![]()

![]()

![]()

![]()

- Interim Update 13th February 2019

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Some thoughts on Modern

Monetary Theory

Modern Monetary Theory, or MMT

for short, is gaining in popularity in the US. It is based on the idea

that under the current monetary system the government doesn't have to

borrow. Instead, it simply can print all the money it needs to fill the

gap between its spending and its income. The only limitation is

"inflation". As long as "inflation" is not a problem the government can

spend -- using newly-created money to finance any deficit -- as much as

required to ensure that almost everyone is gainfully employed and to

provide all desired services and infrastructure. It sounds great! Why

hasn't anyone come up with such an effective and easy-to-implement

prosperity scheme in the past?

Of course, it has been tried in the

past. It has been tried countless times over literally thousands of years.

The fact is that there is nothing modern about Modern Monetary Theory. It

is just another version of the same old attempt to get something for

nothing.

Most recently, MMT has been put into effect in Venezuela.

For all intents and purposes, the government of Venezuela has been

printing whatever money it needs to pay for the extensive 'free' social

services it promised to the country's citizens. The MMT apologists

undoubtedly would argue that the money-printing experiment didn't work in

Venezuela because the government didn't pay attention to the "inflation"

rate. It kept on printing money at a rapid pace after "inflation" became a

problem. Our retort would be: "Good point! Who would have thought that a

government with the power to print money couldn't be trusted to stop

printing as soon as an index of prices moved above an arbitrary level."

In essence, MMT is based on the fiction that the government can

facilitate an increase in overall economic well-being by exchanging

nothing (money created 'out of thin air') for something, or by enabling

the recipients of the government's largesse to exchange nothing for

something. It is total nonsense.

New wealth can't be created by

printing money, but existing wealth will be redistributed. It's like when

a private counterfeiter prints new money for himself. When he spends that

money he diverts real wealth to himself while contributing nothing to the

economy. MMT is the same principle applied on a gigantic scale.

As

is the case when money is loaned into existence under the current system,

the application of MMT will affect relative prices as well as the

so-called "general price level". The reason is that the new money won't be

injected uniformly across the economy. However, it's likely that the price

increases stemming from the monetary inflation will be more uniform and

direct under MMT than under the current system. In other words, under MMT

the effects of monetary inflation should be reflected much sooner and to a

far greater extent in the CPI than is the case with the current system.

That the application of MMT would lead quickly to what most people

think of as "inflation" is a benefit, because the link between cause

(monetary inflation) and effect (rising prices) would be obvious to almost

everyone. A related benefit is that MMT would short-circuit the boom-bust

cycle.

Booms happen when the Fractional Reserve Banking (FRB)

system (with or without a central bank) expands credit and in doing so

creates the impression that the quantity of real savings is much greater

than is actually the case, prompting excessive investment in long-term

business ventures that would not look viable in the absence of misleading

interest-rate signals. We assume that under MMT the commercial banks would

still be lending new money into existence, but the temporary downward

pressure on interest rates from the surreptitious money creation of the

banks would be more than offset by the upward pressure on interest rates

from the blatant money-printing of the government. The boom phase

therefore would be very short, perhaps even barely noticeable. In effect,

MMT would bypass the boom and go straight to the bust. Again, this would

be beneficial because it would expose the link between cause (the

application of a crackpot monetary theory) and effect (economic hardship

for most people).

MMT is such an obviously silly idea that any

economist, politician, journalist or financial-market commentator who

advocates it should not be taken seriously. However, that they are being

taken seriously opens up the possibility that MMT will be implemented in

the not-too-distant future, with the 'benefits' outlined above.

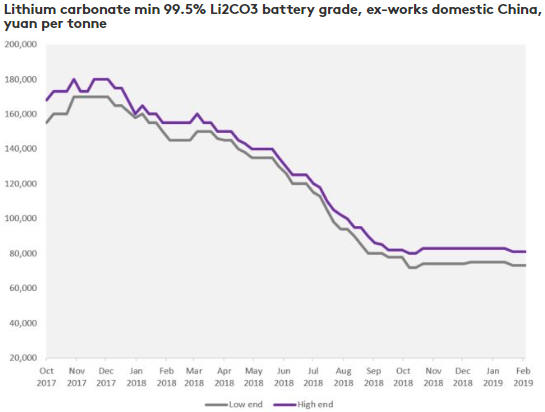

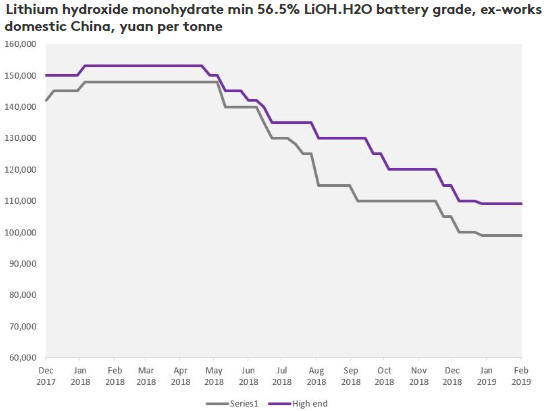

Lithium Update

There is an overview of the

lithium market, including brief descriptions of the two most important

lithium compounds (lithium carbonate and lithium hydroxide), in the 26th

December 2018 Interim Update. Prices have since moved sideways (refer to

the following charts for details), but price expectations have fallen,

that is, investors have become less optimistic about future prices. Most

recently, lithium sentiment took a hit on Monday of this week when U.S.

lithium producer Livent Corp

said that it expects demand for the white metal to sag in China for

the rest of the year.

The final paragraph from our 26th December lithium write-up remains

applicable. Here it is again:

"...there is a risk that all the

new investment in lithium hydroxide production now happening in Australia

will be more than sufficient to cater for the coming increase in demand,

but...we suspect that most forecasters are greatly under-estimating the

future EV-related demand for battery metals such as lithium. We therefore

like the idea of maintaining long-term exposure to well-financed lithium

hydroxide producers/developers such as Mineral Resources (MIN.AX) and

Kidman Resources (KDR.AX)."

The Stock Market

The US stock market has

continued its relentless march upward, enabling the S&P500 Index (SPX) to

close slightly above its 200-day MA on Wednesday 13th February.

Unfortunately, this doesn't tell us anything new of importance. Although

the initial rebound from the December low has now gone further than the

overall rebound was expected to go, the remarkable speed of the recovery

is not inconsistent with performance during the first several months of a

bear market. It neither confirms nor denies the bear market scenario. It

simply means that there is no evidence that the initial rebound is over.

Preliminary evidence that the initial rebound is over would be another

failure to achieve a weekly close above the 50-week MA. That will happen

if the SPX ends this week below 2730.

What we have at the moment is several US stock indices near 200-day MA

resistance, which implies that the market is stretched to the upside given

how far the indices had to travel from their December lows to get back to

this MA. We also have a put/call sell signal (see chart below). The

early-October market top occurred one week after the previous put/call

sell signal and a week has now gone by since the most recent signal. What

we don't have is a significant bearish divergence. In particular, the

Advance-Decline Line (ADL) shown in the bottom section of the above SPX

chart continues to confirm the SPX's strength.

If the market had dropped sharply over the past week then the

Fed-generated 'liquidity drain' that potentially will take place this

Friday or early next week could have precipitated a trend-ending plunge.

However, that's no longer a realistic possibility. There could be

significant weakness over the next few days due to the Fed's quantitative

tightening (QT), but if so it won't be the culmination of a multi-week

decline.

Gold and the Dollar

Gold

The

US$ gold price has done well over the past 4.5 months in the face of a

strong US$. This is explained by the fact that the US dollar's exchange

rate is only one of several important fundamental drivers of the gold

price. Taking everything into account, the fundamental backdrop has been

gold-bullish since the second week of December.

With one exception,

any decline in the gold price should be corrective (a counter-trend move

within an on-going intermediate-term rally) as long as gold's true

fundamentals stay bullish. The exception is when sentiment is dangerously

stretched into optimistic territory, warning that the bullish fundamentals

have been more than fully discounted in the current price. But even in

this case the fundamentals, as indicated by our GTFM, should begin to

deteriorate in the early part of an intermediate-term downward trend, thus

confirming the trend reversal in a timely manner.

Turning to the

daily price chart, we see that the gold price has been drifting lower

since the start of February. This correction probably will be limited by

support near $1280, although it could extend as far as $1250 without

signaling an intermediate-term reversal.

Gold Stocks

The 158-164 range for the HUI

contains three of the most useful moving averages and multiple lateral

support levels. The HUI ended Wednesday's session at the top of this

support range.

A routine correction within an on-going short-term upward trend could

take the HUI to the bottom of the aforementioned support range (158), but

no lower.

Of greater immediate importance than what the HUI does

in dollar terms is what it does in gold terms. As pointed out in a couple

of recent TSI commentaries, if the gold-mining sector is immersed in

something more bullish than a counter-trend rebound then the HUI/gold

ratio should hold above its 150-day and 40-day MAs during pullbacks over

the weeks ahead. By the same token, if HUI/gold drops below these MAs

within the next few weeks it won't mean that a multi-month top is in

place, but it will imply that the rally from the September-2018 low is no

more significant than the other rebounds of the past two years.

As

illustrated by the following chart, HUI/gold's 150-day and 40-day MAs are

only slightly below Wednesday's closing level. Consequently, there is not

much scope for additional near-term weakness in the gold-mining sector

relative to gold bullion.

The Currency Market

From the 31st December

Weekly Update:

"According to Brandt's research, there has been

a very strong tendency for the Euro (or trade-weighted proxy prior to

2002) to establish its annual high or low in the month of January or

early-February. To be specific, an annual low or high in EUR/USD has

occurred within the first six weeks of the year in 79% of years dating

back to 1971. Furthermore, the January Effect has produced an average

price advance or decline of 19.7%.

This will be useful information

if the euro moves sharply higher or lower over the weeks ahead and

reverses course by early-February. If this happens there will be a decent

chance that the high or low for the year has been set."

The

euro just made a new 3-month low, opening up the possibility that the

"January Effect" will create an important bottom this year. If the euro

reverses upward by early next week then the low for the year might be in

place.

For the euro, the most clear-cut and easiest-to-trade

BULLISH setup would involve a spike BELOW the November low during the

final two days of this week followed by an upward reversal. Traders could

then go long the euro in anticipation of a multi-month rally and manage

risk by placing an initial stop slightly below this week's low.

Unsurprisingly, the Dollar Index (DX) is in the opposite position. For

the DX, the most clear-cut and easiest-to-trade BEARISH setup would

involve a spike ABOVE the November high during the final two days of this

week followed by an downward reversal. Traders could then go short the DX

in anticipation of a multi-month decline and manage risk by placing an

initial stop slightly above this week's high.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://www.metalbulletin.com/LITHIUM-PRICES-UPDATE.html

![]()