![]()

![]()

![]()

![]()

- Interim Update 12th July 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Interest rates will

rise until stock prices tank

The stock market will usually

view a new downward trend in bond prices and the associated upward trend

in interest rates as a minor issue until a point is reached when falling

bond prices (rising interest rates) are the only issue that matters. After

this 'point of recognition' is reached, the downward trend in the bond

market begins to have a very negative effect on the stock market.

A

good example of the bond-stock relationship outlined above is illustrated

by the following chart. The chart shows the performances of the S&P500

Index (SPX) and the 30-year T-Bond price during 1986-1987.

With

reference to this chart we note that the stock market had a scare in

April-1987 when the T-Bond broke below support to a new 9-month low. In

fact, during the first half of April the stock market began to form a

crash pattern and it possibly would have crashed in late-May or early-June

if the T-bond hadn't rebounded sharply after making a short-term bottom in

the second half of May. As it was, the T-Bond's rebound from its May low

and its ability to remain above this low until late-August temporarily

removed a potentially-serious threat and enabled another upward leg in the

SPX bull market.

Near the end of August, however, the T-Bond broke

below its May low and in doing so signaled the resumption of its downward

trend. This was the 'point of recognition' for the stock market -- the

point when a critical mass of market participants realised that the rise

in interest rates was inexorable and totally incompatible with current

equity valuations.

Another crash pattern immediately began to form

(the T-Bond's August-1987 break to a new low for the year coincided almost

to the day with the SPX's final top) and this time there was no T-Bond

rebound to prevent the pattern from completing. The T-Bond did rebound

very strongly in October-1987, but this was a reaction to the stock

market's crash.

A similar chart comparison covering the past two years is shown below,

except that in this case we have used the 10-year T-Note price as our

bond-market proxy.

The chart identifies support defined by the

December-2016 and March-2017 T-Note lows as the critical level -- the

level beyond which falling bond prices (rising interest rates) would

dominate all other considerations and put irresistible downward pressure

on the stock market. However, the 'point of recognition' could occur at a

higher level for the T-Note price. For example, if the T-Note were to

rebound strongly over the next few weeks then the early-July low would

possibly become the critical level.

More importantly, regardless of

the amount of additional bond-market weakness it takes to bring about

major weakness in the stock market, now that a certain relationship has

been established it's a good bet that the bond market's downward trend

will continue until there is major weakness in the stock market. In other

words, to get more than a short-lived respite from rising interest rates

the stock market will have to plunge.

Zinc Update

Early this year the per-pound

zinc price made a 9-year high in the US$1.30s. It then dropped back to a

low of around US$1.10 in May before reversing course and quickly returning

to the vicinity of its early-2017 high. In other words, the zinc price is

currently close to a 9-year high.

The reason for zinc's price strength is a bullish supply-demand

situation. This is evidenced by the following chart showing the amount of

zinc stored in LME warehouses. The chart shows that the LME zinc inventory

has fallen from around 1.2M tonnes during the first half of 2013 to only

280K tonnes.

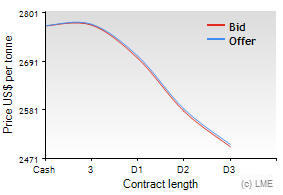

The bullish supply-demand situation is also evidenced by the following

chart from the LME

web site showing the term structure in the zinc futures market. The

downward-sloping curve, which indicates that the later-dated contracts are

cheaper than the earlier-dated contracts (D1, D2 and D3 on the chart's

horizontal axis mean December-2017, December-2018 and December-2019,

resp.), indicates a tightness of supply.

Interestingly, although the zinc price has moved back to near its

high, the prices of most zinc-related stocks are a long way below their

12-month highs. This creates an opportunity.

The zinc price is a

little stretched to the upside on a short-term basis and will possibly

consolidate over the next few weeks, but if the fundamentals remain

bullish then a sustained break above the early-2017 high is likely within

the next three months. If/when that happens it should cause the

speculative demand for zinc-related equities to ramp up, leading to large

rises in the prices of many junior zinc-mining stocks.

There are

numerous junior zinc explorers and developers that would benefit from

increasing zinc-related speculation, but at this time Solitario Zinc (XPL)

is our sole stock pick in this area. XPL has a good mixture of

exploration-stage zinc assets and balance-sheet strength.

The Stock Market

The US

On Wednesday 12th July the SPX broke out to the upside from what now

appears to be a routine 3-week consolidation pattern.

The NDX didn't break out to the upside on Wednesday, but it is close

to doing so and it has been strong enough to negate last week's break

below lateral support at 5650.

Both the SPX and the NDX remain below their June highs, so it's

possible that this week's strength will prove to be part of a

counter-trend rebound. It's also possible that one or both of these

indices will make new highs within the coming week and then reverse

downward almost immediately.

The latter of the aforementioned

possibilities (a false/misleading upside breakout) would be similar to

what happened at this time two years ago, when the NDX clearly broke above

a well-defined resistance level to a new high for the year three days

prior to the start of a 5-week plunge. Here's the relevant chart:

Regardless of these realistic bearish possibilities, short-term

traders should keep bearish speculations on a tight leash. The reason is

that even if the stock market is destined to be much lower 6 months from

now, it could move sharply higher over the coming 1-2 months as part of a

final speculative fling.

As previously advised, the QID (2X inverse

QQQ) trade in the TSI Stocks List will be exited if the NDX closes at or

above 5910.

Commodity-related equities

Although there have recently been signs of a speculative shift toward

"inflation" plays, many commodity-related equities remain in consolidation

mode. As mentioned above with regard to zinc stocks, this creates an

opportunity. Specifically, if metals such as zinc and copper break above

their early-2017 price highs then the associated equities should

experience strong rallies.

We usually concentrate on the small-cap

stocks, because this is where the greatest mispricing tends to occur. That

being said, Freeport McMoran (FCX), the world's largest publicly-traded

copper producer, could be a reasonable short-term or intermediate-term

speculation at this time. This is due to its chart pattern and the strong

potential for the copper price to make a new multi-year high within the

next few months.

The following chart shows that FCX has essentially

been consolidating with a slight upward bias for more than a year. The

pattern suggests the potential for a rise to at least $20 within 6 months,

but to maintain this potential the price must not close below $11.00.

Gold and the Dollar

Gold

In

the TSI commentary posted on Sunday 9th July we guessed that at least a

1-2 week rebound would get underway early this week. Such a rebound

appears to have begun following a spike to a marginal new low for the move

on Monday.

At this stage there's no reason to anticipate anything more than a

2-week (or thereabouts) rebound prior to the start of a decline to new

multi-month lows, but, as always, we'll try to take the evidence as it

comes. The evidence will include the evolving fundamental and sentiment

backdrops.

With regard to sentiment, the COT numbers scheduled to

be reported this Friday will be very interesting for both gold and silver.

This is because they will show how the speculating community reacted to

the breaches of important support levels that occurred late last week.

Evidence of speculator capitulation would be helpful to the bullish

case.

Gold Stocks

The gold-mining sector

has started to rebound as expected. In the case of GDX (the Gold Miners

ETF), the rebound has begun from support defined by the March and May

lows.

We are probably dealing with a counter-trend rebound prior to

a decline to new multi-month lows. If so, the most likely places for the

rebound to end are the 200-day MA and the downward-sloping trend-line

linking the February, April and June peaks. By the same token, a solid

daily close above the aforementioned trend-line would suggest that our

short-term outlook is too pessimistic.

The Currency Market

On Wednesday 12th July the

Bank of Canada (BOC) made its first interest-rate hike in 7 years. It

boosted its targeted overnight rate by 0.25% -- from 0.50% to 0.75%. The

rate hike was clearly telegraphed by the BOC over the preceding few weeks

and should have been expected by everyone, but the Canadian dollar (C$)

still moved sharply higher in reaction to the news.

The C$'s

performance over the past two months is a good example of what can happen

after speculators pile onto one side of a trade. In this case, leveraged

speculators built up a record-high collective net-short position in C$

futures, most likely in response to the belief that Canada's property

bubble was in trouble. Canada's property bubble might be in trouble, but

this was not a good reason to make a huge bet against a currency that

reliably moves with global commodity trends.

Perhaps the C$ will

reach intermediate-term lateral support at 80 before embarking on a

sizable 'corrective' move to the downside, but with the daily RSI now at

its highest level in 3 years it probably makes sense for anyone trading

the C$ from the long side to make at least a partial exit.

In the wake of the UK general-election on 8th June the British Pound

dropped back to its 200-day MA near 126. It could have been worse, as this

constituted only a minor and short-lived breach of support in reaction to

evidence that the UK's political situation is much riskier than previously

believed.

Assuming (as we do) that an 8-year cycle low was put in

place by the Pound during the first quarter of this year, plausible

targets for an intermediate-term peak lie at 134 and 140.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.kitco.com/

![]()