stocks

From late-March to early-July

there was modest strength in the gold-mining indices/ETFs relative to gold

bullion. This was thought by many analysts to have bullish implications

for both the gold-mining sector and the bullion market, but strong rallies

in gold and the related investments usually aren't preceded by modest

relative strength in the mining stocks; they are usually preceded by

substantial relative WEAKNESS in the mining stocks. To put it another way,

it is capitulation, not stubborn optimism, by the holders of gold-mining

stocks that sets the stage for an intermediate-term rally.

Tradable rallies can start in the absence of capitulation, it's just that

the reward/risk will be much higher if the 'decks have been cleared'. We

haven't had a 'deck-clearing' plunge in the gold-mining sector yet and

there is no guarantee that we will get one, but prices are positioned in a

way that it could happen in the near future. Also, thanks to the price

action during the first half of this week it will now be easier for the

gold-mining sector to signal an upward reversal. We are referring to the

fact that during the first half of this week GDX broke below

intermediate-term support defined by numerous lows over the past 18 months

and the HUI dropped to long-term support defined by its December-2016 low.

Due to having breached obvious support at $21.00, to signal a reversal

all GDX would have to do now is close a day at $21.50 or higher. Doing so

would mark the preceding downside breakout as false. However, the downside

breakout suggests a short-term target of $18.50 and the breakout should be

respected until/unless it proves to be false.

It will be a little more difficult for the HUI to signal a reversal.

The quickest/simplest way for it to do so would be to spike at least a few

points below the obvious support at 160 and then close a day above 170.

The Currency Market

Currency market volatility

is very low at the moment, with the Dollar Index (DX) mired within the

confines of a gently-sloped rising wedge. The top of the 'wedge' is around

95.5, but there is important lateral resistance at 95 (95.07, to be

exact). The DX closed slightly above 95 on Monday and Tuesday and closed

slightly below 95 on Wednesday of this week.

A weekly close above

95.07 would be an upside breakout while a daily close below 94 would be a

downside breakout.

Our fundamentals-based model for the DX has an

interest-rate component and an equity component. The interest-rate

component is bullish for the DX if the US 10-year T-Note yield is in an

upward trend relative to the German 10-year Bund yield and the equity

component is bullish for the DX if US equities are in a strengthening

trend relative to European equities. The equity component seems to be the

more important over the long term, but there are periods when the

interest-rate component has the greater influence. We have been in such a

period over the past few months.

The following chart compares the

DX (the blue line) with the 10-year US-Germany yield spread. This chart

suggests that the direction in which the DX breaks out of its 'wedge' will

be determined by the direction in which the yield spread breaks out of its

recent narrow range.

Although we have been leaning towards the DX eventually breaking out

of its wedge pattern to the downside, the price action is about as neutral

as it can get. Note that an upside breakout by the DX potentially would

set in motion a sharp 3-6 week rally along similar lines to what happened

between late-April and late-May.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://tradingeconomics.com/

http://www.goldchartsrus.com/

![]()