![]()

![]()

![]()

![]()

- Interim Update 12th August 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Commodities

Lithium to be boosted by

European EV demand

When forecasting the growth rates of

Electric Vehicle (EV) sales and the associated rate of growth in the

demand for battery metals, the focus tends to be on China and the US.

However, the article posted

HERE makes the point that Europe is now leading the way in EV sales

growth and the demand for EV-related materials. Here is an excerpt from

the article:

"S&P Global Market Intelligence expects global

lithium demand to increase by 91 per cent from 2019 to 2024, reaching

536,000 metric tonnes of lithium carbonate equivalent.

Electric

vehicles are expected to account for nearly three-quarters of that demand

increase. Global passenger electric vehicle sales are expected to rise to

6.2 million units in 2024, about three times higher than in 2019.

Market watchers have focused on this year's sales slump in China and North

America, but the EU has quietly gone the other way: there was a 69 per

cent year-on-year surge in European passenger electric vehicle

registrations in the first five months.

With France and Germany

trowelling on the subsidies for electric vehicle producers and buyers, S&P

reckons sales growth could hit 45 per cent during 2020, even in the midst

of the massive pandemic-led economic contraction."

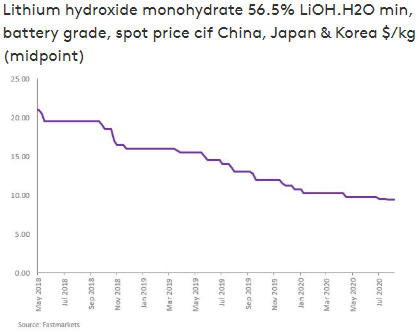

The

following chart shows that the multi-year bearish trend in the lithium

price has not ended, but even based on what we think are conservative

estimates of future EV sales it could end this year and should end by the

first half of next year at the latest. When it does it is reasonable to

expect that the upward trends in the stock prices of lithium

producers/developers that got underway over the past several months will

accelerate.

Source:

https://www.fastmarkets.com/

Our favourite lithium stock at

this time is Galaxy Resources (GXY.AX). GXY has current production at a

hard rock lithium mine in Western Australia, which means it will gain an

immediate financial benefit when the lithium market turns the corner, and

has huge organic growth potential due to its ownership of a

development-stage lithium-brine project in Argentina.

We also like

European Metals Holdings, which was mentioned in the above-linked article

and trades on both the ASX and the AIM (London market) under the symbol

EMH.

EMH owns 49% of the Cinovec project in the Czech Republic

(CR). This project has the largest hard rock lithium deposit in Europe and

the fourth-largest hard rock lithium deposit in the world. According to a

PFS completed in June-2019, at a cost of US$483M the Cinovec deposit could

be developed into a mine that produces 25,300 tonnes/year of lithium

hydroxide or 22,500 tonnes /year of lithium carbonate. Assuming a lithium

hydroxide price of US$12.00/kg, the post-tax NPV(8%) and IRR were

estimated in the PFS to be US$1.1B and 29%, respectively. The current

lithium hydroxide price is only US$9.40/kg, but we wouldn't have any

interest in lithium mining stocks if we didn't expect that the lithium

hydroxide price will be above US$12.00/kg within two years.

Based

on the PFS figures, EMH's 49% stake in the Cinovec project is worth about

US$550M (A$760M at the current exchange rate). Applying a risk discount of

50% and dividing by the current EMH share count (156M) gives us a

potential value of A$2.40/share for EMH at a lithium price of US$12/kg.

EMH currently is trading at A$0.30/share, so there is massive

valuation-related upside.

Adding to EMH's speculative appeal is the

fact that the other 51% of the project is owned by CEZ, a large industrial

corporation (2019 EBITDA of 2.4B euros) headquartered in Prague (the

capital of the CR). CEZ is 70% owned by the Czech State, so in effect

EMH's partner is the Czech government. This should make permitting fairly

straightforward. Also, CEZ purchased its stake earlier this year via an

investment in the project of 29M euros. This investment should mean that

the project is fully funded through to a construction decision sometime

next year.

GXY is a current TSI stock. EMH may be added to the TSI Stocks List in

the future, but for now we will put it in the

TSI Small Stocks Watch List.

Platinum price to be

supported by declining SA production

Platinum demand is

immersed in a long-term decline, but that didn't stop the platinum price

from rebounding to US$1,000/oz from a March-2020 low in the US$500s and in

our opinion won't stop the price from continuing to trend upward over the

coming 12 months. The drivers of the upward trend have been, and should

continue to be, a flood of new money courtesy of central banks (mainly the

Fed) and declining production in South Africa (SA).

The Bloomberg

article posted

HERE addresses the latter of the above-mentioned price drivers. The

article points out:

"Beset by power and water shortages,

alongside whipsawing government policies, South African producers have cut

spending over the past decade on mines responsible for 75% of global

platinum supply."

And:

"Platinum output peaked in

2006, and the lack of investment in deep-level western limb shafts will

result in a further sharp contraction in production over the next 10

years."

There is also the fact that the labour-intensive

mining that happens in South Africa has been made less efficient by the

COVID-related requirement to have greater distances between workers.

The following chart shows that the platinum price has pulled back

after testing resistance defined by its highs of the past 3 years. The

short-term risk/reward is neutral, but the intermediate-term risk/reward

remains bullish.

Oil is close to an upside breakout

The oil

price has moved slightly above long-term support/resistance at US$42.00,

but it hasn't managed to get above its 200-day MA yet. On Wednesday 12th

August it closed exactly at its 200-day MA.

We remain

intermediate-term bullish on oil, but the next $5-$8 move could go either

way. A daily close above the 200-day MA would suggest that it will be to

upside.

Industrial commodities such as oil and copper have been outperforming

gold since April. After the T-Bond yield embarks on a rising trend, which

may have just happened, the outperformance should become more pronounced.

The Stock Market

The S&P500 Index crashed during

the first quarter of this year without going through a "crash pattern"

involving a major high, an initial decline, a rebound that retraces

50%-100% of the initial decline, and a second decline that turns into a

crash after the low of the initial decline is breached. However, the

broader NYSE Composite Average (NYA) did follow the typical crash pattern,

with a major high in mid-January, a secondary (slightly lower) high in

mid-February and then a crash in March, with the whole process taking

about two months. Note that two months is the same amount of time that it

took for crash patterns to complete in 1929 and 1987.

Following

the 1929 crash there was a rebound lasting almost exactly 6 months and

then a downward trend lasting more than two years that didn't bottom until

the Dow Industrials Index (Dow) was trading at only 10% of its 1929 peak.

Here's a daily chart that shows the Dow's peak-to-trough performance

during 1929-1932.

Source:

https://www.macrotrends.net/2484/dow-jones-crash-1929-bear-market

Due to the fact that we now have massive monetary inflation as opposed

to the monetary deflation that characterised the 1930-1932 period, a

repeat of 1930-1932 will NOT happen over the next couple of years.

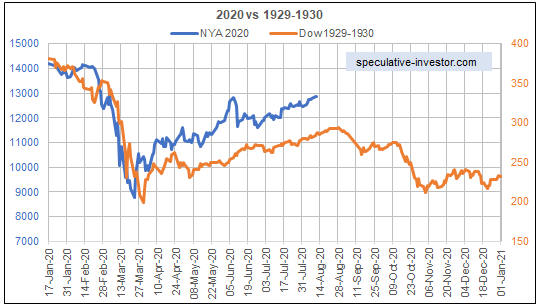

However, it's more than a little interesting that the NYA has followed the

Dow's 1929-1930 path quite closely up until now. This is illustrated by

the following chart. The chart compares the NYA from its 17th January 2020

peak with the Dow from its 3rd September 1929 peak.

If the similarities between the present and 1929-1930 persist in the

short-term, then the rebound from the March-2020 low will end within the

next two weeks and the next tradable low will coincide roughly with the US

Presidential election in early-November.

We wouldn't bet heavily on

the similarities being maintained, but the above chart comparison adds to

the existing reasons to view the short-term risk/reward as decidedly

skewed towards risk.

Due to the high short-term risk, we are adding

a new bearish speculation to the TSI List. There already is an IWM

(Russell2000 ETF) October-2020 put option in the List, but on a short-term

basis we think that QQQ (the NASDAQ100 ETF) has greater downside

potential. Therefore, we are adding QID, a leveraged ETF that moves

inversely to QQQ, at Wednesday's closing price of US$10.28 (see chart

below). In an effort to get more bang for the buck, we also are adding the

QID October-2020 US$11.00 call option at Wednesday's closing price

(US$0.80). The plan at this time is to:

1) Average into the bearish

positions over the next two weeks.

2) Take a profit on the QID call

option during September.

3) Hold the ETF itself until around the

time of the US election.

Note that due to the strong positive

correlation between the NDX and the HUI, in addition to being bearish

speculations the QID positions mentioned above could be used to hedge a

gold stock portfolio.

Gold and the Dollar

Gold

In

the 3rd August Weekly Update, we wrote:

"...we will be

surprised if the gold price does not trade $100-$300 below its current

price within the next three months."

When we made the above

comment the price was US$1986. Despite subsequently trading about $100

higher, the gold price already has traded $110 below the aforementioned

level. This represents a huge increase in volatility, with the steady

advance of mid-July through to early-August replaced by dramatic intra-day

swings.

The following daily chart shows that by early-August the

gold price had moved well above long-term resistance defined by its 2011

high and that over the past four trading days it returned to this former

resistance (now support) in spectacular fashion. The chart also shows that

this new lateral support level survived a test over the past two days, as

did the 20-day MA.

It's unlikely that the downward spike and upward reversal on Wednesday

12th August marked the end of a correction, but it probably marked the end

of the first part of a correction. Our guess is that there now will be a

rebound lasting anywhere from one to three weeks followed by a decline

that takes out this week's low. The rebound, assuming it happens, should

be viewed as a short-term selling opportunity.

Silver

We rarely use the "crash" word when discussing what's likely to happen

in a market. We used it multiple times in January-February of this year

when discussing the gold mining sector's short-term prospects and we used

it in the latest Weekly Update when discussing silver's short-term

prospects. Specifically, in the latest Weekly Update we wrote: "It

looks like the silver market is setting up for a crash...".

It's debatable whether silver's price plunge from last Friday's high near

$30 to Wednesday's low of $23.58 qualifies as a crash. A price decline of

more than 20% within the space of four trading days certainly would be a

crash in some markets, but within the context of the current manic silver

market it possibly could be viewed as nothing more than a pullback. After

all, it didn't even result in a daily close below the 20-day MA.

Although it hasn't yet registered a daily close below the 20-day MA,

the ferocity of silver's reversal from last Friday's high is evidence that

a multi-month price top is in place. It would be normal for the initial

decline from the high to be followed by a rebound that retraced 50%-100%

of the initial decline, after which a larger decline would begin. As is

the case with gold, this rebound, assuming it happens, should be viewed as

a short-term selling opportunity.

As stated in the latest Weekly

Update, we suspect that the correction in the silver market will take the

price down to the vicinity of the 200-day MA. The 200-day MA presently is

at $17.71, but it is rising and probably will reach lateral support at $19

by October. There is also support at around $21 that could come into play

within the next few weeks.

Gold Stocks

Current Market Situation

In the

latest Weekly Update, we wrote:

"...we are into the one-month

time window that has provided either the annual high or the annual low for

the HUI in each of the past five years. Clearly, if this cyclical tendency

remains in force then the early-August through to early-September period

of 2020 will contain an important high. The high could have been set by

the HUI's spike to 374 last Wednesday or it could be set within the next

four weeks.

In any case and as mentioned in previous commentaries,

it will be reasonable to assume that the short-term upward trend is intact

until the HUI ends a day below its 20-day MA. This moving average

currently is at 338."

The first of the following daily charts

shows that the HUI closed below its 20-day MA on each of the past two

trading days. Furthermore, the second of the following charts shows that

the HUI/gold ratio has broken below its 40-day MA. This is clear-cut

evidence that a multi-month price top was set by the HUI's spike to 374

last Wednesday (5th August).

The HUI has support at 300-310, 286 and 260. Our guess at this time is

that the lowest of these support levels will come into play before the

correction ends.

There could be a rebound over the coming 1-3 weeks

that retraces 50%-100% of the decline from last week's high, but we don't

think it makes sense to buy in anticipation of such a rebound. The reason

is that despite the significant pullback of the past few days, the

short-term risk/reward is neutral at best.

What to do?

Over the past few

weeks, managing our holdings of gold stocks and other commodity-related

equities has been more of a balancing act than usual. We have been trying

to make hay while the sun shines, but at the same time we have been

preparing for the dismal weather to come.

We have been preparing

for the coming 'bad weather' by taking money off the table as short-term

selling opportunities presented themselves. In addition, we have a plan to

purchase some insurance in the form of put options later this month if

there's a decent rebound from this week's lows in the gold mining ETFs.

As per our money management practice, we also have maintained

significant (core) exposure to "inflation" plays. This is because much

higher prices are likely during the first half of next year and there's

always the risk that things will happen faster than we expect. Note that

gold mining stocks can benefit from rising "inflation" expectations, but

industrial-metals mining stocks are better suited to such conditions

until/unless there is a major decline in monetary confidence.

The Currency Market

The Dollar Index (DX) appears

to be basing, but it must close above 94.0 to signal an upward reversal.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Input

Capital (INP.V) to be acquired

Input

Capital (INP.V) to be acquired

In the latest Weekly Update

we suggested buying the shares of Input Capital (INP.V), an agriculture

streaming company, due to the large discount to book value at which the

shares were trading (the stock was trading at C$0.80 and the per-share

book value was estimated to be about C$1.33). Congratulations to those who

followed our suggestion, because thanks to a C$1.75/share all-cash

takeover bid announced after the close of trading on Wednesday 12th August

you have just doubled your money in three days on a relatively low-risk

speculation.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

http://bigcharts.marketwatch.com/

![]()