![]()

![]()

![]()

![]()

- Interim Update 15th February 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The Philippines is off

limits to mining investors

Strict environmental regulations

shouldn't be a major problem/risk for mining companies provided that the

regulations are very clear and are consistently applied. Unfortunately,

the regulations are often not clear and/or not applied with consistency.

Instead, whether a mine or a proposed mine is deemed to comply with the

government's environmental requirements often comes down to the subjective

or arbitrary assessment of a bureaucrat or politician. This has certainly

been the case of late in the Philippines, with Regina Lopez, the

Environment and Natural Resources Secretary, ordering the closure of 23 of

the country's 41 mines and halting the development of many other mines.

Some of the mines that have recently been shut down in the

Philippines probably deserved it, but the Secretary appears to be an

environmental crusader who has adopted a 'shut down first ask questions

later' approach to the mining industry. The result is that for the time

being there is far too much uncertainty regarding the ability to obtain

and maintain the necessary environmental permits to warrant making any

mining-related investments in the Philippines.

Therefore and with

one exception, until/unless there is a substantial change in the political

situation we will not consider buying the shares of any mining company

focused on the Philippines. The one exception will be when we can

effectively get a company's Philippine assets for free, meaning that the

company is being valued by the stock market for less than its cash.

The Stock Market

The US

Sentiment Extreme

Market Vane's

bullish percentage for the NASDAQ100 (the percentage of traders surveyed

by Market Vane who describe themselves as bullish on the NASDAQ100 Index)

has reached 90. Our Market Vane data only go back 13 years, so it's

possible that higher readings were achieved in the lead-up to the

March-2000 bubble top. However, 90% is the highest reading of the past 13

years. It is most definitely 'extreme'.

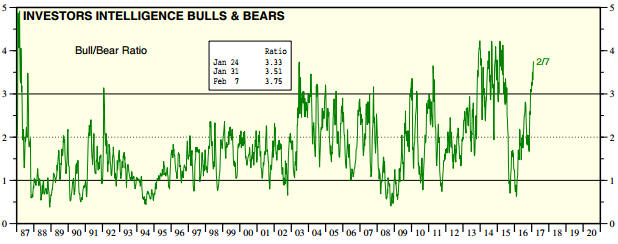

The following chart is

based on the Investors Intelligence sentiment survey and shows that the

bull/bear ratio (the percentage of bullish advisors divided by the

percentage of bearish advisors) is now also at an extreme. It got a little

higher during 2014 and the first half of 2015, but apart from that it

hasn't been above its current level since 1987.

Chart Source: Yardeni.com

After the bull/bear ratio reached its current extreme level in 2014,

nothing dramatically bearish happened to the stock market. There were

pullbacks of a few percent in the S&P500 Index (SPX), but the

intermediate-term upward trend continued. However, when the bull/bear

ratio reached its current level during the first half of 2015 the market

was close to an intermediate-term peak.

The most important

difference between the bull/bear extremes of 2014 and the bull/bear

extreme of 2015 is that market internals were weaker during the latter

period. The bearish divergence between the SPX and market internals that

began to develop in early-December of last year makes the current

situation more like the second quarter of 2015 (within three months of the

start of an intermediate-term decline) than any time in 2014.

Also

worth mentioning is that the average valuation is higher today than it was

at the intermediate-term peak of 2015 and the bull market is now about 18

months older.

Does this mean that the downside potential is at

least as high today as it was during the months just prior to the dramatic

decline of July-August 2015?

Yes, it does. It won't surprise us if

the market maintains an upward bias into March, perhaps spurred on by the

anticipation of and reaction to Trump's "phenomenal" tax plan. There's

even a chance of an upside blow-off, or, to put it more accurately, an

extension to the current upside blow-off, within the next few weeks. But

with or without an additional near-term surge to the upside, we suspect

that the SPX will trade 10% below its current level before the middle of

the year.

In recognition of the sentiment extreme, the

bearishly-diverging market internals, the absurdly high average valuation

and the unusually-low volatility, we are now intermediate-term bearish on

the US stock market.

Despite their more attractive valuations, due

to the US stock market's global influence we are also becoming

increasingly concerned about downside risk in most other stock markets

around the world. We would like to buy into some of these other markets

(the Japanese market, for example) but expect that opportunities to do so

at significantly lower prices will arrive during the second and/or third

quarters of this year.

Current Market

Situation

The following daily chart shows that the current

short-term rally in the NASDAQ100 Index (NDX) has accelerated to a

sufficient degree to take the index above the top of the channel that

capped last year's short-term rallies. This suggests that an upside

blow-off is in progress.

The next chart shows the performance of the Volatility Index (VIX)

over the past 20 years. The VIX probably bottomed near a 20-year low at

the beginning of this month and greater volatility probably lies in store

regardless of whether the senior indices are close to important peaks.

Risk-tolerant speculators could reasonably consider buying VIX call

options expiring in April or May in anticipation of the VIX spiking up to

at least 15-20 within the coming two months.

It's possible that the senior US stock indices will make

intermediate-term tops (highs that hold for more than 6 months) as early

as this week. Be aware, however, that important tops in the US stock

market almost always involve at least one test of the high and often

encompass a sequence of marginal new highs separated by pullbacks of a few

percent. Therefore, rather than an intermediate-term decline beginning

from whatever high is made over the next few days there's a higher

probability of a pullback followed by a rise to test or marginally exceed

whatever high is made in the near future.

Our new bearish outlook

reflects the perception that intermediate-term downside risk is now much

greater than any remaining upside potential and that an intermediate-term

top will probably be put in place within the coming two months.

Gold and the Dollar

Gold

At

this time last week the gold price had broken solidly above resistance at

$1220 and was within about $20 of its 200-day MA (our short-term upside

target). The market was also slightly 'overbought', suggesting that some

sort of price peak would soon be put in place -- possibly after a quick

move up to the 200-day MA.

Since then, very little has happened.

The gold price hasn't been able to extend its advance, but on a daily

closing basis it has remained above the $1220 short-term breakout level.

It therefore still stands a decent chance of reaching its 200-day MA

before a significant correction gets underway.

Based on the price

action of the past three weeks we think that the 20-day MA (the black line

on the following chart), which is presently at $1216, can now be used as a

short-term demarcation level. We are referring to the fact that this

moving average has been acting as support.

What we mean by

"demarcation level" in this case is that the benefit of the doubt should

be given to the short-term bullish scenario as long as the gold price does

not close below its 20-day MA. If the gold price does close below its

20-day MA then it will be prudent to assume that a significant downward

correction has begun.

Gold Stocks

Like gold bullion, the HUI has

essentially marked time over the past 5 trading days and appears to be

'respecting' its 20-day MA (the black line on the following chart).

Consequently, as is the case with gold it makes sense at this time to use

the 20-day MA as a short-term demarcation level for the HUI.

The

HUI's 20-day MA is slightly above 210, a level where there is also some

lateral support. Therefore, the benefit of the doubt should be given to

the short-term bullish scenario as long as the HUI does not close below

210.

The Currency Market

The current annual rate of

increase in Germany's CPI is 1.9% and the trend is up. The rate of

increase will probably rise above 2% this quarter. At the same time, the

following chart shows that the yield-to-maturity on the 2-year bonds

issued by the German government has recently plunged to negative 0.8%. The

implication is that the real yield on German 2-year government bonds is

presently about MINUS 2.7%. Who would buy such a bond?

The answer is the Bundesbank (Germany's central bank). As part of the

ECB's brilliant strategy the Bundesbank is obligated to buy a certain

quantity of 2-year German government bonds each month, regardless of

price. The price is now so high (the yield is now so low) because previous

official-sector buying has created a shortage.

The plunge in German

interest rates over the past couple of weeks is the main source of the

recent downward pressure on the euro. The euro has been pushed a little

below its 50-day MA, but Wednesday's upward reversal keeps alive the

possibility of a rise to 109.5-110.0 before the bear market resumes.

While the euro closed slightly below its 50-day MA on both Tuesday and

Wednesday of this week, the Dollar Index has not yet been able to close

above its 50-day MA. In early trading on Wednesday it looked almost

certain that a daily close by the Dollar Index above its 50-day MA was

going to happen, but a reversal occurred and the moving-average resistance

held.

This keeps alive the possibility of a fall to 97.5 before the

bull market resumes.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Exiting

the Global X Uranium ETF (URA). Recent price: US$18.43

Exiting

the Global X Uranium ETF (URA). Recent price: US$18.43

URA

is an ETF that holds uranium-mining stocks and has been in the TSI Stocks

List since July-2015.

A few weeks ago we wrote that URA would be

removed from the TSI List if it moved up to US$19.00, mainly due to our

concern that the uranium-mining sector was a long way ahead of the

underlying commodity market. It traded above $19 on both Tuesday and

Wednesday of this week before reversing downward on Wednesday. It has now

been removed from the TSI List, using Wednesday's closing price of $18.43

for record purposes.

URA is only up by about 10% since its addition

to the List but is up by about 40% since the beginning of this year and

almost 70% since its November-2016 bottom.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.bloomberg.com/

![]()