![]()

![]()

![]()

![]()

- Interim Update 11th October 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Why a euro collapse

will precede a US$ collapse

There are three critical

differences between the monetary systems of the US and the euro-zone and

these differences make it inevitable that the euro will collapse (cease

being a useful medium of exchange) before the US$ collapses.

The

first difference is to do with the euro-zone system being an attempt to

impose common monetary policy across economically and politically

disparate countries. This is a problem. A central planning agency imposing

monetary policy within a single country is bad enough because it generates

false price signals and in so doing reduces the rate of economic progress.

However, when monetary policy (the combination of interest-rate and

money-supply manipulations) is implemented across several

economically-diverse countries the resulting imbalances grow and become

troublesome more quickly.

As an aside, money is supposed to be

neutral -- a medium of exchange and a yardstick, not a tool for economic

manipulation. Therefore, it is inherently no more problematic for

different countries to use a common currency than it is for different

countries to use common measures of length or weight. On the contrary, a

common currency makes international trading and investing more efficient.

For example, there were long periods in the past when gold was used

simultaneously and successfully as money by many different countries.

However, if a currency can be created out of nothing then there is no

getting around the requirement to have an institution that

oversees/manages it. The euro could therefore not be 'fixed' by simply

eliminating the ECB. The ECB and the one-size-fits-all monetary policy it

imposes are indispensable parts of the euro-zone system.

The second

difference is linked to the concept that a government with a captive

central bank cannot become insolvent with respect to obligations in its

own currency. For example, due to the existence of the Fed the US

government will always have access to as much money as it needs to meet

its obligations, regardless of how much debt it racks up. Putting it

another way, should all other demand for Treasury debt disappear the Fed

will still be there to monetise whatever amount of debt the US government

issues. Consequently, the US government will never be forced to directly

default on its debt.

It's a different story in the euro-zone,

however, because the ECB is not beholden to any one government. The

provision of ECB financial support to one euro-zone government therefore

requires the acquiescence of other governments. This hasn't been a

stumbling block to date and the ECB has provided whatever support was

needed to prevent financially-stressed euro-zone governments from directly

defaulting on their debts, but eventually a point will be reached when the

governments of some countries balk at their interest rates and money being

distorted as part of an effort to prop-up the finances of another

government. At that point there will either be direct default on euro-zone

government debt or the disintegration of the monetary union.

Once

it becomes clear that direct default on government debt is a risk to be

reckoned with, 'capital' will flee the euro-zone at a rapid rate. This is

because the main (only?) reason to own government bonds is that they are

supposedly risk free.

The third critical difference between the US

and euro-zone monetary systems is similar to the second difference. In the

US there is a symbiotic relationship between the Fed and the government,

with one institution always being prepared to support the other in a time

of crisis. One consequence of this relationship is the virtual

impossibility -- as discussed above -- of the US government ever being

forced to directly default on its debt. Another consequence is the virtual

impossibility of the Fed ever becoming bankrupt.

Several years ago

there was much speculation that the Fed would go broke due to large losses

on the bonds it was buying in its QE operations, but this speculation was

never well-informed. Up until now the Fed has made out like the bandit it

is on its 'investments' in Treasury and mortgage-backed securities, but

even if these securities had collapsed in value it would not have resulted

in the Fed going bust. It would simply have led to a line being added to

the Fed's balance sheet to keep the books in balance.

Again,

though, it's a different story in the euro-zone. Should the ECB begin to

incur large losses on its bond portfolio there is no certainty that it

would be able to keep going about its business as usual. To do so would

require the support of governments/countries that never benefited from and

never whole-heartedly agreed with the programs that led to the pile-up of

low-quality bonds on the ECB's balance sheet.

Summing up, the US

monetary system is problematic in that it gets in the way of economic

progress, but it is much less fragile than the euro-zone monetary system.

That's why the euro-zone system will be the first to collapse.

The Stock Market

The US

Does valuation matter anymore?

Valuation has only ever mattered to the extent that it created long-term

downside risk or upside potential. It has never been a market timing

indicator.

When the valuation of the average stock is near the top

of its historic range we can be confident that the stock market will

generate a poor real return over the coming 10 years, but high valuation

(on its own) will never be a good reason to enter a short-term or

intermediate-term bearish speculation. And when the valuation of the

average stock is near the bottom of its historic range we can be confident

that the stock market will generate a good real return over the coming 10

years, but a low valuation (on its own) will never be a good reason to

enter a short-term or intermediate-term bullish speculation.

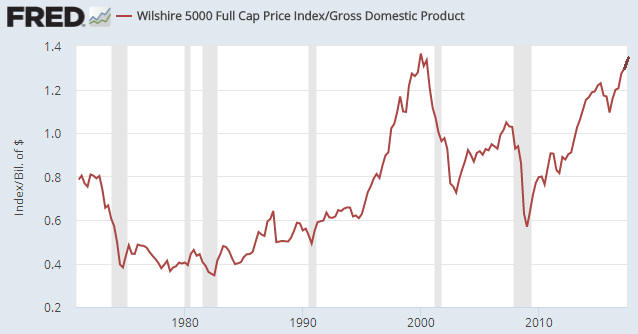

Currently, by all measures we know of the US stock market's valuation is

near the top of its historic range. The measure we'll focus on today is

market capitalisation relative to GDP.

The following chart shows

that the capitalisation of the US stock market, as indicated by the

Wishire5000 Index, is now within 3% its Q1-2000 peak relative to GDP (note

that the last part of the line on the chart was added manually based on

where we estimate the ratio will be when the Q3 GDP number is reported

late this month). The Q1-2000 peak in the Wilshire/GDP ratio was the

all-time high, meaning that the Wilshire5000 will have to rise by only an

additional 3% from here relative to GDP to establish the highest valuation

in history.

The implication of the above chart is that someone who now buys a fund

that mimics the performance of a broad-based US stock index will end up

with a negative return if they hold for 10 years. However, the chart says

nothing about the likely return that this person will achieve over the

coming 12 months. Furthermore, the probably-negative 10-year return will

not be generated by a downward trend lasting many years. Instead, it's

very likely that the declines that lead to the overall 10-year return

being negative will occur during periods with a combined length of less

than 3 years.

Current Market Situation

Over the first three days of this week the S&P500 Index tacked on

another 6 points and ended the 11th October session at an all-time high.

It therefore maintained its upward trend into the 10th anniversary of its

2007 peak.

Volatility remains low, complacency remains high and

there is no sign of weakness yet.

Japan

Mainly for the sake of interest we point

out that Japan's Nikkei225 Index is testing its 2015 peak. Refer to the

following weekly chart for details.

For what it's worth, our guess

is that the Nikkei won't make a sustained breakout in the near future but

will do so early next year. This guess is based on what we expect to

happen in other markets.

Gold and the Dollar

Gold

In

the latest Weekly Update we wrote that although the upward reversal in the

gold price on Friday 6th October wasn't impressive, the preceding strength

in the gold-mining sector relative to gold suggested that it had marked a

multi-week low. We concluded that a rebound to at least $1300 and possibly

as high as the $1350s was on the cards.

Over the first three days

of this week the gold price almost made it back to $1300, where there is

both lateral and moving-average resistance (the 50-day MA is now very

close to $1300). Getting through this resistance may require a larger

rebound in the T-Bond than has happened to date, which, in turn, may

require a significant pullback in the stock market.

If the gold price is capped over the days ahead by resistance near

$1300 then a decline to test the 6th October low ($1262) may follow. We

aren't inclined to establish a new hedge position at this time, though,

because we think that near-term downside risk is limited by support at

$1250-$1262.

Silver

The silver price

rebounded with the gold price over the first three days of this week. On a

daily closing basis this rebound has been capped to date by the 50-day and

200-day MAs.

With the exception of the downward spike in early

July, the silver price has spent the entire year in the $16.00-$18.50

range. We expect it to stay in this range for at least another month.

Gold Stocks

Current

Market Situation

Very little information about what the

future holds in store can be gleaned from the HUI's recent price action.

We think there's a slight short-term bias to the upside, but we aren't

interested in placing a bet. Instead, as mentioned in the Weekly Update we

are continuing to do what we do most of the time, which is scale into our

favourite stocks following sell-offs and take some money off the table

following price run-ups.

Something worth considering is that Q4 weakness in gold bullion and

gold-mining stocks may have become too predictable. In particular, in each

of the past four years the gold-mining indices were weak from

early-October through to at least mid-December and rebounded strongly from

a low in December or January. We don't know how widespread this view is,

but we have seen signs that some market participants are anticipating a

repeat performance over the next few months.

At this stage we are

not betting either way, but the fact that the HUI held its 200-day MA

during the recent sell-off could be an early warning that 2017 is not

going to follow the Q4 pattern established over the past four years.

We are very much open to the possibility that the gold-mining sector

will be 'surprisingly' strong during November-December. This could happen

in response to the broad stock market becoming 'surprisingly' weak over

the same period.

The proposed West

Australian gold royalty increase gets canned

The West

Australian Labour government had planned to increase the royalty paid by

gold producers from 2.5% to 3.75%, but the plan has been killed by the

opposition parties in the state parliament. The plan's death was confirmed

when the

Liberal Party voted against it on 10th October.

The 1.25%

additional royalty would not have significantly worsened the economics of

most gold-mining companies operating in the state, but because such

royalties are applied to the top line rather than the bottom line it may

have had a significant adverse effect on marginal producers. Thankfully,

it won't be happening.

The Currency Market

The Dollar Index (DX) has pulled back following last Friday's test of

lateral resistance at 94. Also, the downward reversal of the past few days

has helped to define channel resistance. Refer to the following daily

chart for details.

There is support at 92.5 and then at the 2017

low of 91.0. A breach of the higher support probably would be followed by

a test of the lower support.

Based on both sentiment and fundamental considerations, the worst the

DX should do over the weeks ahead is test support at 91 before resuming

its recovery.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://research.stlouisfed.org/

![]()