![]()

![]()

![]()

![]()

- Interim Update 15th August 2018

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Brief comment on oil

In the latest Weekly Update we

explained why it was time to bet against the oil price. We concluded:

"...it could make sense for speculators to take a bearish oil

position. As mentioned at the start of this discussion a better entry

point would be established by a near-term rebound to $70-$71, but if the

position is being averaged into the timing of the initial foray won't be

critical.

We caution that it is always risky to bet against oil by

purchasing a leveraged bear fund or shorting the futures. The reason is

that this is a market that can always rocket higher in reaction to 'out of

the blue' news such as a 'blow-up' in the Middle East. A protective stop

may not help in such a situation.

We will be making the bet in our

own account by purchasing USO January-2019 put options, and we possibly

will add a USO January-2019 put option to the TSI List if the oil price

rebounds to around $70 in the near future."

We have taken an

initial position (no more than half the planned full position) in the

aforementioned USO puts in our own account and are hoping that a rebound

will provide a good opportunity to add to the position. Even though the

oil price broke below its channel bottom on Wednesday 15th August (see

below) there is a decent chance that the 200-day MA, which is only $0.20

from Wednesday's low, will limit the initial decline and that the price

will rebound to near the 50-day MA (currently at $68.77) before a larger

decline gets underway.

Another potential

cobalt speculation

An interesting article about

cobalt and a particular cobalt stock was

posted at Stock Gumshoe early this week. The article delves into a

recent cobalt promotion by Casey Research -- a promotion in which cobalt

is seductively referred to as a miracle energy source called "Brandt Oil".

Here are a couple of excerpts from the above-linked article:

"..."Brandt

Oil" must be cobalt... a relatively rare metal that is used, among other

things, as a cathode in lithium-ion batteries, mostly to make them safer

(controlling oxygen production, which is a fire hazard) and more durable

while degrading relatively slowly.

There are lots of different

battery chemistries, and plenty of materials science work is being done to

make it possible to use something other than cobalt (or to use less

cobalt) in vehicle batteries, but breakthroughs appear to be fairly slow

in this space. If you want a fairly plain-language explanation of why

cobalt is important in a lithium ion battery, I found

this one pretty useful."

And:

"...Cobalt is

not a miracle fuel, but it is an essential component in modern

rechargeable batteries, and (arguably) will remain so for a long time...

and it's in relatively short supply. Most cobalt comes from nickel and

copper mines, so if nickel or copper see low prices the production of

cobalt also slumps, and almost 2/3 of the current global cobalt supply

comes from one of the countries that most multinational companies don't

particularly want to be associated with, at least in the public eye: The

Democratic Republic of the Congo (DRC).

So that's the situation,

just to catch you up -- most electric vehicle forecasters believe that we

need a much larger supply of cobalt than is currently being mined, and a

lot of production comes from a place that brings to mind the "conflict

diamonds" of Angola a decade or two ago."

Stock Gumshoe

concludes that eCobalt Solutions (ECS.TO) is the cobalt stock being teased

in the Casey promotion.

We took a cursory look at ECS late last

year and decided that it didn't offer sufficient value to warrant a

mention at TSI or the addition to our own account. We then watched with

amazement and a little annoyance as the price of this stock rapidly

doubled.

As illustrated by the chart displayed below, ECS has since

come back to earth. This and the likelihood that the stock will continue

to receive more than its fair share of newsletter promotion encouraged us

to take another look.

ECS owns the Idaho Cobalt Project (ICP), which it describes as the

only environmentally permitted, primary cobalt project in the United

States. The project is construction ready and some construction activities

have commenced, although financing for the pre-production capex is not yet

in place.

The Feasibility Study (FS) completed in September-2017

reveals that at a cobalt price of US$26.65/pound (a few percent below the

current market price) the project could be developed into a 2.4M

pounds/year underground mine with an after-tax NPV(7.5%) of US$136M and an

after-tax IRR of 21.3%. The estimated pre-production capex is US$187M.

Taking into account the financing and execution risk, for stock

valuation purposes it is appropriate to apply a 50% discount to the

above-mentioned NPV. We therefore reckon that ICP's fair value is around

US$68M at the current cobalt price.

ECS has 160M shares

outstanding and about US$20M of working capital. Adding the working

capital to the 'guesstimated' fair value for the ICP gives us a rough

valuation of US$88M, or C$116M, for the company's equity. This equates to

C$0.73/share.

Based on the above rough estimate of underlying value

we think that ECS would be a reasonable speculation at around C$0.50, or

not far below Wednesday's closing price of C$0.57. At current prices ECS

does not offer as much value as Cobalt 27 Capital (KBLT.V), but for those

who already own KBLT and are looking for additional cobalt exposure it

could make sense to buy some ECS shares near C$0.50.

The Stock Market

There was drama in the commodity

world on Wednesday 15th August, but nothing of significance happened to

the senior US stock indices.

Based on current positioning relative

to support, the NASDAQ100 (NDX) probably will be the first of the senior

US stock indices to signal a downward reversal. The signal would be a

daily close below the 50-day MA, which is slightly below both Wednesday's

low and the bottom of the channel drawn on the following chart.

Despite the recent sharp declines in some European bank stocks and all

the chatter about major banking-industry losses stemming from Turkey's

economic crisis, there is no evidence, yet, that a widespread banking

crisis is brewing.

One of the places that the evidence would appear

is in the spread between 3-month LIBOR (the short-term interest rate that

banks charge each other) and the yield on the 3-month T-Bill (the

short-term interest rate that the US government pays). When some banks

begin to worry about the financial situations of other banks, this spread

widens.

As the following chart shows, the LIBOR-UST3M spread rose

to near an 8-year high early this year. However, as we explained at the

time, this was due primarily to changes in US taxes and secondarily to a

surge in T-Bill supply. It wasn't due to declining confidence within the

banking system.

Currently, the spread is near the bottom of its

long-term range and there has been no increase in response to the recent

goings-on in Turkey.

Gold and the Dollar

Gold and Silver

The Turkey Effect

How

important will be the downward spirals in Turkey's economy and currency?

Very important, according to financial-market strategist Russell Napier in

a

recent article. He expects a near-total default on the roughly US$500B

of foreign-currency-denominated Turkish debt, with major global

ramifications.

Here are some excerpts from the afore-linked

article:

"It is the nature of EM lending that there is little

in the way of liquid assets to realize; they are predominantly denominated

in a currency different from the liability, and also title has to be

pursued through the local legal system. Turkey will almost certainly be

the largest EM default of all time, should it resort to capital controls

as your analyst expects, but it could also be the largest bankruptcy of

all time given the difficulty of its creditors in recovering any assets.

So the events of last Friday represent only the end of the beginning for

Turkey. The true nature of the scale of its default and the global impacts

of that default are very much still to come.

Strong form capital

controls produce a de facto debt moratorium, and very rapidly investors

realize just how little their credit assets are worth. A de jure debt

moratorium at the outbreak of The Great War in 1914 bankrupted almost the

entire European banking system - it was saved by mass government

intervention. While the imposition of capital controls in recent years has

hit selected investors hard, in Iceland, Cyprus, Greece and key emerging

markets, there has been nothing of this size and it is to be fully borne

by financial institutions who believe they hold not just valuable credit

assets but actually liquid credit assets! The loss of hundreds of billions

of assets recently considered liquid by global financial institutions,

through the de facto debt moratorium of capital controls, will be a huge

shock to the global financial system. This is a different type of default

and its nature, as well as its magnitude, will blindside financial

institutions."

And:

"One wonders why investors

expect President Erdogan, a man who has referred to them as like the loan

sharks who enslaved the Ottoman Empire, to choose to repay the foreigner

and accept the crushing socio-political cost on the local population of

doing so? Even if Turkish institutions have the ability to pay, something

your analyst has long doubted, the President will forbid them from doing

so. This is a large default and it will prove to be almost a total

default.

It matters and, of course, it may be politically expedient

for others to follow the advice of Paul Krugman and the IMF and choose not

to repay their debt obligations to foreigners. This is the new normal. In

a world where ten years of extreme monetary policy has failed to inflate

away debts, it will become increasingly common to repudiate those debts.

Those under the most pressure will be those with the highest levels of

foreign currency debt where inflation can play no role in reducing

increasingly crushing debt burdens - almost exclusively emerging markets."

When there's a currency and debt crisis in an emerging market it sets

off a scramble for the foreign currency in which the bulk of the debt is

denominated, which is generally the US dollar. Furthermore, if there is

fear of contagion then the scramble for dollars will be global and can be

dramatic. Therefore, a short-term effect of the crisis will be US$

strength in the FX market, regardless of what's happening in the US.

The crisis can also lead to increased demand for gold, but since none

of the debt is gold-denominated there will be less urgency to obtain gold

than to obtain dollars. Also, for there to be substantial strength in the

US$ gold price there must be declining confidence in the US economy and

financial system. Such a decline in confidence could be a knock-on effect

of a large-scale debt default centred on an emerging-market economy, but

it rarely will be the initial effect.

At the moment there is no

sign that the Turkey crisis is having a significant negative effect on

confidence in the US economy and financial system. Furthermore, as

discussed in the stock market section of today's report there is no

evidence, yet, that the Turkey crisis is having a significant negative

effect on confidence within the global banking industry. Consequently, it

is not surprising that up until now gold hasn't benefited from the crisis.

Current Market Situation

In

the latest Weekly Update we wrote that both gold and silver probably would

drop below their 19th July lows prior to tradable rallies getting

underway. Plunges to new 2018 lows occurred during the first three days of

this week.

The following daily chart shows that December gold

traded as low as $1180 on Wednesday. What's not shown is that it has since

traded as low as $1167. So, have we hit the bottom?

At this time there is no way of knowing and no solid basis for a

guess. The price could have bottomed at $1240 near the beginning of July,

but the rebound that followed the decline to $1240 failed to move quickly

above the 20-day MA (the thin black line on the above chart). This was a

sign that the short-term downward trend wasn't over. Then, the price could

have bottomed on 19th July when it traded at $1210, but again the ensuing

rebound was weak and failed to get above the 20-day MA in quick time. This

left the door wide open to new price lows.

What we have is a market

that is now very 'oversold' with the sort of sentiment that is often

associated with an important price low, but also a market that is yet to

provide any evidence that a low is in place. The first sign would be a

daily close above $1210 or the 20-day MA, whichever is lower.

Turning to the silver market, on the following daily chart we see that

there was a mini-collapse over the first three days of this week and that

the price tested its July-2017 spike low of $14.34 on Wednesday 15th

August. The market is very 'oversold' on a short-term basis and

potentially will rebound over the days ahead, but long-term support at

$13.60-$14.00 now beckons.

We didn't expect that long-term support

would be tested this year, but such a test now looks likely.

Gold Stocks

Current

Market Situation

The gold-sector capitulation that we've

been warning about at least once per week for the past several weeks is

now in progress. We couldn't be certain that it was going to happen and it

didn't have to happen prior to the start of a tradable rally, but the

set-up for such an outcome was clearly in place and, therefore, the

short-term risk was high.

Now that a capitulation has begun, it

must play out. Given that Wednesday 15th August was the first high-volume

day for GDX (the most important gold-mining ETF) in the decline that got

started in early-July (daily trading volume is shown in the middle section

of the following chart), it's unlikely that Wednesday's plunge marked the

end of the capitulation. However, given that GDX's daily RSI (refer to the

bottom section of the following chart) has fallen to only 16, it's highly

probable that the decline's momentum extreme will occur this week.

Based on what tends to happen when a sell-off generates the sort of

momentum extreme achieved by the gold-mining indices and ETFs on Wednesday

15th August, here's a likely short-term scenario for GDX:

1) A

multi-week price low within the next two weeks, probably not far below the

15th August low.

2) A sharp rebound to the 50-day MA or lateral

resistance (former support) at $21.00, whichever is the lower.

3) A

decline that tests and possibly breaches the August price low, with a

positive RSI divergence.

4) A stronger and longer rebound.

That's the most likely outcome, but there are other realistic

possibilities. One is that we get additional downward acceleration over

the next few days and then jump straight to the stronger/longer rebound

mentioned in step 4) above.

Hedging

In each of the past three Weekly Updates we mentioned that we had

hedged against the short-term risk of a speculative capitulation in the

gold-mining sector via the purchase of GDX put options. Here's what we

wrote on this topic in the 30th July Weekly Update:

"With

regard to our own accounts, over the past couple of months we have taken

some opportunities to raise cash. However, we have also done some buying

when our favourite stocks became 'too cheap'. As a result, we are not as

'cashed up' as we would like to be (we are about 30% in cash at the

moment). Due to having less cash than we would like, late last week we

purchased insurance (against a short-term gold-mining capitulation) in the

form of GDX $20 September put options. These options will quickly lose

most of their current market value if support holds and the gold-mining

sector begins to recover, but they will gain a lot of value if a near-term

breach of support leads to panicked selling of gold stocks."

The 'insurance' GDX put options mentioned less than three weeks ago have

since gained about 1,000% in value, so they proved to be a very effective

hedge. However, it didn't have to be that way, as a rebound or an

extension of the sideways drift would have resulted in these options

losing all or most of their value. If that had happened then the options

would have been like the home fire insurance that results in a small loss

every year that the house doesn't burn down.

A difference between

home fire insurance and portfolio put-option insurance is that in the

latter case you are continually being quoted a price at which the

insurance provider will buy the insurance back. You therefore have to make

a decision on when to sell and take the risk that the timing of the sale

will prove to be far from optimal.

We exited all of our gold-stock

put-option insurance during Wednesday's plunge. Except for a cash reserve

of more than 35%, we are now unhedged.

Depending on the overall

market situation at the time, we may re-establish a GDX put-option

insurance position if there is a rebound to around $21 within the next few

weeks.

The Currency Market

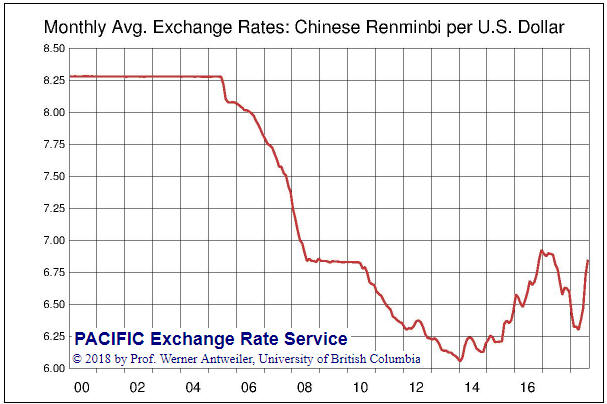

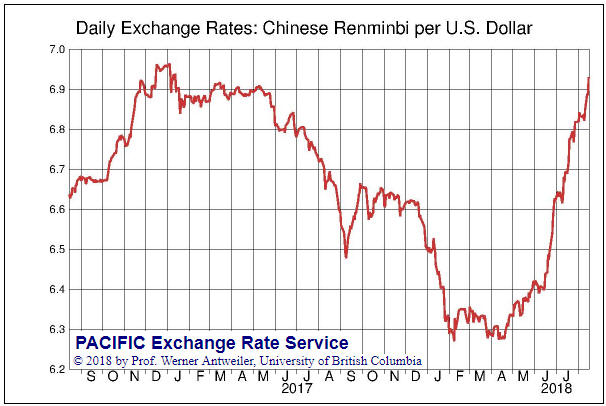

Yuan Update

For the major

financial markets, the US$/Yuan rate is the world's most important

currency exchange rate at the moment. It is vastly more important than the

US$/Turkish-lira rate and even more important than the US$/euro rate. The

reason is that if the Yuan continues to depreciate against the US$ at its

current pace then US$/Yuan will break to a new 10-year high within the

next few weeks, likely leading to a frenetic sell-off in risk assets,

including equities, around the world.

Here is a long-term chart

using monthly averages of the US$/Yuan exchange rate.

And here is a daily chart covering the past two years. The daily chart

suggests that critical resistance is at 6.90-7.00. As we write, this

resistance is being tested.

The Swiss franc (SF) vs the euro

As illustrated by the following daily chart, the SF/euro exchange rate

bottomed near the end of April, broke upward from a declining channel in

mid-May and made a new 12-month high during the first half of this week.

0.91 is the short-term target implied by the chart pattern.

Relative to the US$ the SF possibly bottomed for the year in

early-May, although it is not yet known if the price action of the past

few months is a base (a reversal pattern) or a consolidation (a

continuation pattern).

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() A

trading position in the Physical Platinum ETF (PPLT) was added to the TSI

List on 18th July with a daily-closing stop at $795. The nearest platinum

futures price closed below $795 on Wednesday so the position has been

removed. The result was a loss of about 6%.

A

trading position in the Physical Platinum ETF (PPLT) was added to the TSI

List on 18th July with a daily-closing stop at $795. The nearest platinum

futures price closed below $795 on Wednesday so the position has been

removed. The result was a loss of about 6%.

Note that platinum came

very close to its 2008 Global Financial Crisis low in the $750s on

Wednesday before bouncing, so it may well have just bottomed. However, a

new position can always be added after more evidence of a bottom emerges.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

Pacific

Exchange Rate Service

![]()