![]()

![]()

![]()

![]()

- Interim Update 15th July 2015

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The Greek Deal

The framework of an eventual

deal between the Greek government and its major creditors has been agreed, but

the situation remains 'fluid'. Many pieces, including various parliamentary

approvals* and additional ELA (Emergency Liquidity Assistance) from the ECB,

must fall into place over the days ahead to transform the preliminary agreement

into a deal that enables Greek banks to resume semi-normal operations and the

Greek government to temporarily meet its financial obligations. And even if a

deal is soon finalised, the article posted

HERE explains that Greece's banks and government will still be in precarious

positions.

Incredibly, the deal that Greece's Prime Minister accepted at the start of this

week is worse than the deal that was on the table prior to the preceding week's

referendum and that was definitively rejected in the referendum. This tells us

that Greece's government was not prepared to leave the euro-zone whereas the

other side of the negotiation was prepared for such an outcome. If you want to

get a favourable, or at least a reasonable, outcome in any negotiation you

generally must have walk-away power (the ability/willingness to walk away if the

other party refuses to move far enough in your direction). It seems that

Greece's creditors had walk-away power (meaning: the EU's political and monetary

leadership was prepared to accept the consequences of a

multi-hundred-billion-dollar debt write-off and "Grexit"), but Greece's

government did not.

Regardless of whether or not the deal between Greece and its creditors is put to

bed over the days/weeks immediately ahead, it's unlikely that Alexis Tsipras and

his Syriza Party will maintain control of Greece's government for much longer.

Also, the fact that the EU's leadership was prepared to let Greece go -- or

perhaps even encourage Greece to go, considering the onerous terms on which it

ended up insisting -- demonstrates that EZ membership is reversible. This is

important because it means that whenever a euro-zone government gets into dire

financial straits in the future, the financial issue will potentially turn into

an EZ membership issue.

*The Greek parliament approved the deal on Wednesday 15th

July and the German parliament is scheduled to vote on the deal on Friday 17th

July.

An Iran deal and a

possible oil bottom

The US and the other

P5+1 countries reached an

agreement with Iran on Tuesday 14th July aimed at preventing the Islamic

republic from building a nuclear weapon in return for the lifting of economic

sanctions. From a global perspective this is vastly more important than the deal

between Greece and its creditors, because it makes the world a safer place.

The nuclear agreement with Iran doesn't make the world a safer place by

curtailing Iran's nuclear-weapon-building ambitions, since those ambitions were

non-existent to begin with. At least, the International Atomic Energy Agency (IAEA)

has

come up with no evidence over the past 10 years to suggest that any such

ambition existed*. Rather, it makes the world a safer place by restraining the

ambitions of the US War Party -- the influential group of Republicans and

Democrats within the US government that is continually trying to justify

increased US military presence or outright military conflict in some part of the

world.

Of much lesser consequence, the nuclear agreement with Iran MIGHT have resulted

in a correction low for the oil price. In a classic sell-the-rumour-buy-the-news

situation, the oil market sold off over the preceding two weeks in anticipation

of the nuclear agreement and the increase in Iran's oil exports that will

eventually stem from the agreement, and then failed to make a new low for the

move after the news of a completed agreement hit the wires.

We emphasised the word "might" because there isn't yet any evidence, aside from

the oil price holding above last week's low in reaction to this week's news,

that a correction low is in place. A weekly close above the 10-week and 40-week

MAs (the blue and black lines on the following chart) would be clear-cut

evidence of a short-term price bottom and resumption of the intermediate-term

rally that began in March. Both of these MAs are currently around $58 and

declining.

*The agreement is comprehensive and blocks every possible

path to a nuclear weapon. It was relatively easy for Iran's current leadership

to agree to such stringent terms because it didn't want to go down such a path

in the first place. That being said, the Iranian government is far from 'squeaky

clean'. Like the US government, it has provided assistance to unsavoury groups

as part of efforts to expand its influence in the Middle East.

The Stock Market

The following chart shows the

horizontal range in which the S&P500 Index (SPX) has oscillated over the past

5.5 months. It dropped to near the bottom of this range last week and has since

rebounded to within 1% of the top.

The SPX is not yet short-term 'overbought', so it could certainly make a new

high within the coming two weeks. However, we suspect that if a break to a new

high were to happen in the near future it would not be followed by significant

additional gains.

In the US stock market there is still a lot more downside risk than upside

potential in both the short-term and the intermediate-term.

Gold and the Dollar

Gold

The fundamental argument for the coming gold rally

We don't want to create the impression that a sizable gold rally over the next

several months is inevitable, because it isn't. There is, in fact, a realistic

scenario under which the gold market will continue to languish. We are referring

to the possibility that inflation expectations and nominal interest rates remain

near their current levels while the US stock market (as represented by the

S&P500) breaks out to the upside and resumes its multi-year upward trend.

However, we view this as the third most likely scenario. Under the two most

likely intermediate-term outcomes there would be a significant rise in the US$

gold price and a substantial rise in the gold-mining sector.

Here, in brief, are descriptions of the two most likely intermediate-term

scenarios:

1) The US stock market made a long-term top during May-June and will gradually

roll over to the downside over the reminder of this year -- via a sequence of

lower highs and lower lows -- before accelerating downward in 2016. Under this

scenario, evidence will emerge within the next few months that the US economy is

entering a recession. Also, the Fed will hike its targeted interest rate no more

than once (in September) and by the final quarter will be talking more about

providing additional monetary accommodation than about 'normalising' monetary

policy. Due to the lacklustre stock market and the nascent signs of recession,

real US Treasury yields will decline and the yields on low-quality (junk) bonds

will rise.

2) The cyclical bull market in US equities will continue for up to another year,

with the final 6-12 months being characterised by rising inflation expectations

and a shift towards commodity-related investments. This scenario is supported by

the ECB's foolhardy attempts to promote economic growth via rapid monetary

inflation and by the China government's increasingly-desperate attempts to

create new bubbles to temporarily mitigate the undesirable consequences of

previous bubbles. Under this scenario the Fed will probably hike its targeted

interest rate twice before year-end and will continue hiking in 2016, but real

interest rates will fall due to rising inflation expectations.

In the first of these scenarios the intermediate-term gold rally would be the

initial leg of a new cyclical bull market, whereas in the second scenario the

intermediate-term gold rally would probably turn out to be a bear-market

rebound. However, from a practical speculation standpoint it makes no difference

whether a large multi-quarter rally is part of a bull market or a bear market.

A few months ago we favoured the first of these scenarios, but the probability

of the second scenario has risen to the point where they now appear to have

roughly equal chances. The probability of the second scenario has increased due

to a) the resilience shown by the S&P500 and some other important US stock

indices in the face of a fear-laden news backdrop over the past few weeks, b)

the fact that the most reliable leading indicators of US recession are still

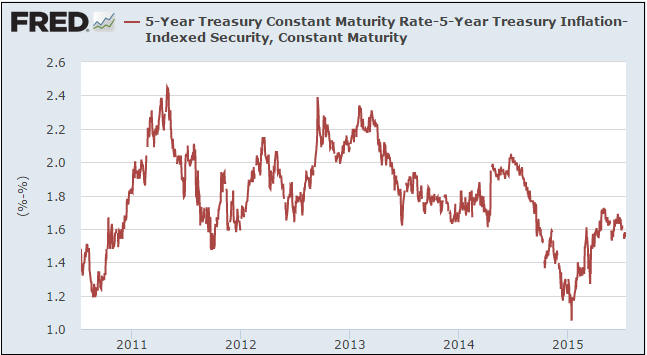

signaling "no recession imminent", and c) the 5-year "Expected CPI" holding onto

the bulk of its January-May gain (refer to the first of the following charts)

despite news that would superficially support deflation forecasts. Note, though,

that this scenario is not yet being supported by an upward reversal in the EEM/SPY

ratio (refer to the second of the following charts). Based on the historical

record, the EEM/SPY ratio is likely to make a sustained turn to the upside

before a similar turn in the CRB Index.

Current Market Situation

The US$ gold price spiked to a new multi-month low and tested its March low on

Wednesday 15th July. Also, the euro gold price is now very close to its 200-day

MA, which is roughly the level at which the intermediate-term correction that

began in January was expected to end.

The stage is set for an important bottom. However, a quick spike below the

March-2015 and November-2014 lows to the bottom edge of gold's 2-year wedge

(around $1130) remains a realistic near-term prospect, especially considering

the continuing relative weakness in the gold-mining indices.

Gold Stocks

The relentless weakness in the gold-mining indices is difficult to explain. It

can only be due to a sense of hopelessness on the part of those who are already

involved on the long side and complete disinterest on the part of everyone else.

With the Greek deal, the Iran deal, the temporary abating of China's

stock-market meltdown and the rebounds in equities around the world, the news

and financial-market backdrops have recently been more bearish for gold than for

gold-mining stocks. However, it's the gold-mining sector that has taken the

brunt of the negativity, despite it being very 'oversold' relative to gold. Gold

bullion has actually held up remarkably well.

When the gold-mining sector is as 'oversold' as it is right now, the beginning

of a multi-month rally is typically marked by an explosion in the form of 2 or 3

big up-days. This means that we should get clear evidence of a bottom very soon

after it happens.

As previously advised, short-term speculators should wait for evidence of a

bottom before taking long positions. As also previously advised, the HUI's

20-day MA (the black line on the following chart) can be viewed as a bar that

must be stepped over to generate the necessary evidence. Fortunately, the bar is

being lowered with each passing day.

Long-term speculators should accumulate positions in the highest-quality junior

and mid-tier gold miners as opportunities arise, perhaps via the use of

under-the-market buy orders designed to take advantage of downward spikes.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://research.stlouisfed.org/

![]()