![]()

![]()

![]()

![]()

- Interim Update 9th September 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

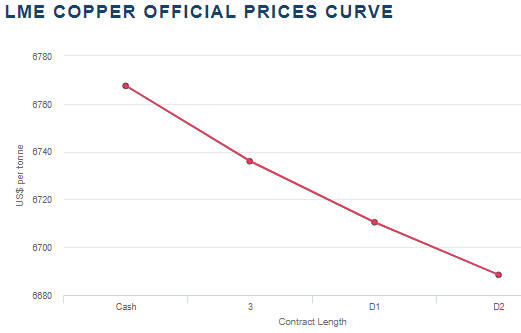

Copper in short supply

The total amount of copper

stored in LME warehouses has dropped to the lowest level in at least 15

years. To put the current LME copper inventory into perspective, it is

much less than a single week's copper consumption in China.

The reported LME warehouse inventories are subject to manipulation and

often do not reflect the overall supply situation in the metals markets.

In the current case of copper, however, the unusually low level of the

reported LME inventory does appear to be indicative of a commodity in

short supply. One reason is that the LME futures curve (see below) for

copper has a downward slope from the present through to December-2022 (D2

on the following chart). This means that the copper market is in

backwardation, which usually only happens when physical supply is tight.

Another reason is the ability of the copper price to hold near US$3.00

in the face of stock market weakness, general commodity market weakness

and US$ strength over the past several trading days.

The bullish supply-demand situation for physical copper won't prevent

a price correction, especially if there is a significant rebound in the

US$. However, it suggests to us that the short-term downside risk is less

than 10%.

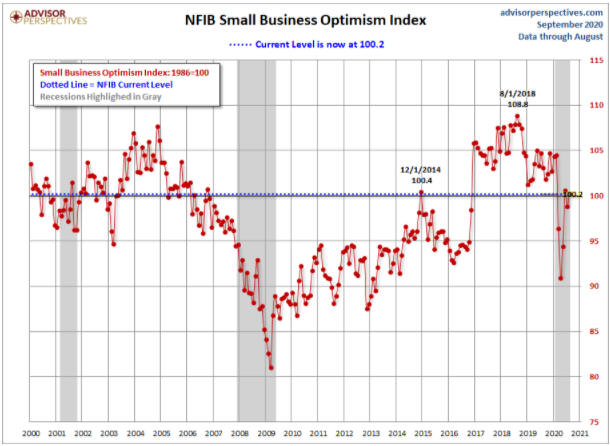

Survivorship bias

at work?

The following chart shows that

the National Federation of Independent Business (NFIB) Small Business

Optimism Index is close to its long-term average and higher than it was

throughout the economic expansion period of 2010-2016. Given the current

economic backdrop this doesn't make sense, but "survivorship bias" could

be distorting the picture.

Survivorship

bias is the logical error of concentrating on the people or things

that made it past some selection process and overlooking those that did

not, typically because of their lack of visibility. In this case, we think

that what's being overlooked is the large number of businesses that have

gone bust and therefore dropped out of the survey. For example, about 30%

of the restaurants in New York City have closed their doors permanently

since the lockdowns were imposed in March. A current survey of New York

restaurants would not include these establishments.

Source:

advisorperspectives.com

The Stock Market

More thoughts on the

Presidential Election Effect

In the 17th August Weekly

Update we wrote that beyond short-term reactions (a 'pop' in response to a

Trump victory and a plunge in response to a Biden victory), the outcome of

the US election scheduled for 3rd November might not matter as much as

most people believe. Regardless of who wins the political race in

early-November of this year, massive government spending and central bank

money-pumping probably will support the overall stock market, and

especially the cyclical sectors of the stock market, for 2-3 quarters

after the election. Also, regardless of the election result a major

stock-market downward trend probably will get underway by the middle of

next year.

Our view hasn't changed, although in our earlier

discussion we didn't mention the biggest election-related threat to the

stock market. Our earlier discussion was predicated on the assumption that

a winner would be known within days of the election taking place, but

there is a risk that it will be weeks or even months after election day

before one side or the other concedes defeat. For the stock market, this

would be the worst-case scenario for two reasons. First, it would prolong

the uncertainty and prevent many investors from attempting to discount

future government policy, leading to reduced market liquidity and larger

weekly price swings. Second, it could delay the spending programs that

both parties are planning for 2021.

The situation could look very

different by the time November rolls around, but based on what we know

today we think it will make sense to be positioned defensively (meaning:

not aggressively long or short) going into the US election and to remain

defensive until the result is clear.

Vaccine news and the

biotech sector

News hit the wires on Tuesday that the

AstraZeneca/Oxford phase 3 COVID-19 vaccine trial had been put on hold due

to an unexplained serious illness (subsequently reported as being

Transverse Myelitis) in one of the trial participants. Other vaccine

trials are on-going, but the AstraZeneca/Oxford vaccine had been described

by the World Health Organization as the world's leading candidate.

The issue encountered in the AstraZeneca/Oxford vaccine trial is

significant not only because it will delay one potential vaccine, but also

because it will reduce the public's confidence in whatever vaccine makes

it through the approval process. We suspect that the majority of people

will be unwilling to take the first generation of any government-approved

vaccine, so in most parts of the world it will be a long time before there

is "herd immunity".

Given the widespread fear regarding the

coronavirus and the massive resources that have been channelled into the

development of vaccines and treatments for the virus, it isn't surprising

that the biotech sector of the stock market was a relative strength leader

between mid-March and mid-July. What is perhaps a little surprising is

that the biotech sector, as represented on the following daily chart by

BBH, appears to have made an intermediate-term top in mid-July and is now

testing its lows of the past 4 months. This probably reflects the reality

that most biotech and pharmaceutical companies will not make money from

the coronavirus and that the overarching focus on this virus has detracted

from work on other medical/health issues.

We don't pay much

attention to the biotech sector and have no opinion regarding its

short-term or intermediate-term prospects. We do note, though, that BBH

has major support in the $140s and short-term resistance in the $160s.

This suggests to us that the $160s is a likely area for a short-term

rebound to end and that the $140s is a likely area for the

intermediate-term correction to end.

Current Market Situation

In the US stock

market, the sell-off that began last Thursday continued on Tuesday of this

week (the first trading day of the holiday-shortened week). This enabled

the SPX and the NDX to close below last week's low on Tuesday and for the

NDX to reach is 50-day MA.

This is the first time the NDX has

traded at its 50-day MA since April, with all previous pullbacks over the

past 4.5 months having ended near the 20-day MA. Consequently, for the NDX

this is already the most significant correction since the March low.

The oil sector of the stock market held up well in the face of

weakness in both the SPX and the oil price late last week, but it took a

hit on Tuesday of this week. Tuesday's plunge was caused by the government

of Saudi Arabia announcing a cut in the price of its exported oil at a

time when the oil market was technically vulnerable. However, other

cyclical sectors of the stock market have continued to show the same

resilience that was evident during last week's general market sell-off.

For example, the following chart shows that the Dow Transportation Average

(TRAN) remains close to its high for the year.

Also worth mentioning is that the Volatility Index (VIX) did not

exceed last week's high during Tuesday's selling squall and has dropped

back to the high 20s. As a result, last week's volatility spike looks

similar to the June volatility spike.

Tuesday's closes below last week's lows by both the SPX and the NDX

warn that a 10%+ correction could be underway for these indices, but after

underperforming for a couple of months the overall market now looks

stronger than the mega-cap tech stocks that dominate the NDX and to a

lesser extent the SPX.

Gold and the Dollar

Gold and Silver

The US$ gold price continues to test support near $1920 without

closing below it. On each of the past two trading days it traded at/below

this support and then rebounded, with Wednesday's rebound being capped by

the 20-day MA. This means that it is showing some resilience, but not

showing any real strength.

The upshot is that the following comment

from the latest Weekly Update remains applicable:

"A solid

break below US$1920 probably would pave the way for a correction low

during October, but until support is breached there will be a realistic

chance that the price action since early August was a mid-trend

consolidation rather than a topping pattern."

Like gold, silver is showing resilience but not much strength. It

managed to hold above short-term lateral support at US$26.00 over the past

two trading days while being capped by its 20-day MA.

A rebound

within the context of a developing top could take the price up to the

$28-$29 range over the days ahead, while a daily close below $26.00 would

signal that a decline to below the August low and possibly as low as the

200-day MA had begun.

Gold Stocks

In the latest Weekly Update, we

wrote:

"The HUI's price action since its early-August high

currently looks more like a mid-trend consolidation -- similar to what

happened between mid-May and mid-June -- than a topping pattern. However,

the strong tendency for the HUI to set a multi-quarter extreme between

early-August and early-September is a cause for concern. The

August-September cycle warns that the next 15%+ move will be to the

downside.

A new high for the year within the next few days still

would be consistent with the August-September cycle, but a new high for

the year after this week would indicate that the August-September cycle

did not work this year and that the intermediate-term upward trend had

resumed. A daily close below 320 would validate the August-September cycle

and indicate that a decline to an October-November low was underway."

Due to what happened over the past two trading days the HUI's price

action now looks even more like a mid-trend consolidation. As illustrated

by the following daily chart, the HUI traded slightly below its 50-day MA

on Tuesday and then reversed course. It ended Tuesday above this MA and

then gained enough ground on Wednesday to close above its 20-day MA.

The HUI has now spent about four weeks inside its early-August range.

During this period it made a sequence of slightly-lower highs and

slightly-higher lows, a coiling pattern that is more often associated with

a mid-trend consolidation than a top.

We are still in the

time-window for a multi-month high, but that window will close this week.

A new high for the year after this week will suggest that the

intermediate-term upward trend has resumed. If that happens we probably

will remove most of our hedges.

Note that the short-term chart patterns of the gold mining

indices/ETFs are more bullish than the short-term chart patterns of gold

and silver bullion. One way or the other the charts should move into line

with each other within the next couple of weeks, either by the metals

following the equities higher or the equities following the metals lower.

The Currency Market

The following daily chart

shows that over the past month the Dollar Index (DX) moved from the bottom

to the top of its short-term downward-sloping channel essentially by going

sideways. Needless to say, to date the rebound has been unimpressive.

A stronger rebound -- within the context of a longer-term decline that

should extend well into next year -- is expected and would be signalled by

a daily close above 94. The 94 level looks significant because a daily

close above it would break the DX above short-term lateral resistance, the

short-term channel and, if it happened after this week, the 50-day MA.

A break above 94 would suggest short-term upside targets of 95.5-96.0

and 97.5-98.0. The DX should make it to the former and could make it to

the latter of these target ranges before resuming its longer-term decline.

However, as things stand right now there is a risk that the DX will

make a new low for the year before commencing a meaningful rebound. This

could happen due to US election-related uncertainty and/or a further

near-term rise in US inflation expectations.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() The

Enable Midstream Partners (ENBL) trading position closed

below our 20% trailing stop loss on Tuesday 8th September and has been

removed from the TSI List. The result of the trade was a profit of 11%.

The

Enable Midstream Partners (ENBL) trading position closed

below our 20% trailing stop loss on Tuesday 8th September and has been

removed from the TSI List. The result of the trade was a profit of 11%.

We remain optimistic about the intermediate-term prospects of this

natural gas distributer and will look for a new opportunity to 'go long'.

New Century Resources (NCZ.AX), a mid-tier Australian

zinc producer, was added to the TSI List as a trading position in the 8th

June Weekly Update to provide leveraged exposure to zinc and also

potentially to provide leveraged exposure to nickel. The exposure to

nickel required the completion of a deal that involved NCZ acquiring the

Goro nickel mine in New Caledonia from Vale.

New Century Resources (NCZ.AX), a mid-tier Australian

zinc producer, was added to the TSI List as a trading position in the 8th

June Weekly Update to provide leveraged exposure to zinc and also

potentially to provide leveraged exposure to nickel. The exposure to

nickel required the completion of a deal that involved NCZ acquiring the

Goro nickel mine in New Caledonia from Vale.

On Tuesday of this

week NCZ advised that it has decided not to proceed with the Goro

acquisition. In our opinion, this news leaves the stock's risk/reward

unchanged.

As explained in our 8th June write-up:

"We

like NCZ with or without the Goro deal. Without the Goro deal it has good

upside potential (100%-200% within the next 12 months, assuming a rebound

in the zinc price to above US$1.10/pound) and only moderate risk. With the

GORO deal it has much greater upside potential in exchange for much higher

risk."

NCZ is now a pure play on zinc, which is fine. However,

it means that we are now on the lookout for a nickel play for the TSI

List. One possibility is Clean TeQ (ASX and TSX: CLQ), a former TSI stock

selection that provides exposure to cobalt and platinum in addition to

nickel.

CLQ's

Sunrise project in NSW is marginal at current metal prices and the

stock is not particularly cheap (with 746M shares outstanding, at the

current price of A$0.30/share the market cap is about A$220M), but the

company is chaired by Robert Friedland and therefore stands a good chance

of being aggressively promoted under the right market conditions.

Along with many other commodity-related equities CLQ appears to have made

a major bottom in March-2020. It has traced out an intermediate-term

basing pattern, but during the first half of this week it became

short-term 'overbought' due to rapid price rise. It is now in the process

of 'correcting' this rapid rise.

In a recent press release CLQ advised: "...[the company] will

release the final outcomes for its Project Execution Plan (PEP) at the end

of September 2020, including a full economic evaluation of the [Sunrise]

Project. It will incorporate the latest engineering and design work based

on updated material quantities, vendor pricing and labour costs."

Therefore, within the next three weeks we should get some useful

information regarding CLQ's value and potential.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://www.lme.com/

https://www.kitco.com/

http://bigcharts.marketwatch.com/

![]()