![]()

![]()

![]()

![]()

- Interim Update 14th June 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The FOMC announcement

had minimal effect

These days the Fed is so

concerned about not doing anything to upset the financial markets that the

outcomes of FOMC meetings tend to be very predictable. This week's meeting

was not an exception. The Fed's 14th June post-meeting announcement was in

line with almost everyone's expectations and therefore had minimal effect

on market prices.

At this week's meeting the Fed implemented

another 0.25% rate hike and mentioned its plan to gradually reduce the

size of its balance sheet by not reinvesting all the proceeds received

from maturing securities. The Fed expects the balance-sheet reduction

program to begin late this year at an initial pace of US$10B/month.

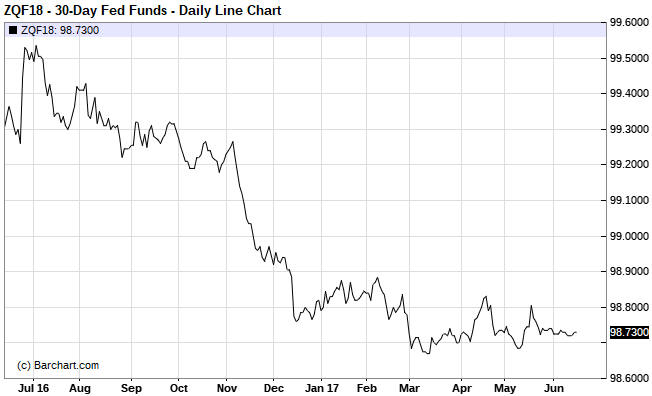

The extent to which these developments were already 'baked into the

cake' is evidenced by the following daily chart of the January-2018 Fed

Funds Futures (FFF) contract. This contract indicates the level of the Fed

Funds Rate (FFR) expected by the market near the end of this year, with

the implied interest rate being 100 minus the FFF contract price.

The chart shows that the expected FFR barely moved on Wednesday 14th June.

In fact, it has barely moved for the past three weeks. The chart also

shows that the January-2018 FFF contract has a slightly higher price now

than it did 3.5 months ago. This means that interest-rate expectations

actually edged downward during a 3.5-month period in which the Fed

implemented two rate hikes.

Before leaving this topic it's worth noting that the market's

expectations regarding the Fed's actions will have to change over the next

several months, because the current price of the January-2018 FFF contract

implies a roughly 50% chance of one more rate hike before year-end. Either

there will be a rate hike later this year or there won't be a rate hike

later this year, so at some point the market will have to move one way or

the other.

Whether or not there is one more rate hike this year

will largely be determined by the performance of the stock market. If the

stock market is strong or stable during the second half of this year then

there will definitely be another rate hike, but if the stock market

appears to be trending downward then there won't be. Furthermore, if the

stock market crashes then there not only won't be a rate hike, there will

be a rate cut.

A Fed rate hike doesn't

tighten monetary policy, but it does help the banks

As we've explained many times in

the past, a hike in the FFR no longer does anything to tighten monetary

conditions (a genuine tightening of monetary policy won't begin until the

Fed starts to shrink its balance sheet). This is because in a banking

system inundated with excess reserves there will be almost no borrowing of

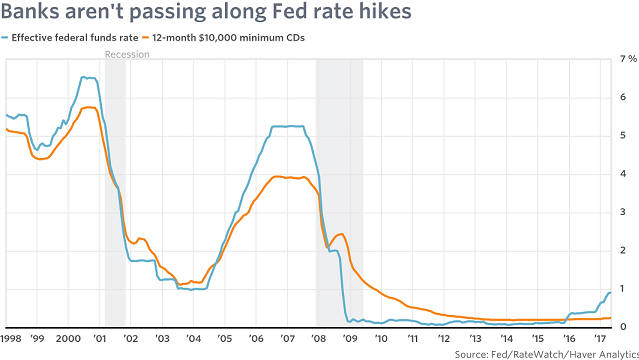

Federal Funds. However, a hike in the FFR does help the commercial banks.

One reason is that the Fed now implements its rate hikes by raising

the amount of interest it pays on bank reserves. A Fed rate hike therefore

now involves the Fed pumping more money into the banks. Another reason is

illustrated by the following chart, which is from a

Steve Goldstein article at Marketwatch.com and doesn't include

Wednesday's 0.25% boost in the FFR.

The chart shows that banks have

generally not lifted the rate of interest they pay to depositors as the

Fed has lifted the FFR. In some cases the banks have, however, used the

Fed rate hikes to justify lifting the amount they charge on loans, meaning

that the Fed rate hikes have led to higher interest margins for the banks.

The Stock Market

The US

Trying to solve the sentiment conundrum

In a

blog post early this week we reiterated the potential pitfalls in

using sentiment as a market timing tool and presented a chart showing the

Investors Intelligence (II) bull/bear ratio as an example. The chart

suggests that US stock market sentiment has been consistent with a

bull-market top for the bulk of the past four years, and yet the bull

market has persisted with only one intermediate-term correction. Even

though the chart helps to make our point, further analysis is warranted

because it is very unusual for sentiment -- when used as a contrary

indicator -- to be so wrong for so long.

We've come up with a

possible -- and, we think, plausible -- explanation for why measures of US

stock-market sentiment that worked well as contrary indicators in the past

have not been useful of late. The reason relates to the third of the

potential pitfalls outlined in the above-linked blog post. We are

referring to the following:

"...regardless of what sentiment

surveys say, there will always be a lot of bears and a lot of bulls in any

financial market. It must be this way otherwise there would be no trading

and the market would cease to function. As a consequence, if a survey

shows that almost all traders are bullish or that almost all traders are

bearish then the survey must be dealing with only a small -- and possibly

not representative -- segment of the overall market."

The

explanation we've come up with is that prior to the past few years the II

sentiment survey, which is a survey of investment advisors who regularly

publish their views via newsletters, reflected the sentiment of the

investing public, but this is not so much the case anymore. Prior to the

past few years the advisors and the general public would become

increasingly bullish or increasingly bearish together, with high levels of

optimism invariably following persistent price strength and high levels of

pessimism invariably following either persistent or dramatic price

weakness. Over the past few years, however, the perceptions of these two

groups took separate paths. Investment advisors became very optimistic in

reaction to the strong upward trend in prices, but for the most part the

general public remained unenthusiastic about the stock market.

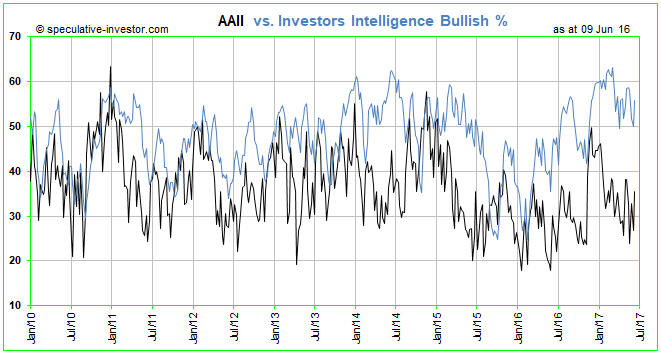

We

can illustrate the change described above by comparing the II bullish

percentage with the AAII (American Association of Individual Investors)

bullish percentage, which is what we've done on the chart displayed below.

The AAII survey is based on the opinions of retail investors, that is, the

general public.

The chart shows that prior to 2014 the II (the blue

line) and AAII (the black line) bullish percentages typically moved up and

down together within a similar range, but that from 2014 onwards the II

bullish percentage tended to be significantly higher. Furthermore, the

distance between the two survey results has increased since early this

year, with the II bullish percentage remaining above 50 and the AAII

bullish percentage spending most of its time in the 25-35 range. The most

recent results show an II bullish percent of 55.8 and an AAII bullish

percent of 35.4.

It seems that the general public's stock-market sentiment has not

reached an optimistic extreme during the current cycle. Does this mean

that there's a lot more price strength to come or does it mean that the

next major price top will happen without the general public having fully

embraced the upward trend?

We don't know, but it's definitely

possible that the public will never fully embrace the latest bullish trend

for the simple reason that it is financially incapable of doing so. Having

had its savings decimated when earlier Fed-fueled investment booms

inevitably collapsed it may not have the financial wherewithal to

enthusiastically participate in the Fed's latest venture.

Current Market Situation

There

isn't a lot happening, but what is happening is interesting and

potentially significant. In particular:

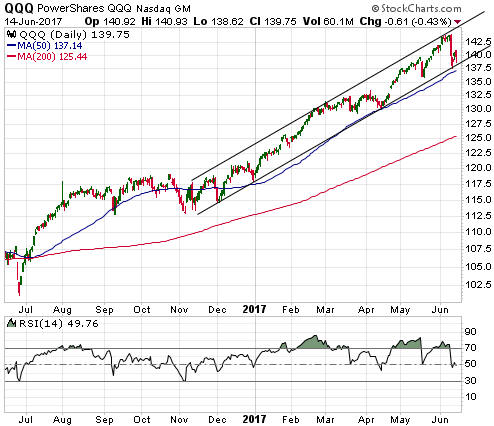

1) QQQ (the NASDAQ100 ETF),

the focal point of speculation during this year to date, has trended

upward within a well-defined channel since early-November of last year.

Last week it quickly moved from the top to the bottom of this channel, but

up until now the channel bottom has held.

If the channel bottom is

breached on a daily closing basis it will be a warning that something more

serious than a routine short-term correction is underway. We expect that

the channel bottom will soon be breached.

2) XME (the Metals and Mining ETF) broke out to the downside in

early-May and then almost immediately began to slowly work its way upward.

At this stage the upward drift of the past few weeks looks corrective (a

counter-trend move within a downward trend) and Wednesday's nearly-3%

decline has possibly signaled the resumption of the downward trend.

Support at $28.00 seems to be important. If this support is breached

we suspect that a quick decline to around $25 will follow, at which point

the post-election surge will have been fully retraced.

The Emerging Markets ETF (EEM)

EEM continues

to show remarkable resilience. We think that this resilience is mostly due

to US$ weakness and that EEM will begin to trend downward when the US$

begins to rally.

EEM will probably drop to support at $38 and could

fall as far as support at $34 within the next two months.

Gold and the Dollar

Gold

In

the latest Weekly Update we wrote that until there was a daily close below

$1260 there would remain a chance of gold making a short-lived move above

$1300. Gold still hasn't closed below $1260, but there is now a high

probability that it double-topped near $1300 last week.

We think

that gold's short-term risk/reward is bearish, but we don't have any

specific short-term price targets in mind at this time.

Gold Stocks

In the latest Weekly Update, we

wrote:

"Unless GDX closes above $23.86 it will be prudent to

assume that the rebound from the early-May low ended on Tuesday 6th June

and that a significant decline has begun. For those with the requisite

experience and inclination it could also be prudent to view strength in

the early part of this week as an opportunity to hedge long positions in

gold-mining stocks. The hedges (for example, GDX put options) could then

be exited at a loss if GDX subsequently closes above $23.86 or at a profit

if GDX suffers a quick and sizable decline."

The following

charts show that GDX and the HUI fell sharply on Wednesday 14th June. The

Fed's announcement was the catalyst, but Wednesday's price action was

really just the continuation of a pattern that began months ago.

The March-May double bottom ($21 for GDX, 180 for the HUI) may soon be

tested.

The declines in the gold-mining indices and ETFs are probably not yet

close to complete, but junior gold-mining stocks that get hit hard by the

infamous GDXJ rebalance could bottom as soon as this Friday.

During

the first two trading days of this week there were no signs of the

substantial buying and selling that will have to be done by GDXJ to bring

itself into line with the index it is supposed to track, in that trading

volumes in the affected stocks were no higher than average and price

movements were generally not significant. However, the GDXJ effect started

to become apparent on Wednesday 14th June, with some gold-mining stocks

taking relatively big price hits on relatively high volumes.

The

GDXJ effect will probably increase over the final two trading days of this

week, although it's worth noting that when it comes to matching the ETF

with its underlying index the managers of the ETF have considerable

leeway. Rather than bringing the ETF into line with the associated index's

new component weightings by the close of trading this Friday, which is

when the new weightings take effect, they could, for example, decide to

gradually implement the required changes over the next several weeks.

If the required weighting changes are implemented prior to the end of

this week then we may soon be presented with good short-term buying

opportunities in individual gold stocks as outlined in the latest Weekly

Update.

The Currency Market

On a daily

closing basis the Dollar Index (DX) went nowhere during the 14th June

trading session, but the intra-day price action was significant. We are

referring to the fact that the DX spiked to a marginal new low for the

year and then recovered to be roughly unchanged on the day.

It must

now achieve a daily close above 97.5 to signal that a

potentially-important reversal has taken place.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Exiting

Cordoba Resources (CDB.V)

Exiting

Cordoba Resources (CDB.V)

Cordoba Resources (CDB.V)

announced that ownership of its San Matias copper-gold project in Colombia

will be restructured.

The current (pre-restructure) situation is

that 1) Robert Friedland's High Power Exploration (HPX) has earned a 51%

stake in the project, 2) to increase its stake to 65% HPX is obligated to

pay all costs to take the Alacran deposit (the most advanced part of the

district-scale project) through to the completion of an FS, and 3) due to

HPX's 36% ownership of CDB its total ownership of San Matias is

effectively 69% (the 51% direct stake plus an indirect stake via ownership

of CDB).

The restructuring involves CDB issuing 105M shares to HPX

in exchange for HPX's stake in the project and reimbursing HPX for

expenditure incurred since the 51% level was reached (92.7M shares for the

51% stake plus 12.3M shares for the expenditure reimbursement). This will

result in CDB owning 100% of the project and HPX owning 69% of CDB,

meaning that HPX's effective ownership of San Matias will remain the same.

The restructuring also involves CDB raising C$10M via a private placement

at C$0.81/share.

We estimate that CDB will have about 206M shares

outstanding and about C$8M of cash after the restructuring is complete.

Although this deal will have no effect on HPX's current effective

ownership of San Matias it significantly reduces HPX's future financial

commitment to the project, as the cost to HPX of taking the project

through the feasibility stage would have been high. For HPX it therefore

reduces risk while keeping most of the exposure to the upside. By the same

token, it increases the risk being borne by CDB's shareholders while not

significantly increasing their upside exposure. In other words, it's a

better deal for HPX than CDB. Furthermore, the pace of progress is likely

to slow now that CDB will be fully funding the progress.

Due to the

worsened risk/reward for CDB shareholders we are removing CDB from the TSI

Stocks List.

Just to be clear, the CDB story hasn't suddenly become

substantially less bullish, but from our perspective an important part of

the story was that project exploration/engineering would be driven and

fully funded by HPX to the point where there was a completed FS. With that

part of the story having been erased we no longer find the stock

sufficiently attractive.

CDB was added to the TSI List at C$0.77

only three weeks ago. Its most recent price was C$0.90, but it has been

halted since the HPX deal was announced on Tuesday afternoon. We don't

know when the trading halt will be removed, but when it is the stock will

likely trade well below the aforementioned C$0.90 level.

It

doesn't make sense to sell this stock at any old price, since the

potential value of the San Matias project hasn't changed. We therefore

wouldn't sell below C$0.80.

For TSI record purposes the stock will

be exited when it next trades at C$0.80 or higher.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.barchart.com/

![]()