![]()

![]()

![]()

![]()

- Interim Update 9th January 2019

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Random Predictions For

2019

1) Early last year we predicted

that the US stock market would experience greater-than-average volatility

over the year ahead. This obviously happened, as there were more 2%+

single-day moves in the SPX during 2018 than in an average year.

We

expect the same for this year, that is, we expect price volatility to

remain elevated. The reason is that the two most likely scenarios involve

abnormally-high price volatility. One of these scenarios is that a

cyclical bear market began last October, and bear markets are

characterised by periods of substantial weakness followed by rapid

rebounds. The other scenario is that a very long-in-the-tooth cyclical

bull market is about to embark on its final fling to the upside.

2)

When attempting to predict when a period of economic growth will end it is

futile to look more than 6-12 months into the future, because there are no

leading recession indicators that can predict that far ahead with

acceptable reliability. There are, however, leading indicators that can be

used to determine the probability of a recession beginning within the next

few quarters.

Early last year these indicators told us that a US

recession would not begin during the first half of the year. They

currently tell us that the US economy stands a good chance of commencing a

recession this year, most likely during the second half of the year. Note,

though, that if a recession does get underway this year it won't become

official until 2020, because recessions usually aren't confirmed by the

National Bureau of Economic Research until about 12 months after they

start.

3) Regarding 'cryptoassets', at around this time last year

we wrote:

"...it's a good bet that the Bitcoin bubble reached

its maximum level of inflation late last year. Also, the broader bubble in

cryptoassets is set to burst during the first quarter of this year."

And:

"By the end of 2018 it will be apparent that the

public's enthusiasm for Bitcoin and the "alt-coins" was one of history's

great speculative manias."

This assessment looks correct.

We don't have a strong opinion about what will happen to

'cryptoassets' in 2019. This is partly because there is no reasonable way

to determine the fair value of these assets. For Bitcoin, for example, a

price of $3,000 is no more or less sensible than a price of $30,000 or a

price of $300.

Distributed ledgers can be very useful, but there

should be ways to implement them without consuming a lot of resources. If

so, the price of Bitcoin eventually will drop to almost zero.

A

year ago we also predicted:

"Despite spectacular collapses in

the prices of the popular 'cryptoassets' during 2018, central banks

including the Fed and the ECB will firm-up plans to introduce their own

blockchain-based currencies. This will be driven by a desire to eliminate

physical cash, the thinking being that if there is no physical money it

will be more difficult for the average person to make/receive unreported

payments and escape a negative interest rate."

As far as we

know the major central banks didn't firm-up plans to introduce their own

blockchain-based currencies last year, but we continue to expect that they

will -- for the reasons mentioned above.

4) Regarding the Fed's

expected actions in 2018, early last year we wrote:

"Due to

rising commodity prices it's a good bet that "price inflation" will become

a higher-profile issue during the first half of 2018, prompting the Fed to

move ahead with its quantitative tightening (QT) and make two more rate

hikes. However, both the QT and the rate-hiking will be put on hold during

the second half of the year in reaction to increasing downside volatility

in the stock market."

We got the anticipated rate hikes during

the first half and the increasing downside stock-market volatility during

the second half of last year, but the Fed stuck to its guns. However, over

the past three weeks the Fed Chairman has made it clear that the Fed will

be quick to change direction if the stock market continues to decline

and/or the economic numbers point to significant weakness.

For 2019

we expect one Fed rate hike, most likely in June. Also, we expect that

people 'in the know' will explain to senior Fed members that it's the

balance-sheet reduction program (QT) that really counts, prompting the Fed

to slow the pace of QT during the first half and conclude the QT program

before year-end.

5) The ECB has just ended its QE program and has a

tentative plan to implement its first rate hike during the third quarter

of 2019. Given that nothing has been learned from the failed monetary

experiments of the past few years, it's a good bet that evidence of

declining economic activity in the future will be met by the ramping-up or

reintroduction of policies that failed in the past. Therefore, we predict

that the ECB will not increase its targeted interest rates this year and

will restart QE during the second half of the year.

6) This is not

a prediction for 2019, but rather an observation that could apply for

decades to come. We suspect that the age of real estate has ended.

We don't mean that from now on it will be impossible to achieve good

returns by investing in real estate, but that gone are the days when

anyone could buy a house almost anywhere and likely end up with a sizable

profit as long as they held for 10 years or more. From now on only astute

investors will consistently make good returns from real estate, where

"astute" means able to time the cyclical swings in the broad market or

able to correctly anticipate future supply-demand imbalances in specific

areas.

For the average person, residential property will transition

from an investment to what it was prior to the 1970s: a consumer good

(something bought solely for its use value).

The reason for the

change is the interest-rate trend. The 3-4 decade downward trend in

interest rates resulted in a 3-4 decade upward trend in housing

affordability for buyers using debt-based leverage (that is, for the vast

majority of buyers). There were corrections along the way, but provided

that long-term interest rates continued to make lower lows there would

eventually be a pool of new debt-financed buyers able to pay a much higher

price.

There's a good chance that the secular interest-rate trend

reversed from down to up during 2016-2018. If so, future house buyers that

don't have good timing and/or substantial area-specific knowledge

generally won't make long-term capital gains on their residential property

purchases.

A multi-week top

for the oil price?

In the latest Weekly Update we

wrote that 1) oil's initial rally from its December low probably will be

limited by resistance in the low-$50s and followed by a decline to test

the low, and 2) a larger and longer rally should get underway after the

December low is tested.

The following chart shows that there was a

positive momentum divergence at the December low and that the initial

rally from the low has reached resistance in the low-$50s. Also, note that

there is substantial resistance at $53-$55 that should limit the initial

rally if some additional headway is made over the days ahead.

There's a good chance that the next $5+ move in the oil price will be to

the downside, but there's also a good chance that oil will trade in the

$60s before the middle of this year.

The Stock Market

The US stock market's

valuation

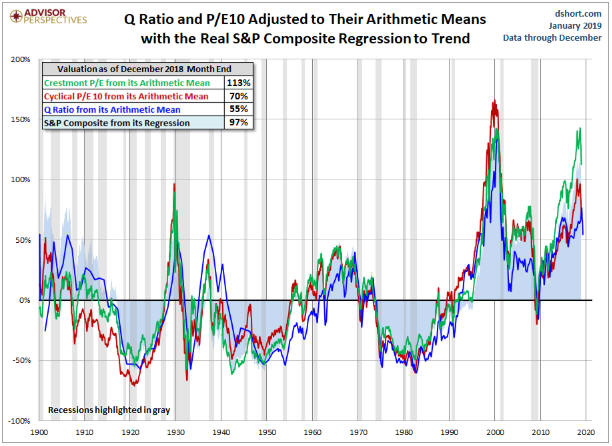

According to the four long-term valuation

measures shown on the following chart, at its 2018 high the S&P500 Index

was more expensive than at any time over the past 118 years with the

exception of 1999-2000 (the peak of the dot.com bubble). It was more

expensive than at the 1929 bubble peak and a lot more expensive than at

the major peaks of 1937, 1966 and 2007.

These long-term valuation

measures don't matter until a bear market gets underway, at which point

they indicate the magnitude of the downside risk over the ensuing 1-3

years. The current message is that IF (still a big if) a bear market began

last year then within the next two years the SPX will trade at least 50%

below last year's high, that is, at 1500 or lower. The reason is two-fold.

First, bear markets usually don't end until after the market becomes

under-valued. Second, the SPX would have to fall to around 1500 just to

get the long-term valuation measures down to their historical averages.

Chart source:

dshort

An argument can be made that the SPX was close to fair

value at last month's low, but only by assuming that earnings will grow at

a healthy pace over the next few years and that interest rates will remain

near their current depressed levels. These assumptions probably aren't

valid. This is partly because there's a high probability that the US

economy will enter a recession within the next 12 months, and if this

happens then 2020 corporate earnings will be much lower than 2018 or 2017

earnings. It's also because interest rates are probably now in long-term

upward trends.

Current Market Situation

In

the latest Weekly Update, we wrote: "The maximum levels that could be

reached prior to multi-week tops are 2600 for the SPX and 6600 for the

NDX. These levels are determined by the October lows."

We

should have written "should', not "could", because obviously it is

possible for the indices to trade higher. In any case, the following daily

charts show that the aforementioned maximums were reached on Wednesday 9th

January.

We have been expecting that the initial rally from the December low

would be followed by a decline to test the low and then a larger/longer

rally, regardless of whether we are dealing with a new bear market or an

intermediate-term bull-market correction. The attainment this week of

maximum target levels for the initial rally therefore should have set the

stage for tradable multi-week declines in the senior stock indices.

Although this remains the most likely outcome, something happened over the

past three days that muddied the waters. What happened was a surge in the

McClellan Oscillator (MO) for both the NYSE and the NASDAQ.

To

further explain, in the latest Weekly Update we wrote:

"The

NASDAQ's MO has risen to roughly the level that coincided with rebound

peaks in March and October of last year. This means that the market is

stretched to the upside on a short-term basis. However, if the MO were to

move significantly further into 'overbought' territory, say to 75 or

above, it would be a sign of strength rather than a warning of high

downside risk. This implies that the top of the initial rally should be

close IF -- as is reasonable to assume -- we are going to get a test of

the December lows prior to a more substantial rally."

Over the past

three trading days the MOs for both the NYSE and the NASDAQ moved

significantly further into 'overbought' territory -- to at or near 20-year

highs. A chart showing the NYSE Composite Index and the NYSE MO is

presented below. The signal is not infallible, but an MO surge of this

magnitude suggests the sort of internal strength that usually is followed

by only minor setbacks over the ensuing few weeks.

The odds still favour a test of the December low within the next two

months, but there is also a realistic chance that the next short-term

correction will do no more than retrace half of the initial rally from the

low.

New Option Positions

From the latest

Weekly Update:

"For TSI record purposes, a position will be

taken in the SPY (S&P500 ETF) 15th February-2019 $245 put option if it

trades at $3.60 this week. The option ended last week at around $4.00. For

the option to trade at our stipulated buy price the SPX would have to rise

to around 2550. Also, a position will be taken in the SPY 15th March-2019

$245 put option if it trades at $4.30 this week. The option ended last

week at around $6.00 and will only drop to our stipulated buy price this

week if the SPX rises to around 2600. We don't expect the SPX to get that

high before the start of the next meaningful decline, but a near-term rise

of that magnitude is not out of the question."

The

above-mentioned February put was added on Monday 7th January at $3.60 and

the above-mentioned March put was added on Wednesday 9th January at $4.16

(anyone with an outstanding order to buy at $4.30 would have been filled

at the open on Wednesday at $4.16).

Due to the MO surge discussed

above, we will be quick to exit the February put.

Gold and the Dollar

Gold

It's possible that last Friday's outside-down day marked a multi-week top

for the US$ gold price, but that hasn't been confirmed. A daily close

below the 20-day MA (the black line on the following chart) would be

preliminary evidence that such a top is in place. The 20-day MA is at

$1270 and is rising at the rate of $5-$10 per week.

A test of major

resistance in the $1360s is a realistic possibility for later this

quarter.

Gold Stocks

The Gold Miners ETF (GDX) is

slightly below the top of its rising short-term channel, which is where it

has been for about two weeks now. The channel top is at approximately

$21.70. Also, GDX is oscillating around lateral support/resistance at

$21.00, and the 200-day MA (near $20.60 at this time) has acted as support

during recent pullbacks.

In our most recent two commentaries we wrote that a pullback to

support and upward acceleration were equally-probable near-term outcomes.

That's still the case. Probably all it would take to get some upward

acceleration in the gold-mining sector is a couple of daily closes above

US$1300 in the bullion price.

As mentioned above, the 200-day MA

has been acting as support during pullbacks. Therefore, a daily close

below this MA (say, $20.50) would be evidence that a multi-week top is in

place.

Thanks to the choppy price action of the past three weeks,

the gold-mining sector (as represented by GDX) is not short-term

'overbought'. Be aware, though, that if it does become so via a sharp

up-move within the next several days then it will be vulnerable to

substantial weakness in the broad stock market. To put it another way, if

the gold-mining sector is 'overbought' near the start of the next sizable

decline in the broad stock market then gold stocks probably will go down

with most other stocks.

The Currency Market

The Dollar Index (DX) has finally broken below support at 95.75. This

validates our short-term target of 93.50. The associated target for the

euro is 1.18.

The fundamentals will determine whether the DX is

immersed in a short-term correction prior to a rise to new 12-month highs

or the first leg of an intermediate-term downward trend. Our

fundamentals-based model shifted from US$-bullish to neutral last week,

but from here it could quickly flip back to bullish or work its way into

bearish territory. If it does the latter then support at 93.5 will not act

as a floor for long.

Note that the DX must end this week below

95.75 to confirm the breakout. Also note that a daily close above 96 at

any time will suggest that the short-term downward trend is over.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

![]()