![]()

![]()

![]()

![]()

- Interim Update 11th July 2018

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The copper unwinding

Four weeks ago, speculators in

Comex copper futures collectively held their largest net-long position in

history. When the copper price began to decline this massive speculative

bet started being unwound, which exacerbated the price weakness and

prompted more speculative selling. In other words, due to the immense size

of the speculative net-long position the price decline temporarily became

self-reinforcing. By last Tuesday (the date of the latest COT data) the

speculative net-long position on the Comex had dropped to near an 11-month

low, meaning that bullish speculators in Comex futures no longer posed a

substantial threat. However, the Financial Times article posted

HERE points out that another threat was lurking in the background.

The other threat was a large speculative net-long position in copper

futures on the Shanghai Exchange. It seems that about three-quarters of

this Chinese position was rapidly sold after the copper price had been

driven down to the mid-$2.90s by the liquidation of speculative long

positions on the Comex. This explains the 3-day plunge from seemingly

strong support at around $2.95 to last Friday's low of $2.78.

Here's an excerpt from the above-linked article:

"The

liquidation of a $1bn bet placed by a Chinese investor has roiled the

copper market, triggering a violent sell-off that has seen the metal

plunge to a 12-month low.

Data released by the Shanghai Futures

Exchange showed the huge futures position held at Gelin Dahua, a

Beijing-based brokerage, had fallen from a net long of 36,050 lots last

Wednesday to only about 10,000 lots yesterday.

That is the

equivalent of 130,000 tonnes of copper, worth roughly $800m, being

liquidated over the past four trading sessions.

Since last August,

Gelin has been the dominant buyer of copper, stepping into the market to

buy metal whenever the price weakened, according to Nicholas Snowdon,

analyst at Deutsche Bank. "There was in other words a perceived Gelin put

in the copper market in the first half of 2018," said Mr Snowdon. "This

now appears to be dissipating fast.""

Given copper's

performance after the close of this Tuesday's Comex trading session, with

the price plunging from a Tuesday close of $2.84 to as low as $2.72 during

Asian trading on Wednesday, it's likely that the balance of the

speculative Chinese position discussed in the above-linked article has

been liquidated. This could mean that the path is now clear for the

rebound to the mid-$2.90s mentioned in the latest Weekly Update, although

an important support level was breached during the

late-Tuesday/early-Wednesday sell-off and there was no recovery later on

Wednesday.

The copper market is now extremely 'oversold' on a short-term basis,

but it is in the midst of a self-reinforcing decline driven by emotion and

could fall further over the days ahead. Support near $2.50 remains the

most likely place for a sustainable low, with or without an intervening

rebound.

No currency

manipulation by China's government, yet

In the 2nd July Weekly Update we

discussed the risk posed by the recent weakening of China's currency (the

Yuan), and commented: "We won't know for sure until China's central

bank publishes its international currency reserve figure for June, but the

recent weakening of the Yuan does not appear to be the result of a

deliberate move by China's government." We now know for sure -- the

Yuan's pronounced weakness during the month of June was NOT the result of

government manipulation. In fact, it can be more aptly described as the

result of an absence of manipulation.

We know that this is so

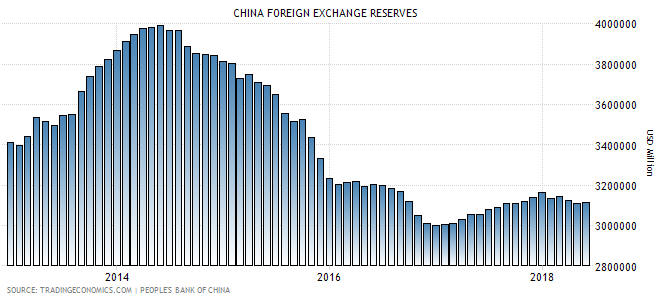

because of what happened to China's currency reserves in June. As

indicated by the final column on the following chart, almost nothing

happened (there was no significant change). This means that China's

government made no attempt to either strengthen or weaken its currency

last month.

To further explain, for China's government to engineer weakness in the

Yuan's foreign exchange value it must add to its international currency

reserves by exchanging its own currency (that it creates 'out of thin

air') for foreign currency. By the same token, for China's government to

increase the Yuan's relative value it must use its international currency

reserves to purchase Yuan. Consequently, periods when China's currency

reserve is increasing are periods when China's government is attempting to

weaken the Yuan and periods when China's currency reserve is decreasing

are periods when China's government is attempting to strengthen the Yuan.

The above chart therefore tells us that China's government was

trying to weaken the Yuan up to mid-2014 and strengthen the Yuan from

mid-2014 until the end of 2016. The chart also seems to indicate that

there was a tentative attempt to weaken the Yuan during 2017, but 2017's

gradual increase in China's foreign currency stash was most likely driven

by changing market valuation. We are referring to the fact that because

reserves are reported in US dollars and held as debt securities, the

reported value of the reserves can be altered by a change in exchange

rates or bond prices. In particular, the reported reserve figure will have

an upward bias during periods when the US$ is weak relative to other major

currencies, as it was throughout 2017.

The bottom line is that

China's government has not yet weaponised the Yuan's FX value in its

economic war with the US government, but it is also not standing in the

way when the Yuan weakens in response to market forces.

The Stock Market

Further escalation in

the "trade war"

It was announced after the close of US

trading on Tuesday 10th July that the US government is ploughing ahead

with tariffs on an additional $200B of Chinese goods. This latest batch of

US tariffs is in retaliation to tariffs on US goods imposed by the Chinese

government in retaliation to the $34B of US tariffs that came into effect

at the end of last week. This would be funny if the economic consequences

weren't so seriously negative.

Chinese exports to the US amount to

about $500B per year whereas US exports to China amount to only about

$130B per year. Therefore, China's government cannot keep retaliating in

kind against US tariffs on a dollar for dollar basis. However, the sum of

US exports to China and local sales in China by US companies happens to be

about $500B per year, so China's government potentially could retaliate

dollar for dollar by making life more difficult and costly for US-owned

companies operating in China.

Strangely, the stock market doesn't

seem to care. Some industrial and agricultural commodity markets have

reacted in dramatically-negative fashion to the escalating economic war

between governments, but the US stock market has been acting as if it were

a safe haven. This can't last, especially in light of the relatively tight

monetary backdrop.

Current Market Situation

With regard to the long-term price prospects for equities and

commodities, the "trade war" is not close to being the biggest issue. Even

if it continues to escalate it will not be the biggest issue, despite the

fact that it will materially reduce economic progress and living

standards. The biggest issue is the damage that has been inflicted over

the past several years by central bank manipulation of interest rates and

money. Mal-investment stemming from monetary manipulation will be the root

cause of the next recession and/or financial-market crisis, but the "trade

war" could be the catalyst for a stock market reversal of at least

intermediate-term importance.

Up until now, investor/speculator

fear related to the "trade war" has been confined to a few commodity

markets and some peripheral stock markets. Prior to Wednesday of this week

the oil market was unscathed (the oil price dropped 5% on Wednesday) and

so were some of the most important US stock indices.

Among the

high-profile US stock indices, the Russell2000 SmallCap Index (RUT) and

the NASDAQ100 Index (NDX) have been the strongest. Investors (using the

term as loosely as possible) have been buying the stocks and ETFs

associated with these indices as if they were immune to the economic

weakness that would stem from the continuation of the international trade

conflict, seemingly oblivious to the reality that these stocks are, on

average, priced for perfection.

The aforementioned indices were

expected to make marginal new highs before reversing course. As

illustrated below, the RUT made a marginal new high and the NDX tested its

high on Tuesday before pulling back.

It is yet to be seen whether the pullbacks of the past two trading

days were meaningful reversals. However, the fact that pullbacks have

occurred following tests of the highs means that the risk associated with

new bearish speculations can be managed by placing stops slightly above

Tuesday's highs. For example, Tuesday's high for the NDX was 7298 and the

June high (the all-time high) was 7310, so it would be reasonable to buy

QID (UltraShort QQQ) now and risk a daily NDX close above, say, 7320. For

another example, Tuesday's all-time high for the RUT was 1709, so it would

be reasonable to buy TWM (UltraShort Russell2000) now and risk a daily RUT

close above, say, 1720.

Alternatively, speculators who are willing

to accept the risk of a larger loss in exchange for reducing the

probability of being 'whipsawed' could take a position in a leveraged

inverse ETF now and initially risk a WEEKLY close above this week's

intra-day high.

Protective stops can't be used effectively with

out-of-the-money options, though. With such options the risk management

must happen at the time of purchase, in that the amount of money put at

risk should be small enough that a total write-off would be easy to

handle.

Today we are adding a bearish option speculation to the TSI

List. The option is associated with IWM, an ETF that tracks the RUT.

Specifically, we are adding the IWM September-2018 $150 put option at

US$0.76, which is near the mid-point of Wednesday's closing bid-ask spread

(US$0.74-$0.77). This option is about 10% out of the money.

Gold and the Dollar

Gold and Silver

In the latest Weekly Update, we wrote:

"...last week the

US$ gold price spiked down to its December-2017 bottom and then rebounded

to end the week with a net gain of about one dollar. It's possible that

last week's downward spike to the December-2017 bottom will be the low for

the year, but that possibility is a long way from being confirmed. At this

stage all we have is a test of support followed by a minor rebound.

A typical counter-trend rebound would end below $1280, so to indicate

that a multi-month bottom is in place the price must achieve a solid break

above $1280. Failing to do so would keep alive the possibility that the

decline from the April high ($1370) is not complete."

This

week the US$ gold price didn't come close to breaking above $1280.

Instead, it spiked up to the high-$1260s on Monday and then reversed

course. It is now re-testing the December-2017 bottom.

If the

December-2017 bottom ($1238.30) is breached on a daily-closing basis then

a decline to the next area of strong support, which means a decline to the

$1200-$1215 range, will become likely. A decline of that magnitude within

the coming week or two potentially would turn the sentiment situation from

moderately supportive to very supportive and -- as long as the fundamental

backdrop remained gold-bullish -- set the stage for an intermediate-term

advance.

Regarding silver, in the latest Weekly Update we wrote:

"A

daily close above $16.30 would be a preliminary sign that the price has

turned upward on a sustainable basis, but to signal conclusively that a

meaningful rally is underway the market will have to end the pattern of

declining tops that is now almost 2 years old. To do so the silver price

will have to close above $17.30."

Over the first three days of

this week the silver market didn't even come close to generating a

preliminary sign that the price has turned upward on a sustainable basis.

Instead, the highest daily close was $16.14 on Monday 9th July, after

which there was a quick return to the early-July low. At the moment the

path of least resistance appears to be down.

If the early-July low

is breached then a test of the December-2017 low near $15.60 likely will

follow in short order. A decline to the December-2017 low or lower may be

required to finally establish a bullish sentiment backdrop in this market.

Gold Stocks

The Gold Miners ETF (GDX) ended

last week above its 50-day and 200-day MAs and near the top of its narrow

3-month price channel. As illustrated by the following daily chart it

spiked above its channel top on Monday of this week, but failed to close

above it. On Wednesday it plunged below its 50-day and 200-day MAs while

remaining within its narrow channel.

Wednesday's decline in the GDX price looks impressive on the above

chart, but that's only because the chart zooms in on a period of

unusually-low volatility. It takes a move of only 4% to get the price from

channel top to channel bottom or vice versa. Consequently, we are yet to

see the anticipated increase in volatility in the gold-mining sector.

As mentioned in a recent TSI commentary, we have a nagging concern

that there hasn't been a sharp decline or capitulation in the gold-mining

sector that 'clears the deck'. A capitulation is not a prerequisite for a

multi-month rally, but the fact that it hasn't happened creates the risk

that it is yet to come.

The Currency Market

The Dollar Index (DX) bounced off its 50-day MA early this week, but

this hasn't changed our expectation that it will drop to around 92 within

the next 2 months.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

https://tradingeconomics.com/

![]()