![]()

![]()

![]()

![]()

- Interim Update 8th November 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Oil and Gas

Oil extends its upside

breakout

It looks like Mohammed bin Salman (MBS), Saudi

Arabia's Crown Prince, is following the lead of Xi Jinping and using a

corruption crackdown as the cover for eliminating anyone perceived as a

threat to his absolute power. All senior government and military personnel

in China are corrupt, so to find evidence that can be used against any one

of them, all you have to do is investigate. It's no doubt a similar story

in Saudi Arabia.

News over the weekend that MBS had arranged to

have dozens of influential members of the Saudi royal family, government

and business community arrested as part of an anti-corruption campaign

created fear that the dominant member of OPEC was becoming politically

unstable. When this news was added to signs of increasing tension between

Saudi Arabia and Iran, the result was a 3% rise in the oil price on Monday

and an extension of the breakout move that occurred last Friday.

Monday's surge appears to have pushed oil to the top of an 18-month

channel. At least, that's one way to interpret oil's price chart (see

below). Therefore, the oil market is now 'overbought', 'overbullish' and

near intermediate-term channel resistance. At the same time, we explain

below that the fundamental backdrop is becoming increasingly supportive

for the oil price.

Oil fundamentals becoming increasingly bullish

As we've mentioned numerous times in the past, for an industrial

commodity with a large and liquid futures market the "term structure" in

the futures market (a.k.a. the futures curve) is the most reliable

indicator of the supply-demand situation.

An upward-sloping futures

curve (earlier-dated futures priced lower than later-dated futures) is

called "contango" and is the normal state of affairs. In this normal state

of affairs a more distant futures contract will have a higher price

because of the cost of storage and financing, not because traders expect

the price to be higher in the future.

When the curve flattens, in

most cases it means that the physical supply situation is getting tighter.

Why? Because if the gap between a futures price and the spot price falls

to the point where it is less than the cost of storage then a risk-free

arbitrage opportunity will be presented to the owners of physical supply

who won't need their supply prior to the time that the futures contract

expires. They can sell their physical oil, buy the futures and make a

guaranteed profit equal to the cost that they would have paid for storage

minus the difference between the futures price they paid and the spot

price they received.

Sometimes, the futures curve doesn't just

flatten, it inverts; that is, it becomes downward-sloping. This is called

backwardation. When the oil market is well into "backwardation" it means

that a substantial risk-free profit is being offered to the owners of

physical supply who are able to do the trade described above.

Since

risk-free profit opportunities tend to be rare and fleeting, the only way

that "backwardation" can be sustained is if very few owners of physical

supply are in a position to do the trade described above. In other words,

sustained "backwardation" implies a market with minimal surplus supply,

either because inventory levels are low or because the current owners of

the physical supply are unwilling to relinquish ownership even when

presented with a large financial incentive to do so.

Here are three

charts that show the shift in the oil market's futures curve over the past

few months. The first chart shows the situation at 20th June. This is a

picture of a normal, well-supplied market. The second chart shows the

situation at 16th August, by which time the curve had flattened markedly.

This implies that oil's supply situation tightened between 20th June and

16th August, but the fact that the curve still had an upward slope

suggests that there was no shortage in mid-August. The third chart shows

the current situation. This is a picture of a market in which you get paid

significantly more to deliver a barrel of oil today than to store the

barrel and deliver it a year from now, which implies a significant supply

shortage.

The last of the above charts indicates that the fundamental backdrop

is currently bullish for the price of West Texas Intermediate Crude

(WTIC). The futures curve for Brent Crude is even more bullish, so this is

a global phenomenon and not just a peculiarity of the US market.

The oil market's backwardation may soon disappear, but the fact that it

happened at all is bullish. It's the main reason that a bearish oil

speculation is of no interest to us at this time despite the market being

stretched in momentum and sentiment terms. However, the sentiment

situation keeps us cautious with regard to oil's short-term prospects.

Natural Gas (NG) is close to an upside breakout

The NG price is testing resistance at $3.20. A weekly close above this

resistance would be an upside breakout and would suggest that NG was on

its way to a 2-year high (above $3.90).

Petrus Resources (PRQ.TO), a junior Canadian NG producer, provides

TSI's solitary exposure to NG. PRQ's bottom line would be helped by a

sustained upside breakout in the NG price, although there isn't a strong

short-term correlation between the PRQ stock price and the NG price.

PRQ has support at C$2.05 and resistance at C$2.80. A close above

C$2.80 would suggest that the stock was on its way to at least C$3.50.

The T-Bond

rebound may be almost complete

The iShares 20+ Year Treasury

Fund (TLT) tested important support near $123 in late-October and has

since rebounded. We suspect that this rebound is forming the 'right

shoulder' of a 'head and shoulders' topping pattern. If so, the rebound

should end at or below $128.

Although the rebound is probably

almost complete in terms of price, we won't be surprised if it takes TLT a

few weeks to roll over into its next downward trend.

The Stock Market

In addition to the obvious

nominal price highs, the US stock market has broken many records over the

past few months. These records include:

1. The lowest ever reading

for the Volatility Index (VIX).

2. By far the greatest number of

single-digit VIX readings in any 6-month period.

3. By far the

highest median price/sales ratio in US stock market history.

4. The

highest daily RSI for the Dow Industrials Index since at least 1980.

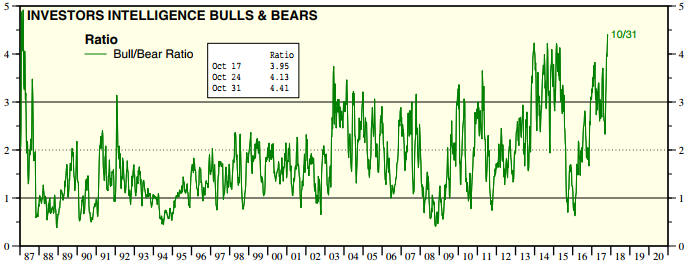

5. The highest Investors Intelligence bull/bear ratio since 1987.

The last of the above-mentioned records was achieved over the past

week and is illustrated by the following chart.

Cracks are appearing in some of the lesser indices, but the following

daily chart shows that the US stock market's most important index

continued its relentless low-volatility upward march over the first three

days of this week. All heck is going to break loose at some point,

probably for no obvious reason. Right now, however, there isn't a care in

the world.

Gold and the Dollar

Gold

In

the latest Weekly Update, we wrote:

"The fundamental backdrop

was still bearish for gold at the end of last week, although less so than

it was a couple of weeks earlier. We won't be surprised if the fundamental

backdrop switches from bearish to bullish within the next two weeks, but,

as usual, a lot will depend on what happens to the bond market."

Over the first three days of this week the fundamental backdrop

shifted in gold's favour by enough to push the GTFM into bullish

territory, although the GTFM can't officially change until the end of the

week. In other words, the weekly closing levels must confirm the shift in

order for it to register in our model.

The shift in the fundamental

backdrop reduces the risk that the gold price will plunge to the

low-$1200s prior to a short-term bottom, but, as also written in the

latest Weekly Update:

"Gold's biggest near-term threat is

sentiment, not fundamentals. Despite the roughly $100 decline in the gold

price over the past two months, speculators, as a group, remain stubbornly

optimistic."

It is certainly possible that gold will make a

short-term price bottom without a preceding purge of leveraged

speculators, but a rally that began in the absence of a solid sentiment

foundation probably would be limited in size to about $100 and limited in

time to about two months.

Important nearby support still lies at

$1260. There still could be a spike below this support prior to a

short-term bottom, but, as noted above, the risk of a plunge to the

low-$1200s has diminished over the past few days.

Gold Stocks

In the latest Weekly Update we

wrote that a) the HUI had made a 1-2 month high or low at 2-month

intervals beginning in early-March, b) the next turning point in this

2-month cycle was due immediately, and c) if the cycle was still in force

it would have to be a turn from down to up.

Based on the price

action over the first three days of this week it looks like the 2-month

cycle low was put in place last Friday (3rd November). The less-likely

alternative, assuming that the cycle remains in force, is that there will

be a sharp decline to a cycle low over the final two trading days of this

week.

If the 2-month cycle remains in effect, which currently seems

likely, then the rally that follows the early-November low should continue

until at least early-December and could continue until early-January. In

other words, as things stand today the most likely scenario is that a 1-2

month rally has just begun.

Turning to the charts, today we are

going to focus on GDX. The reason is that whereas the HUI, the XAU and

GDXJ have not yet rebounded far enough from their recent lows to challenge

any resistance levels of significance, GDX has already reached its 200-day

MA. In other words, GDX's rebound is already undergoing its first

meaningful test.

The stage is set for a daily close by GDX above

its 200-day MA to be the first evidence of an upward trend reversal.

The Currency Market

The Dollar Index (DX) has

drifted sideways for the past 8 trading sessions. This price action has

the look of a mid-trend consolidation, which means that the next

significant move is more likely to be to the upside than to the downside.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.yardeni.com/

![]()