![]()

![]()

![]()

![]()

- Interim Update 13th September 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Gold and the Yield

Curve

The yield curve is a remarkably

useful leading indicator of major economic and financial-market events.

For example, its long-term trend can be relied on to shift from flattening

to steepening ahead of economic recessions and equity bear markets. Also,

usually it will remain in a flattening trend while a

monetary-inflation-fueled boom is in progress. That's why we consider the

yield curve's trend to be one of the true fundamental drivers of both the

stock market and the gold market. Not surprisingly, when the yield curve's

trend is bullish for the stock market it is bearish for the gold market,

and vice versa.

A major steepening of the yield curve will have one

of two causes. If the steepening is primarily the result of rising

long-term interest rates then the root cause will be rising inflation

expectations, whereas if the steepening is primarily the result of falling

short-term interest rates then the root cause will be increasing risk

aversion linked to declining confidence in the economy and/or financial

system. The latter invariably begins to occur during the transition from

boom to bust.

A major flattening of the yield curve will have the

opposite causes, meaning that it could be the result of either falling

inflation expectations or a general increase in economic confidence and

the willingness to take risk.

On a side note, the conventional

wisdom is that a steepening yield curve is bullish for the banking system

because it results in the expansion of banks' profit margins. While

superficially correct, this 'wisdom' ignores the reality that one of the

two main reasons for a major steepening of the yield curve is widespread,

life-threatening problems within the banking system. For example, the

following chart shows that over the past three decades the US yield curve

experienced three major steepening trends: the late-1980s to early-1990s,

the early-2000s and 2007-2011. All three of these trends were associated

with economic recessions, while the first and third got underway when

balance-sheet problems started to appear within the banking system and

accelerated when it became apparent that most of the large banks were

effectively bankrupt.

Continuing with the side note, here's an

analogy that hopefully helps explain the relationship (under the current

monetary system) between major yield-curve trends and the

economic/financial backdrop: Saying that a steepening of the yield curve

is bullish because it eventually leads to a stronger economy and

generally-higher bank profitability is like saying that bear markets are

bullish because they eventually lead to bull markets; and saying that a

flattening of the yield curve is bearish because it eventually -- after

many years -- is followed by a period of severe economic weakness is like

saying that bull markets are bearish because they always precede bear

markets.

Both rising inflation expectations and increasing risk aversion tend

to boost the general desire to own gold, whereas gold ownership becomes

less desirable when inflation expectations are falling or

economic/financial-system confidence is on the rise. Consequently, a

steepening yield curve is bullish for gold and a flattening yield curve is

bearish for gold.

As discussed in a

TSI

blog post earlier this week, the US yield curve's trend has not yet

reversed from flattening to steepening. This means that the yield curve's

present situation is bullish for the stock market and bearish for the gold

market.

Currently, of the seven inputs to our Gold True

Fundamentals Model (GTFM) the yield curve is the only one that isn't

bullish.

The Stock Market

The S&P500 Index (SPX) broke

into new high territory over the past three days. This doesn't necessarily

mean that significant additional gains are going to occur, but it does

change the pattern from what was expected.

A September low is now

out of the question, but there is still a realistic chance of an October

low. A lot depends on what happens over the next few days. In particular,

a downward reversal followed by a daily close below 2460 would create a

very bearish set-up, while an ability to hold above 2480 until the end of

next week would suggest that we are dealing with a genuine upside breakout

and a significant extension to the upward trend that got underway last

November.

Gold and the Dollar

Gold

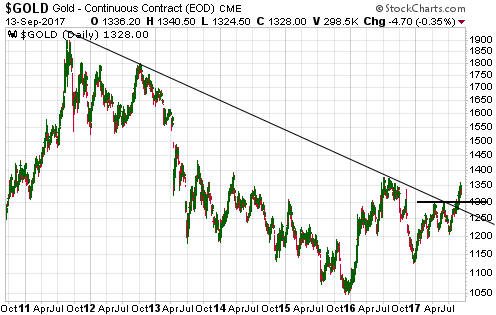

Looking for some historical context

In euro terms the early-July low in the gold price was below the

December-2016 low. In fact, it was a 16-month low. Also, in euro terms the

gold rebound from the early-July low has done no more to date than take

the price up to the declining 200-day MA. Refer to the following daily

chart for details. An implication is that this year's rise in the US$ gold

price has a lot more to do with US$ weakness than genuine gold-market

strength.

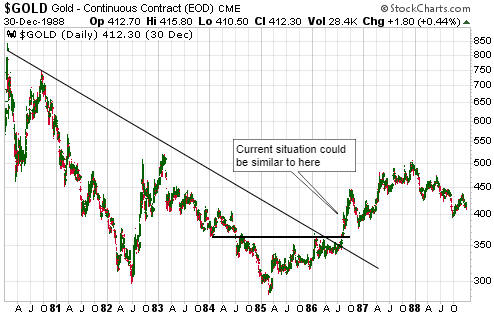

At this stage 1986-1987, when a gold rally occurred alongside an

upward-trending stock market, an economic expansion and a

downward-trending US$, appears to be a more relevant historical parallel

than 2001-2002, when a gold rally occurred alongside an equity bear

market, an economic recession and a topping US$. In particular, the

current situation could be similar to September-1986. At that time, in

response to relentless US$ weakness the US$ gold price broke above

intermediate-term lateral support and a long-term trend-line. Here's the

associated chart:

And here's a chart showing the current situation:

The impressive upside breakout in the US$ gold price in Q3-1986 was

not confirmed by an upside breakout in the gold/SPX ratio and did not

indicate that a new gold bull market was underway. However, there was

still plenty of money to be made over the ensuing 12 months from owning

gold-related investments, especially gold-mining stocks.

Current Market Situation

A

gold-price correction has begun. If this is a routine pullback to address

the short-term 'overbought' condition that existed at the end of last week

then it should end at or above former resistance (now support) at $1300.

However, as stated in the latest Weekly Update:

"In previous

instances over the past 35 years when the gold price made a short-term

bottom during June-July and then rallied strongly into the first half of

September, the 50-day MA became an important demarcation level. As long as

declines did not decisively breach this MA then the rally was intact and a

move to well above the September high was in store prior to year-end,

whereas a decisive breach of this MA was a reliable signal that an

intermediate-term top was in place."

In other words, a

pullback could continue to the 50-day MA (the blue line on the following

chart) without presenting a problem to the short-term bullish case. The

50-day MA is rising and at its current rate of ascent will reach $1300

near the end of this month.

Gold Stocks

The gold-mining sector has begun

to 'correct' along with the US$ gold price.

Gold-mining

corrections within short-term upward trends typically last 4-8 trading

days. The current correction is 4 days old, which means that it may

already be at least half complete.

We don't put much emphasis on

trading volume, but we are a little concerned that the recent sharp moves

higher by gold-mining ETFs such as GDX were not accompanied by volume

surges. In fact and as illustrated by the following daily chart, GDX

volume has trended downward during the entire rally from the December-2016

low.

Perhaps this just means that the gold-mining ETFs will have to

break above their February highs to generate some enthusiasm.

US$ weakness to the rescue

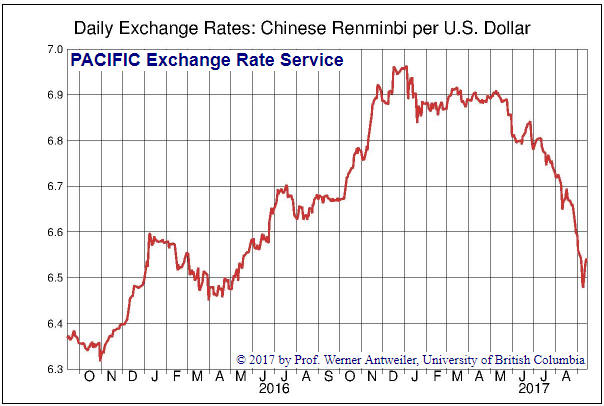

Under the weight of

its own over-valuation, the Chinese Yuan weakened relentlessly for about

18 months prior to December of last year. In doing so it created two

problems for China's government.

First, in its efforts to slow the

pace of the Yuan's depreciation China's government was rapidly 'eating up'

its foreign currency reserves to the extent that by late last year the

efforts had consumed more than 1 trillion US dollars. That still left

almost 3 trillion dollars, but at the rate the reserve pile was being

reduced there was a genuine risk that in the not-too-distant future the

government would lose its most important exchange-rate-manipulation tool.

Second, even though China's government was acting to prop-up the Yuan,

Donald Trump, due to either ignorance or a willingness to say anything to

get votes, was citing the Yuan's weakness as evidence that China's

government was attempting to gain a trade advantage at the expense of the

US. Consequently, the Yuan weakness led to a perception problem that

potentially could have been the catalyst for a US-China trade war

following Trump's election victory.

Fortunately for all concerned,

the Yuan stopped weakening at the beginning of this year and in May of

this year began to strengthen at a relatively fast pace. As illustrated by

the following chart, against the US$ it has now recouped all of last

year's loss. Note that the chart shows the number of Yuan to the US$, so a

falling line indicates a strengthening Yuan and a rising line indicates

relative weakness in the Yuan.

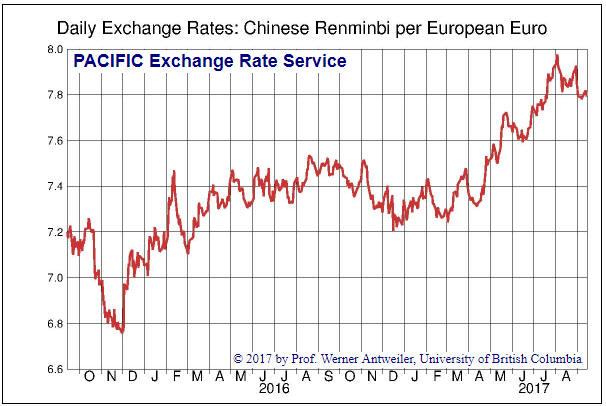

This year's strength in the Yuan relative to the US$ was not caused by

the actions of China's government. It was, instead, caused by weakness in

the US$ that had nothing to do with China. We know that this is the case

because the next chart shows that the Yuan has continued to weaken against

the euro (again, a rising line indicates relative weakness in the Yuan).

In fact, relative to the euro the Yuan is about 5% lower today than it was

at the start of this year.

China's government did not cause this year's strong rebound in the

Yuan relative to the US$, but there is no doubt that it has benefited.

First, it has not only been able to stop consuming its FX reserves, it has

also begun to replenish its reserves. This eliminates the short-term risk

that it will run out of reserves, but more importantly it results in

looser monetary conditions in China (the selling of currency reserves

takes money out of the local economy whereas the accumulation of currency

reserves injects new money into the local economy). Second, the Yuan's

strength relative to the US$ greatly reduces the threat of an all-out

trade war with the US. In fact, it creates the impression that China's

government is going out of its way to support the efforts of the new US

Administration.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() The

TSI Stocks List has short-term bearish speculations in the form of VIX

October $15 call options and Amazon (AMZN) October $800 put options. The

VIX is capable of gaining 50%-100% or more within the space of a few days,

so there is still time for the VIX call-option position to work. However,

even if we are right to interpret AMZN's price pattern as a "head and

shoulders" top (see chart below) there's now a high risk that the pattern

will take more time to complete than we have left in our October options.

For TSI record purposes we are therefore 'rolling' from the October to the

December $800 puts.

The

TSI Stocks List has short-term bearish speculations in the form of VIX

October $15 call options and Amazon (AMZN) October $800 put options. The

VIX is capable of gaining 50%-100% or more within the space of a few days,

so there is still time for the VIX call-option position to work. However,

even if we are right to interpret AMZN's price pattern as a "head and

shoulders" top (see chart below) there's now a high risk that the pattern

will take more time to complete than we have left in our October options.

For TSI record purposes we are therefore 'rolling' from the October to the

December $800 puts.

The cost of doing the 'roll' is the price paid

for the December options minus the price received for the October options.

This cost is added to the trade's original entry price to get the

new/revised entry price.

Based on the middles of Wednesday's

closing bid-offer spreads, the cost is $3.59 ($4.45 for the December puts

minus $0.86 for the October puts). This gives us a revised entry price of

$6.52 ($2.93 plus $3.59) for the AMZN put-option trade.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://fx.sauder.ubc.ca/plot.html

![]()