![]()

![]()

![]()

![]()

- Interim Update 15th July 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Commodities

Oil is still threatening

to break out

To date, the post-crash rebound high for the

S&P500 Index (SPX) occurred in early-June. Since then the SPX has 'chopped

around' within a narrow range bounded on the upper side by its early-June

high. Not coincidentally (since the markets are linked), it has been a

similar story for the oil price. As illustrated below, the oil price

essentially has traded sideways since hitting a post-crash rebound high in

early-June. Furthermore, the six weeks of sideways trading has taken place

slightly below long-term resistance/support at $42.

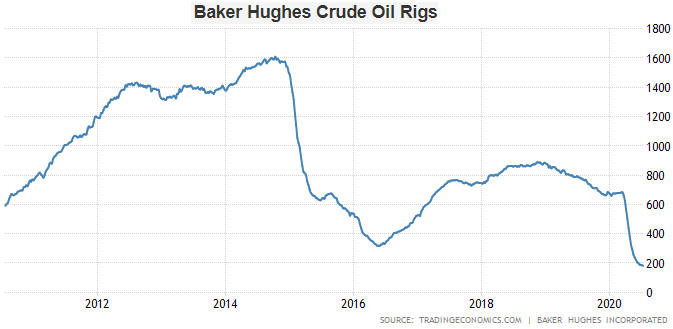

Despite the big rebound in the oil price from its April trough, the

following chart shows that the number of operating oil rigs in the US has

continued to shrink and made a new 10-year low last week. We've shown this

rig-count chart numerous times over the past two months, because it is an

important piece of the intermediate-term oil market puzzle.

The on-going decline in the US rig count reflects the fact that even

though the oil price is a long way above where it was 2-4 months ago, it

is still too low to cover the costs of most US-based oil producers. The

implications are that the downward trend in production will continue and

that there will have to be a significant additional gain in the oil price.

We have been expecting that the "significant additional gain" would

wait until the final quarter of this year or the first half of next year

(we have written that the oil price probably will trade at least as high

as the $60s during the first half of 2021). Also, we have been expecting

that the next $5-$10 move in the oil price would be to the downside.

However, to get an oil price correction of that magnitude there probably

will have to be a decline in the SPX to well below 3000. If there isn't a

meaningful SPX correction within the next few weeks, then it's likely that

the oil price will make a sustained break above resistance at $42 a few

months sooner than expected.

The uranium correction is

complete

A week ago, we wrote: "There will be room for

uncertainty until CCJ [Cameco] makes a solid break above US$11.00, but

over the first two days of this week the probability increased that the

correction is complete. If it is complete then resistance at US$13 is a

logical short-term target."

On Wednesday 15th July CCJ made a

solid break above US$11.00. Therefore, we pronounce the correction

"complete".

If Wednesday's upside breakout is genuine then over

the next few weeks CCJ should either move directly to resistance at

US$13.00 or pull back to test this week's breakout before moving up to

resistance at US$13.00.

CCJ is the lead dog in the uranium mining sector, so if CCJ has

resumed its bull market then most other uranium stocks should follow. This

includes Energy Fuels (UUUU, EFR.TO), the US-based junior uranium producer

that was added to the TSI List last week. UUUU is yet to move and remains

at a reasonable level for new buying.

For UUUU, a daily close above

US$1.70 would signal the resumption of the intermediate-term bullish

trend.

T-Bond Update

The following chart shows that

the T-Bond price has drifted sideways-to-lower since peaking in March. We

suspect that the March-2020 high will prove to be the long-term variety,

but the price action leaves the door open to a final surge to a new high.

If a final surge to a new high is going to happen it will have to

happen soon. The reasons are:

1) The lockdowns did substantial

long-term damage to the goods-and-services supply side, while massive

government spending programs are preventing an equivalent fall-off in

demand. As a result, for many 'things' the monetary demand will increase

relative to the supply, leading to higher consumer prices and the

emergence of a general "inflation" problem. We doubt that the "inflation"

problem will become obvious prior to 2021, but the bond market should

begin to 'sniff out' the problem well before it becomes obvious.

2)

The following chart shows that there is a positive correlation between the

T-Bond price and the gold/commodity ratio, with commodities represented on

the chart by GNX. It very much looks like the gold/commodity ratio made an

intermediate-term peak in April-2020, so the time is running out for the

T-Bond to make an equivalent peak if it hasn't done so already.

The Stock Market

The stock market was given a

boost over the past two trading days by a vaccine story. Getting a

COVID-19 vaccine is important for the economy, but even if one or more of

the companies that is trying to develop a vaccine is successful in the

near future the widespread distribution of the drug won't happen until

next year. Moreover, when it does happen the businesses and jobs that were

destroyed by the lockdowns won't magically return. Many of these business

and jobs are gone for good. This is a reality that the US stock market

will have to deal with at some point, but probably not until 2021. In the

meantime, there is an uncomfortably high risk of a sizable correction in

the 'market darlings', but not a major broad-based decline.

The

'market darlings' are represented by the NASDAQ100 Index (NDX), a daily

chart of which is displayed below. The chart shows that there was a

potentially significant reversal on Monday of this week, with the index

first surging to a new all-time high and then ending the day with a loss.

At this stage there is no evidence that anything more than a multi-day top

was set on Monday, but a daily close below the 20-day MA before the end of

this week would be evidence that at least a multi-week top is in place.

Interestingly, some of the more depressed parts of the market

benefited from the NDX's downward reversal. Two examples are shown below.

The first example is the small-cap end of the market as represented by the

Russell2000 ETF (IWM). IWM successfully tested its 50-day MA last week and

has just closed above its 200-day MA for the first time in more than one

month. The second example is the oil services sector, as represented by

OIH. OIH fell by about 35% from its early-June high to last week's low,

but on Wednesday of this week it closed above its 50-day MA and at a

3-week high.

It's too soon to know, but what we've witnessed over the past three

trading days could be the start of a rotation from the recent focal points

of speculation (TSLA, AMZN, etc.) to sectors/stocks that have experienced

meaningful corrections over the past six weeks.

A rotation within

the market over the next several weeks is the most plausible bullish

alternative to the market-wide short-term correction we've been expecting.

Such an outcome would be a ramification of the hugely-disparate

performances of different parts of the market over the past month.

The upshot is that IF the NDX elevates the significance of Monday's

downward reversal by closing below its 20-day MA within the coming few

days, it will signal that either 1) a general market downturn has begun,

with the relatively strong stocks/sectors joining the relatively weak

stocks/sectors in correction mode, or 2) investment/speculative demand is

shifting from the stocks/sectors that have been relatively strong to those

that have been relatively weak. In both cases the S&P500 Index wouldn't

make much headway over the weeks ahead and in the first case the S&P500

Index probably would lose more than 10%.

The potential for an

intra-market rotation has prompted us to add a trading position to the TSI

List (refer to the "Updates on Stock Selections" section below), but this

is not a time to be aggressive from either the long side or the short

side. The market could prove challenging for both bulls and bears in the

lead-up to the election in November, with a tradable rally getting

underway after the election -- regardless of the election result -- due to

the expectation that a multi-trillion-dollar infrastructure spending

program will be approved early next year.

Gold and the Dollar

Gold

The

US$ gold price spent the past five trading days consolidating slightly

below last week's high.

Although it would negate the recent breaks above the April high and

$1800, a pullback to the mid-$1700s would be perfectly normal at this

point and would not signal an end to the short-term upward trend. We are

not saying that we expect such a pullback, only that it could happen and

would not indicate a trend reversal. A solid weekly close below $1750

would, however, warn that a short-term trend reversal (from up to down)

had occurred.

Our view is that gold's short-term upward trend is

intact and that a multi-month top is not yet in place.

Gold

Stocks

The September Cycle

Over the past five years the gold mining sector has shown a strong

tendency to make its high or its low for the year in early-September.

Specifically, early-September ushered in the low for the year in 2015, the

high for the year in 2017, the low for the year in 2018 and the high for

the year in 2019. Moreover, the 2016 high is consistent with this cyclical

tendency if we widen the turning point window to cover the period from

early-August to early-September. In other words, the period from

early-August through to early-September ushered in the annual high or the

annual low in each of the past five years.

Using GDX as our proxy

for the gold mining sector, the vertical red lines on the following weekly

chart mark the aforementioned August-September turning points.

If we are going to get another August-September turning point this

year it almost certainly will be a turn from up to down.

The

cyclicality outlined above is something to be aware of IF the gold stock

indices/ETFs extend their short-term upward trends into August. Something

else to be aware of is that a minor correction over the coming 1-2 weeks,

with "minor" meaning a decline that holds at/above the 50-day MA, probably

would extend the short-term upward trend to early-September, whereas a

straight-up move from here would increase the probability of an important

turning point (from up to down) in August.

Note that even if the

August-September cycle works again this year and GDX makes its high for

the year within the next two months, in the absence of a major fundamental

shift we will continue to anticipate new multi-year highs during the first

half of 2021.

Current Market Situation

In the latest Weekly Update and last week's Interim Update we guessed

that the HUI was close to a top that would be followed by a pullback to

either the 20-day MA or the 50-day MA, after which the upward trend would

resume.

The following daily chart shows that the HUI made its most

recent peak 5-6 trading days ago, so a pullback to as low as the 50-day MA

could be underway. As mentioned above in the "September Cycle" discussion,

a correction at this point that holds at/above the 50-day MA should have

the effect of extending the short-term upward trend to early-September.

The Currency Market

The weakening trend for

the US$ that began in March-2020 probably will extend well into next year.

The drivers will be an exploding US budget deficit, massive US monetary

inflation, the combination of supply disruptions and aggressive government

efforts to prop-up demand resulting in much higher traditional "inflation"

than has been seen over the past few decades, and the US stock market

becoming a global laggard. However, it won't weaken in a straight line.

Major currency trends take a long time to get going, but once they

begin they are relentless. Confirmation that the Dollar Index (DX) has

commenced a major downward trend requires a monthly close below the

March-2020 low of 94.5, but before that happens there could be at least a

few months of choppy trading in the 94.5-98.5 range.

The DX

currently is testing its early-June low. It is not yet 'oversold' and

therefore the current decline could extend to the March low, but, as

mentioned above, we expect the March low to hold for now.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() New

trading position: Enable Midstream Partners (ENBL). Recent price: US$4.38

New

trading position: Enable Midstream Partners (ENBL). Recent price: US$4.38

ENBL builds and operates natural gas (NG) processing facilities and

pipelines in the US. It is a Master Limited Partnership (MLP), which

means, in effect, that almost all pre-tax income is transferred to

unitholders in the form of distributions and only taxed at the unitholder

level.

ENBL was a successful TSI trade from around the middle of

March until it was stopped out during the first half of June. At the time

it was stopped out we wrote that we would look for an opportunity to

return it to the List. That opportunity has arrived. Although there is no

evidence that the stock has ended its correction, the pullback from the

early-June high near US$7.00 to this week's low near US$4.00 has

substantially reduced the risk.

The stock is supported by a

US$0.16525/quarter distribution, giving it a current yield of about 15%.

Furthermore, there's a good chance that the quarterly distribution will be

increased within the next 12 months, although we are not viewing ENBL as a

long-term position.

For TSI record purposes we will set a 20%

trailing stop loss on this position.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://tradingeconomics.com/

![]()