![]()

![]()

![]()

![]()

- Interim Update 12th September 2018

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Getting exposure to

food

We are long-term bullish on the

prices of food commodities, especially the grains. However, it is not easy

to obtain long-term exposure to food commodities via the major financial

markets, at least not in a cost-effective way.

Getting short-term

exposure to grain prices is straightforward. It can be done by purchasing

futures or by purchasing ETNs/ETFs such as JJGTF (iPath Grains Total

Return ETN) and DBA (Invesco DB Agriculture Fund). The problem with trying

to invest for the long-term via commodity futures or funds that hold

commodity futures contracts is that under normal market conditions there

will be regular value leakage due to the "futures roll*". This leads to

the investment performing much worse than suggested by the performance of

the spot commodity price.

For example, JJGTF has performed much

worse since its inception than the spot prices of the grains it is

designed to track. In particular, whereas the spot prices of corn,

soybeans and wheat have approximately gone sideways over the past four

years, the first of the following charts shows that JJGTF has been in a

strong downward trend over this period. The second of the following charts

shows that DBA hasn't fared any better.

An alternative to buying funds that hold the commodity futures would

be to buy shares of the companies that produce the commodities. The

problem is that the most likely reason for a huge rally in grain and other

food-related commodity prices is reduced supply due to unseasonal weather

and/or changing climatic conditions. The implication is that high

commodity prices will coincide with lowered production and reduced

profitability for many producers. It will be impossible to predict which

producers will be left unscathed, and therefore in a position to profit

from, the weather conditions that bring about the supply disruption.

As far as we can tell, taking risk and potential reward into account

the best way to obtain LONG-TERM exposure to food commodities via the

major financial markets is to buy the shares of fertiliser producers.

These companies could benefit either from higher prices due to reduced

supply or from an increase in production.

It's obvious that we

aren't the only ones to figure this out given that the stock prices of

Nutrien Ltd. (NTR) and The Mosaic Company (MOS), two of the world's

biggest and best-known fertiliser producers, have been steadily rising

even though the prices of corn and soybeans are languishing near 9-year

lows. As illustrated by the following charts, NTR has been trending upward

since early-2016 and MOS has been trending upward since completing a

double bottom in Q3-2017. However, the charts also show that on a

long-term basis both NTR and MOS are much closer to the bottoms than to

the tops of the ranges that were established way back in 2008. Also, their

valuations are reasonable. This suggests that if new bull markets have

begun, they are still in their infancy.

If you are looking for long-term investments that will benefit from

rising agricultural-commodity prices and/or increasing global production

of food, the above stocks are good places to start. They will get dragged

down by the next meaningful decline in the broad stock market, but the

occasional sharp correction shouldn't be a problem for an investor

employing an averaging-in approach.

*When a

futures market is in "contango", which is the normal state of affairs for

most commodities, the contracts with later expiry dates have higher

prices. Consequently, 'rolling' from an earlier to a later futures

contract results in a loss.

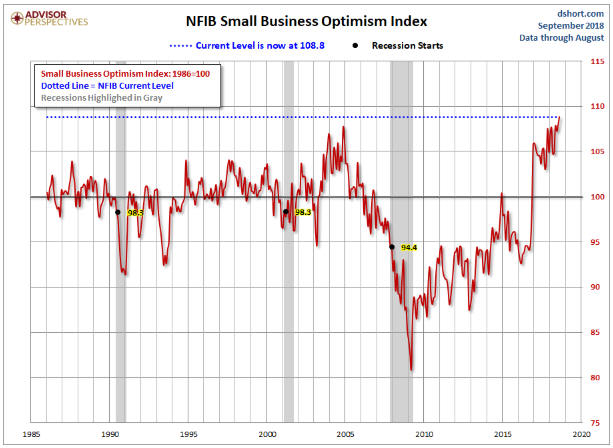

Business optimism

continues to rise

The following chart shows that

the NFIB Small Business Optimism Index hit an all-time high last month.

Although this may well be as good as it gets, the implication is that the

US economy is a long way from commencing a recession (the last three

recessions didn't begin until after the Optimism Index dropped below 100).

Chart source:

Doug Short

The Stock Market

The senior US stock indices did

nothing significant during the first three days of this week, but there

were some interesting developments beneath the surface.

The US

stock market has been rife with divergences over the past few months, one

of which is that strength in some of the high-profile stock indices has

gone with lacklustre performance on the part of the Bank Index (BKX). This

divergence became more pronounced on Wednesday 12th September, with the

BKX dropping below its 50-day and 200-day MAs (refer to the top half of

the following chart) and the BKX/SPX ratio dropping to within spitting

distance of its 12-month low (refer to the bottom half of the following

chart).

By the way, if you want a fundamental explanation for why

the gold market perked up on Wednesday, the sharp decline in the BKX/SPX

ratio is it. The relative strength of the banking sector is one of the

seven inputs to our Gold True Fundamentals Model (relative weakness in the

banking sector puts upward pressure on the gold price).

Critical

support for the BKX is near 104, or about 4% below the current price.

Here's a chart we haven't shown for about three months. It compares

the Bitcoin price (in green) with the S&P500 Index. The idea behind the

chart is that Bitcoin -- for whatever reason -- is leading the SPX and

that divergences are resolved by the SPX moving back into line with

Bitcoin. With Bitcoin near its low for the year and the SPX not far from

its high for the year, the current divergence is large and potentially

bearish for the SPX.

At this time we are following the Bitcoin-SPX

relationship more for the sake of interest than to identify trading

setups. The divergence is not something on which we would predicate a

bearish speculation, although there are reasons to expect a sizable move

in one direction or the other within the next few weeks and to suspect

that the direction will be down.

By the way, although the Bitcoin

price has fallen from around $20,000 in December-2017 to around $6,000

today, it has held up better than we thought it would. It essentially has

gone sideways since its December-January crash and is still up on a

year-over-year basis. This suggests that there is plenty of underlying

demand and that it would be premature to announce the death of the world's

first cryptocurrency.

Gold and the Dollar

Gold

The

US$ gold price broke above its short-term channel top on Wednesday 12th

September. Within $10 of Wednesday's closing price there is both lateral

resistance ($1220) and MA resistance (the 50-day MA), and above that there

is more lateral resistance at $1240.

We think that if the gold price achieves consecutive daily closes

above $1220 then it will work its way up to around $1280 over the ensuing

weeks. That's regardless of whether the fundamental backdrop turns bullish

or stays bearish.

Gold Stocks

The most

important gold-mining indices and ETFs made new 2-year lows on Tuesday

11th September and then rebounded quite sharply on Wednesday. So, what are

the chances that a multi-month bottom is now in place? Before answering

this question it's worth reviewing what happened to the gold-mining sector

over the past month, using GDX as the sector proxy.

In mid-August,

GDX's daily RSI(14) hit a rare extreme. As noted on the following chart,

it was the second-lowest level for this short-term momentum indicator in

10 years. We stated at the time that regardless of whether or not there

were new price lows over the weeks ahead, this would prove to be the

downward trend's momentum extreme.

Downward momentum extremes of

the sort experienced by GDX in August-2018 generally don't mark

sustainable price lows. More often than not there's a counter-trend

rebound and then a decline that tests or breaches the momentum price low

prior to the start of a tradable rally. With the momentum extreme in place

it goes without saying (but we'll say it anyway) that a decline to a new

price low would create a positive divergence between the RSI and the

price.

The rebound from the mid-August low was lacklustre and after

two weeks it still hadn't reached the 20-day MA. This indicated that it

was a counter-trend move and that a decline to new lows would occur either

in the near future or following a couple of months of upward drift. The

decline to new lows happened on 4th September, after which there was

additional downside and then a bottom on 11th September. Naturally, the

11th September bottom coincided with a higher low for the daily RSI, thus

creating the positive divergence mentioned above.

Which brings us back to the question: What are the chances that a

multi-month bottom is now in place?

The chances are good, because

we now have a) a new price low following a momentum extreme, b) a positive

divergence between price and momentum at this week's low, and c) a

divergence between gold bullion and the gold-mining sector at this week's

low (a higher low for gold alongside lower lows for the gold-mining

indices/ETFs).

The next question is: Assuming that at least a

multi-week bottom was put in place on Tuesday 11th September, what is a

reasonable upside target?

A reasonable initial upside target is the

50-day MA. For GDX this is a bit more than 10% above the current price.

The way the 50-day MA is reached will provide clues regarding whether

there is more upside to come. In particular, a fast move up to the 50-day

MA would suggest that there is significant additional short-term upside in

store whereas a slow/choppy rise to the 50-day MA would suggest that we

are dealing with another minor reaction within an on-going downward trend.

In the latter case, a rise to near the 50-day MA would create an

opportunity to buy put options to profit from or hedge against a decline

to new multi-year lows.

The Currency Market

It's possible that the Dollar Index (DX) and the euro are in the

process of completing H&S reversal patterns, with "possible" being the

operative word. This was discussed in the latest Weekly Update and nothing

has changed.

Due to its recent price action, the Australian dollar

(A$) is worthy of an update today.

As illustrated below, during

the first two trading days of this week the A$ spiked below the bottom of

a declining 'wedge'. Since the 'wedge' is steeply sloped, this has the

look of a downside blow-off. It also spiked below intermediate-term

lateral support.

Wednesday's rebound wasn't strong enough to mark

the preceding downside breakouts as false, but the potential is there.

Furthermore, the A$'s COT situation is very bullish.

It would be reasonable for risk-averse speculators to buy FXA here and

place an initial sell stop slightly below this week's low, whereas

aggressive speculators could consider buying FXA December-2018 $75 call

options. These options ended Wednesday's session at US$0.25-$0.35.

The TSI Stocks List contains an FXA September-2018 $80 call option

that will expire worthless at the end of next week. We are going to record

the loss and replace the expiring option with the one mentioned above,

using US$0.30 (the middle of the current bid-ask spread) as the starting

price for record purposes.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

![]()