![]()

![]()

![]()

![]()

- Interim Update 10th May 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

What is a bull market?

A reasonable definition of a

bull market must be practical. This means that it must take into account

the fact that what people really want from an investment is an increase in

purchasing power, not just an increase in price. Figuring out whether or

not an investment is in a bull market is therefore not as straightforward

as observing its long-term trend in nominal currency terms.

Here's

a great example of why looking only at nominal price change doesn't

necessarily indicate whether or not something is in a bull market: Ten

years ago, the price of everything in the world was in a powerful upward

trend when price was expressed in terms of the Zimbabwe dollar. Obviously,

it was far more reasonable in this case to say that the Zimbabwe dollar

was in a bear market than to say that everything else was in a bull

market.

The Zimbabwe example is extreme, but the fact is that all

of today's official currencies are losing purchasing power (PP). They are

losing PP at different rates and some are losing PP quite slowly at the

present time, but not one of them is likely to be a good measuring stick

over a long period.

Unfortunately, determining whether or not an

investment is gaining value in real terms is problematic due to the

impossibility of coming up with a single number that reflects the

economy-wide PP of money. We have a method of adjusting for the effects of

monetary inflation that should be 'in the right ballpark' over periods of

more than 5 years, but our method could be wildly inaccurate over periods

of less than 2 years. Inflation-adjusting using the official CPI, on the

other hand, is likely to be inaccurate over all periods and wildly

inaccurate over the long-term.

In a world where the official

currencies make poor measuring sticks due to their relentless and variable

depreciation, looking at the relative performances of different

investments is probably the best way to determine which ones are in bull

markets. Furthermore, because they are effectively at opposite ends of an

investment seesaw, with one doing best when confidence in money, central

banking and government is rising and the other doing best when confidence

in money, central banking and government is falling, this is a concept

that works especially well for gold bullion and the S&P500 Index (SPX).

There will be times when both gold and the SPX are rising in US$

terms, but it will always be possible to tell the one that is in a genuine

bull market because it will be the one that is the stronger. More

specifically, if the SPX/gold ratio is in a multi-year upward trend then

the SPX is in a bull market and gold is not, whereas if the SPX/gold ratio

is in a multi-year downward trend then gold is in a bull market and the

SPX is not. There will naturally be periods of a year or longer when it

will be impossible to determine whether a multi-year trend has reversed or

is consolidating (we are now in the midst of such a period), but, as

discussed last week, there is a moving-average crossover that can be used

to confirm a reversal in timely fashion.

In conclusion, it is

reasonable to say that an investment is in a bull market if it is in a

multi-year upward trend in nominal currency terms AND relative to its main

competition.

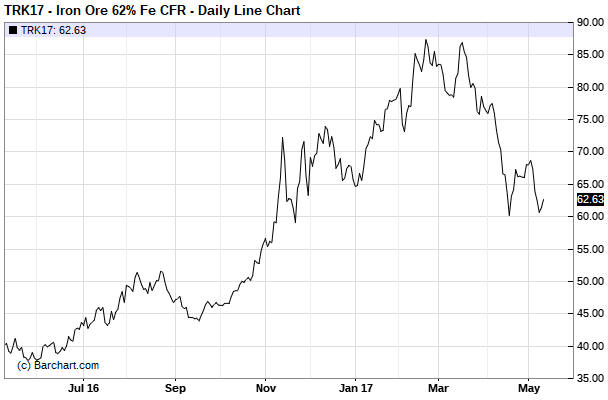

Iron-Ore

In the world of industrial

commodities, the iron-ore market led the way higher from a January-2016

low and then confirmed an intermediate-term downward reversal when it

broke below $80/tonne in March of this year.

Due to its leadership,

over the past year we have paid more attention to iron-ore than we

normally would. We will continue to do so, because at some point over the

next few months it could provide timely confirmation of an

intermediate-term reversal to the upside.

As illustrated below, the

iron-ore price has found some support near $60. However, it would need to

get back above $75 on a weekly closing basis to suggest that the bottom

was in.

The Stock Market

The following daily chart shows

the SPX and the Volatility Index (VIX).

During the second half of

April the SPX quickly rose from near a 2-month low to near its 1st March

all-time high. It has since hovered near its all-time high, not showing

any signs of weakness but also not managing to break out to the upside.

This lack of volatility with the price near an all-time high has pushed

the VIX down to a 20-year low.

With the VIX at such a low level it is tempting to buy VIX call

options. At least, it would be if the options weren't so expensive.

VIX call options with a few months to expiry often seem expensive

because they are based on VIX futures prices rather than on the index

itself. For example, even though the VIX ended the 10th May session at

only 10.2, the October-2017 VIX futures contract ended the same session at

15.6. Consequently, if you were to buy October-2017 VIX calls right now

you would be buying calls that are priced on the basis of an underlying

index value of 15.6.

The large premium to the spot index at which

VIX futures contracts usually trade is the reason you will lose money

buying a volatility ETF/ETN such as VXX unless you get the timing exactly

right. These ETFs/ETNs are regularly rolling from relatively low-priced

nearer-dated contracts into relatively high-priced later-dated contracts,

leaking value as they go.

The stock market is currently a high-risk

proposition, but it is not going to 'fall out of bed' with no warning.

Ideally, a warning will come in the form of a failed upside breakout (a

surge into new-high territory that is quickly reversed), as this would

create a relatively low-risk setup for a bearish speculation.

Alternatively, any decline that takes out the SPX's March low would be a

clear-cut warning.

Gold and the Dollar

Gold

Based on the daily RSI(14), on Tuesday of this week the gold market became

short-term 'oversold' for the first time this year. However, while there

is some support in the $1215-$1220 range, the price could still drop to

lateral support in the $1190s before a 1-3 week counter-trend rebound gets

underway.

Assuming that an interim low is either already in place

or will soon be put in place via a spike down to the $1190s, the

$1245-$1255 range is a likely place for a rebound peak.

Silver

The silver extreme became even more so

over the first two days of this week. In particular, by the close of

trading on Tuesday 9th May silver's daily RSI(14) was near a 20-year low

of only 17.4 and the price had fallen on 15 of the latest 16 trading days.

The relentlessness of the decline was made possible by the price

having reversed course after speculators had built up a record-high

net-long position in silver futures. We will therefore be more interested

than usual to see the COT data at the end of this week. The data will show

the positioning at the close of Tuesday's trading session and will

therefore reveal the extent to which speculators in the futures market

liquidated their collective long exposure in response to the price

weakness.

Based on what happened in the past following similar short-term

momentum extremes (as indicated by the daily RSI), this week's low will

NOT be the final low but it will hold for a few weeks. Here's the sequence

that we can reasonably expect:

1) A rebound from this week's low

that lasts about 2 weeks and reaches the 20-day MA (the black line on the

above chart) or a little higher. The rebound target range noted in the

latest Weekly Update ($17.00-$17.50) is still applicable.

2) A

decline that takes the price either slightly below the May low or well

below the May low. Whether it's slightly below or well below will mostly

be determined by the extent to which the speculative net-long position has

been reduced and what's happening in the gold market at the time the May

low is breached.

3) A tradable multi-month rally.

Gold Stocks

The HUI successfully tested support at 180

last week and is now rebounding. The 50-day MA near 196 or a few points

higher is the most likely area for a rebound peak, although a

counter-trend rebound could possibly go as high as the 200-day MA near

210.

We expect that this rebound will be followed by a decline to

new lows for the year, with the likely time-window for an

intermediate-term bottom having narrowed from May-July to June-July due to

the absence of a capitulation over the past week.

Due to the liquidity problems recently experienced by GDXJ and the

resulting decision of the ETF's manager to shift the fund's focus towards

mid-tier gold-mining companies, from now on we will use the Global X Gold

Explorers ETF (GOEX) as our main proxy for the junior end of the

gold-mining sector.

Even though GOEX broke below support defined by

its March low last week, it is likely that a multi-week low is in place. A

rebound to near the 50-day MA ($23) would be normal.

The Currency Market

The Dollar Index

Macron predictably won the French

Presidency on Sunday 7th May and the market reaction was minor. This

supposedly euro-bullish political outcome resulted in only a small upward

spike in the euro and downward spike in the Dollar Index on Monday, no

doubt because the polls had all but ruled out any other outcome well

before 7th May. However, it did cause both the euro and the Dollar Index

to make marginal new extremes for the year before reversals occurred.

This week's reversal increases the probability that May-2017 will be

the fourth in a series of important May lows for the Dollar Index (the

Dollar Index made a multi-month or multi-quarter low in May-2014, May-2015

and May-2016).

Needless to say, Monday's intra-day low is now a

very significant support level. Going the other way, there is trend-line

resistance slightly above 100 and more important resistance defined by the

April high at 101.3. It would take a daily close above 101.3 to remove

most of the remaining doubt that a multi-month low is in place.

The Canadian Dollar (C$)

A

reversal over the past few days has signaled an interim low and the start

of what will probably turn out to be a 2-3 week rebound for the C$. A

routine rebound would take the C$ up to around 74 to test its previous

downside breakout, after which the longer-term decline would resume.

As noted in an earlier commentary, the short-term technical objective

is 71.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.barchart.com/

![]()