![]()

![]()

![]()

![]()

- Interim Update 9th August 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Oil Update

Recapping the bearish

oil supply situation

In the 17th May Interim Update we

wrote that the supply side of the supply-demand equation was now more

bearish for the oil market than for any other commodity market, the reason

being the ability and willingness of the US shale-oil industry to quickly

ramp-up supply in response to a higher price. Evidence in support of this

statement is provided by the market response over the past 18 months to

rising commodity prices.

On the one hand we have the zinc market,

where a strong upward trend in price has done almost nothing yet to

alleviate a tight supply situation. In fact, the supply situation in the

zinc market is more bullish today with the zinc price at around

US$1.30/pound than it was 18 months ago when the price of the metal was

around US$0.80/pound.

On the other hand we have the oil market,

where a strong upward trend in price during February-December of last year

prompted a large increase in drilling activity within the US shale-oil

industry, leading to a significant increase in production. Furthermore,

even though the oil price has drifted downward during the course of this

year it has clearly remained high enough to generate profits for many US

shale-oil-focused producers. We say this because during this year to date

the Baker Hughes Oil Rig Count (see chart below) has extended the steep

rise that began last year.

The rig count is still a long way below its average level of

2012-2014, but this is not a reason to be optimistic about the oil price.

The following chart of US daily oil production illustrates why. Notice

that even though the rig count is currently less than half its 2014-2015

peak, production has nearly returned to its 2014-2015 peak. Moreover,

there's a good chance that production will exceed its 2014-2015 peak

within the next 6 months regardless of what happens to the oil price.

Taken together, the two charts displayed above point to a very

impressive increase in productivity. Specifically, the charts indicate

that productivity per rig has roughly doubled over the past few years.

This is why oil drillers that needed an oil price of more than $70/barrel

a few years ago just to break even are now profitable at $45-$50/barrel.

For the reasons outlined above and in earlier commentaries, we suspect

that it will take an extraordinary event, such as a region-wide

conflagration in the Middle East, to get the oil price above $60/barrel

(in 2017 dollars) for more than a brief period. However, 3-12 month trends

in the oil price are driven to a greater extent by what's happening in

other markets, most notably the currency market, than what's happening to

oil supply. That's why we are expecting an intermediate-term rally in the

oil price from whatever low is made over the coming three months.

Oil's price action

The oil price made its most

recent bottom in June and has since rebounded as far as it can without

signaling an upward trend reversal. A daily close above $51 would be such

a signal.

We think that the oil price is close to a top that will

hold for at least a couple of months and that the next 10% move will be to

the downside. Also, there is still a risk of a decline to below $40 prior

to the start of the next intermediate-term rally, although the more likely

scenario is that the June low will turn out to be the low for the year.

The Stock Market

Close to the highest

valuation in history

From John Hussman's

latest Weekly

Comment:

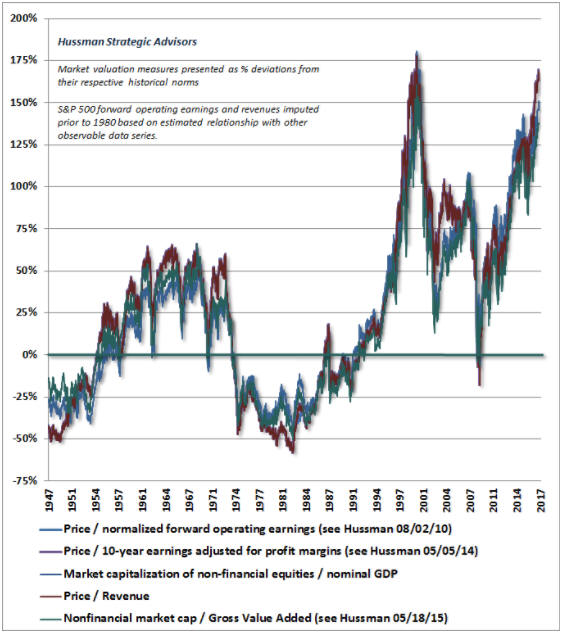

"The most reliable market valuation measures we

identify (those most strongly correlated with actual subsequent S&P 500

10-12 year total returns) now exceed every point in history except the

extreme reached in the single week of the final high March 24, 2000."

Valuation is an exceedingly blunt tool to use when trying to determine

what the stock market will do over the next several months, but a high

valuation creates downside risk and the highest valuation in history

suggests the scope for an unusually-large price decline. We hasten to

mention, though, that we are currently not betting that an unusually-large

price decline will soon get underway. What we are betting on is a decline

of at least 10% within the coming 2.5 months.

Putting some

numbers to the low volatility

With its 0.24% decline in

Tuesday 8th August, the SPX had gone 14 trading days without moving by

more than 0.30% in either direction. To put this into perspective, in data

going back to 1927 the previous record of consecutive daily moves of 0.30%

or less was ten. That's according to a Deutsche Bank analyst (Jim Reid).

Trump then came out with his crazy "fire and fury the likes of which

have never been seen" threat against North Korea, but even that wasn't

enough to bring about a daily move of more than 0.30% by the SPX. In fact,

the SPX ended Wednesday's session almost unchanged, increasing its

record-breaking sequence of trivial daily changes to 15.

The work of the same DB analyst tells us that as of 9th August the SPX

had gone 75 trading days without a daily gain of more than 1%. Over the

past 20 years the current run without a daily gain of at least 1% was only

exceeded between November-2006 and March-2007, when the SPX went 80 days

without such a daily gain.

The stock market is like a pendulum,

with periods of low volatility inevitably being followed by periods of

high volatility and periods of high volatility inevitably being followed

by periods of low volatility. The difference is that in the stock market

the swings from one extreme to the other don't occur at regular or

predictable intervals.

Interesting developments

Not much happened over the first three days of this week, but there

were two developments worth highlighting.

First, even though the

NASDAQ Composite Index reached its all-time high as recently as two weeks

ago and remains within 2% of its peak, on Wednesday 9th August there were

119 new 52-week lows by NASDAQ-traded stocks versus only 41 new 52-week

highs. As illustrated by the red bars on the lower section of the

following chart, the number of individual-stock new lows on 9th August was

the highest since the start of the post-election upward trend in

early-November of last year. This reflects internal weakness.

Second, the EURO STOXX 50 Index (STOX5E) has moved sideways since the

end of June, but reversed lower from its 50-day MA early this week and is

now precariously poised above short-term support. A breach of support at

3450 would likely be followed by a quick decline to around 3350.

Gold and the Dollar

Gold

The

US$ gold price gained $17 on Wednesday 9th August and managed to trade at

its highest level since early-June. Wednesday's price action didn't

significantly alter the chart pattern, though. To significantly alter the

chart pattern the gold price would have to close above resistance at

$1300. Also, Wednesday's price gain appears to have been a reaction to

Trump's "fire and fury" comment, which makes it suspect given that the

gold price never sustains gains that are driven by geopolitical conflict

or fear of same.

That being said, the fundamental backdrop was already gold-bullish

prior to Trump's latest threat to obliterate North Korea and regardless of

geopolitical issues will become increasingly so if economic confidence

declines over the weeks ahead. It is therefore possible that the US$ gold

price will soon break out to the upside. However, there is also a risk

that it will drop back to near the bottom of its 4-month trading range

before the next meaningful rally begins.

Note that for a breakout

in the gold price to be considered genuine/sustainable it would have to be

confirmed by a breakout in the gold-mining sector.

Gold

Stocks

In effect, the gold-mining sector has been coiling

since February. This is evidenced by GDX's well-defined contracting range.

As illustrated below, the price action over the first three days of this

week didn't change anything.

In addition to tracing out a form of 'coiling' pattern since its

February peak, GOEX, our preferred ETF proxy for the junior end of the

gold-mining universe, has also traced out a shorter-term coiling pattern

since mid-May. This pattern is the narrow rectangle drawn on the following

daily chart. A breakout would require a daily close above $23.00 or below

$21.20.

The question is: Will the coiling patterns end in upside or downside

breakouts?

With the fundamental backdrop currently being

gold-bullish and having the potential to move further into bullish

territory over the weeks ahead, we can make a reasonable case for an

upside breakout. However, we can also make a case for a 'deck-clearing'

plunge prior to the start of a tradable rally.

Fortunately,

there's no need to try to guess the answer to the above question because

prices won't have to move far from current levels to provide a conclusive

answer.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Exiting

Nevsun Resources (NSU)

Exiting

Nevsun Resources (NSU)

We added NSU to the TSI Stocks List

only two weeks ago with the idea that it would be a 3-9 month trade, but

the quarterly results published by the company after the close of trading

on Wednesday 9th August have prompted us to remove it.

There are

two main issues. First, the Bisha project is performing worse than

expected and could be a significant drain on the company's cash for at

least the next two quarters. Bisha accounts for about one-third of our NSU

valuation. Second, completion of the Timok project PFS has been delayed by

a few months -- from early in Q4-2017 to sometime in Q1-2018. Timok

accounts for the other two-thirds of our NSU valuation and the PFS was

expected to be a positive short-term catalyst.

NSU ended

Wednesday's session at US$2.62, which is roughly the price at which it was

added to the List two weeks ago. However, the price will fall on Thursday

in reaction to Wednesday's news. For TSI record purposes the exit price

will be adjusted to reflect where the stock trades on 10th August, as long

as it trades at US$2.40 or above.

We may return to NSU within the

next few months, as the Timok project has one of the world's best

undeveloped copper deposits and should eventually attract a premium

valuation.

A rank speculation on a gold discovery

A rank speculation on a gold discovery

Over the

past four weeks there has been crazy speculation in the shares of Novo

Resources (NVO.V). The stock was trading at around C$0.80 in early July

when it became apparent, initially via a Youtube video and subsequently

via an official press release, that the company had found gold nuggets in

primary conglomerates in the first trench at its 50%-owned Purdy's Reward

prospect in Karratha, Western Australia. In the 12th July press release

that confirmed this discovery the company advised that it had collected a

small bulk sample of these gold-bearing conglomerates for analytical test

work. Although the results of the bulk sample were positive it looks like

the 8th August press release that reported these results marked a

short-term top for the stock. On this day NVO traded as high as C$3.30. It

has since pulled back to C$2.83.

At C$2.83/share, NVO has a market cap of about C$340M. Considering the

very early stage of its exploration work at Purdy's Reward and its other

prospects in the northern part of Western Australia, this is an extremely

high valuation. With what's presently known about the company's assets,

near its current valuation we wouldn't touch NVO shares with a 10-foot

barge pole.

In effect, what happened over the past few weeks was

that stock speculators boosted NVO's market cap by about C$250M in

response to the company finding a few gold nuggets using a metal detector.

Now, there is obviously more gold in the area, but there would have to be

a LOT more to justify the current market cap and it would have to be

possible to economically extract the gold. Moreover, it will probably take

years and tens of millions of dollars of exploration work to define the

resource, assuming that a substantial resource even exists. In other

words, speculators in NVO shares got way ahead of the reality on the

ground, to put it mildly.

There is, however, a reasonable stock

speculation associated with this potential gold resource, just not

currently in NVO shares. The reasonable speculation is in the shares of

Artemis Resources (ARV.AX), the Australian company that owns the other 50%

of Purdy's Reward.

With 464M shares outstanding (including

in-the-money options that will soon be exercised) and a share price of

A$0.14, ARV is presently being valued by the stock market at about A$65M.

For this A$65M an investor gets 50% of the asset that resulted in the

recent frenzied speculation in NVO shares plus a few other

potentially-valuable assets including a gold processing plant and the

largest tenement package in Karratha. Some introductory information about

these assets can be found

HERE.

The following chart shows that, like NVO shares, ARV

shares were given a hefty boost by the recent speculation linked to

Purdy's Reward. However, the stock price has already pulled back sharply

from its high and, as mentioned, the market cap is MUCH smaller.

There are 68M ARV warrants with an exercise price of only A$0.02 that

expire at the end of next month. Trading associated with the exercising of

these warrants could create opportunities to buy ARV shares at lower

prices over the coming 1-2 months, but if you are interested in this

high-risk speculation then it would probably make sense to take an initial

position near the current price (A$0.14) with the aim of adding on

weakness.

We have added ARV to the TSI Small Stock Watch List.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://bigcharts.marketwatch.com/

http://www.investing.com/

![]()