![]()

![]()

![]()

![]()

- Interim Update 16th September 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The Fed reaffirms its

counterproductive policy

The statement and forecasts

issued at the completion of the FOMC Meeting on 16th September reaffirmed

the Fed's plan to keep its targeted interest rates near zero for at least

two more years. According to the Fed this is being done to support the

economy, but the reality is that manipulating interest rates to

artificially low levels hinders economic progress.

In the real

world, the economic growth process begins with an increase in savings and

ends with an increase in consumption. Therefore, any actions that

discourage saving, such as pushing interest rates to well below where they

otherwise would be, must reduce the economy's long-term growth. In

addition, the suppression of interest rates leads to mal-investment and

thus the boom-bust cycle. It also enables relatively inefficient companies

to remain in business and in doing so brings about a general reduction in

profit margins.

However, in the back-to-front world of Keynesian

economics (the world in which all central bankers live), economic growth

is driven by increasing consumption. That's why central bank actions that

prompt people to consume more in the present are touted as providing

support to the economy.

Also of significance is that a

heavily-indebted government will benefit from central bank actions that

push interest rates downward. The Fed was never really independent of the

government and these days the Fed and the Treasury act as if they were a

single organisation. In other words, just like both major US political

parties have stopped pretending to care about the budget deficit and the

government's debt, the Fed has stopped pretending to be independent.

The Fed's commitments to keep interest rates near zero for a long time

and to tolerate more "inflation" in the future than was deemed prudent in

the past is bearish for the US$ and very bullish for commodity prices.

Unfortunately, in addition to hampering the US economy's long-term growth,

these commitments run the risk of creating a monetary crisis.

We may have to

adjust our economic roadmap

In early-June we presented the

following picture to explain, in rough terms, the path we expected the US

economy to take over the ensuing two years. Our thinking was that the bulk

of the economic rebound from an April-May trough would be complete by Q4

of this year, with possibly a little more strength during the first half

of next year in response to a multi-trillion-dollar infrastructure

spending bill. Also, we thought that the second economic recession of the

2020s would be underway by 2022. At this time there is no reason to change

our broad-brush outlook for the coming two years, but the risk is rising

that the final quarter of this year will involve a dip rather than the

levelling-off depicted below.

The above economic roadmap was based on four assumptions. The first

was that the severity of the economic contraction caused by the lockdowns

would result in a rapid rebound as soon as the re-opening process began.

The second was that aggressive monetary and fiscal stimulus measures would

continue until late this year. The third was that regardless of the

outcome of the elections in early-November, economic activity would be

given another artificial boost during the first half of next year by the

approval of a massive infrastructure spending program. The fourth was that

there would be too much rot in the economic foundations* to enable the

economy to remain on a growth path beyond mid-2021.

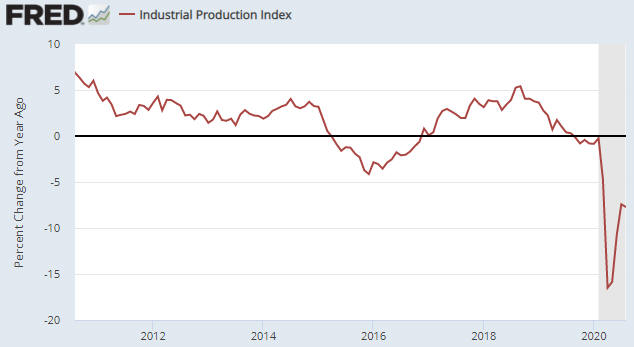

We know that

the first assumption was valid, in that a rapid rebound happened. As

evidence we cite the following chart, which shows that the year-over-year

change in the US Industrial Production Index rocketed upward from an

April-May trough. Also, we see no reason to question the third and fourth

assumptions. However, the second assumption is now in doubt.

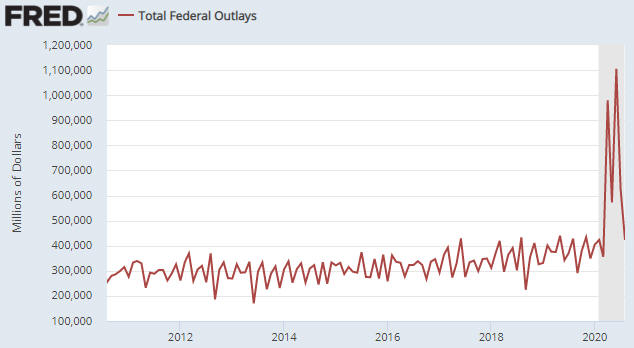

Over the past two months the Fed has added about $200B of securities

to its balance sheet, which implies that the Fed is creating new dollars

at the rate of around 100 billion per month. Furthermore, the Fed has

committed to at least maintain this pace over the months ahead. Although

this is a much slower pace of Fed money-pumping than occurred during

March-May, it still counts as aggressive monetary stimulus. However, the

following chart shows that the monthly pace of total US Federal Government

spending collapsed over the past two months to the extent that federal

spending in August-2020 (the last point on the chart) was roughly the same

as it was in August-2019.

The recent plunge in federal government spending would be a long-term

plus if it indicated a major strategy change, but what it indicates is a

temporary inability of the Republicans and the Democrats to agree on a new

fiscal stimulus package. It's reasonable to assume that a new fiscal

stimulus package will be approved at some point over the next few months,

but unless it is approved very soon (within the next couple of weeks

rather than 2-3 months from now) there probably will be a slowing of

economic activity in the short-term.

Therefore, rather than

essentially levelling-off for two or three quarters as indicated on our

current economic roadmap, there is a rising probability that the pace of

US economic activity will dip over the next few months before rebounding

during the first half of next year in response to both a new fiscal

stimulus package and an infrastructure spending program.

If the

change described above takes place it won't affect our intermediate-term

outlooks for any of the major financial markets. In particular, with

regard to the coming 6-12 months we still would be bearish on the US$,

bullish on gold and commodities, neutral on the US stock market and

bearish on the T-Bond. However, it would result in a bumpy ride in the

short-term, which is why the potential change is worth discussing.

Forewarned is forearmed.

*The rot is due to

mal-investment promoted by the Fed, damage to supply chains stemming from

business closures and restrictions on international trade, the bankruptcy

of numerous small businesses thanks to the lockdowns and social distancing

regulations, and the diversion of resources from the private to the public

sector caused by dramatic increases in government spending and

indebtedness.

The Stock Market

Over the past seven trading days

the S&P500 Index (SPX) has oscillated between its 50-day and 20-day moving

averages. This looks like a consolidation within a short-term correction.

If so, a decline to a new multi-week low (below 3300) will happen soon.

Note that a fairly normal correction would take the SPX down to the

vicinity of its 200-day MA, which at the moment is near 3100.

Given the economic backdrop, it's remarkable that the Dow

Transportation Average (TRAN) traded at a new all-time high on Wednesday

16th September. Refer to the top section of the following daily chart for

the details. What does this tell us about the future?

Well, the

last time the TRAN broke above lateral resistance to a new all-time high

was at around this time two years ago. After trading in new all-time high

territory for a few days in September-2018, the TRAN embarked on a large

(>20%) 3-month decline.

One positive difference this time is that

whereas the TRAN was in a weakening trend relative to the SPX in September

of 2018, the bottom section of the following chart shows that it has been

very strong relative to the SPX over the past four months. Another

positive difference this time is that monetary conditions were tight in

September-2018 and are extremely loose today.

The TRAN is

'overbought' and probably will commence a short-term correction very soon,

but a repeat of Q4-2018 does not appear to be on the cards. We are

expecting a normal correction.

Transportation wasn't the only 'cyclical' sector to strengthen on

Wednesday 16th September. Perhaps spurred on by the Fed's promise to

remain profligate for years to come, there was broad-based strength among

the 'cyclicals'. For example, the stock price of that old industrial

conglomerate General Electric (GE) reversed upward on heavy volume. We

don't have a direct financial interest in GE, but we suspect that it will

perform well over the next 12 months.

Gold and the Dollar

Gold

The "inflation"-adjusted gold price

Below are two long-term monthly charts showing the US$ gold price

adjusted for "inflation" (the US dollar's loss of purchasing power). The

first chart uses the CPI as the "inflation" measure and the second chart

adjusts for "inflation" using the method we developed in 2010.

Note: Our method of inflation adjustment is based on the theory that the

percentage reduction in a currency's purchasing power (PP) should, over

the long-term, be roughly equal to the percentage increase in its supply

minus the percentage increase in the combination of population and

productivity. Due mostly to the long and variable time from a change in

money supply to the associated change in PP, during any given month or any

given year the inflation adjustment estimated using this method probably

will be wrong. However, it should be approximately correct over periods of

7 years or more. It therefore is a big improvement over the CPI, which is

all but guaranteed to be very inaccurate over the long-term.

Both charts are interesting in their own ways.

The gold/CPI

chart shows that the 2011 high was slightly below the 1980 high and that

the August-2020 high (this year's monthly closing high-to-date) was

slightly below the 2011 high. In other words, on a very long-term basis

the CPI-adjusted US$ gold price has just made a triple top. This suggests

that some large gold speculators/investors are tracking gold/CPI and

selling as the 1980 high is approached. In other words, even though the

CPI is not a good measure of the dollar's PP loss, gold's long-term

performance in CPI terms appears to be important.

The chart that

reflects our method of inflation adjustment shows that this year's high

was well below the 2011 high, which, in turn, was well below the 1980

high. It also shows that in 'real' terms the gold rally since the

late-2015 low has been unimpressive to date. This could be viewed as

evidence that gold is not close to being 'overbought' on a long-term

basis.

Current Market Situation

Gold's price volatility in US$ terms has become unusually low. The

following chart shows that the price has been oscillating within a

shrinking range over the past month and that the average daily price range

has also shrunk. This implies that the market is coiling in preparation

for a tradable move in one direction or the other, but unfortunately the

price action does not indicate the most likely direction of this move.

If the Dollar Index (DX) is in the process of reversing upward on a

short-term basis, which currently appears to be the case, then the more

likely direction of gold's next meaningful move is down. This would be

signalled by consecutive daily closes or a weekly close below US$1920.

A break below US$1920 would confirm that a multi-month top was set in

early-August and pave the way for a correction low during

October-November.

Gold Stocks

The gold

mining indices/ETFs continue to mark time. A big move should commence

soon, but the direction of this move is unknown. The August-September

cycle suggests that the direction will be down, but the price action since

the early-August high looks more like a continuation pattern than a

reversal pattern.

For the HUI, short-term downside risk is defined

by lateral support near 260 and the 200-day MA. This implies that there

could be a decline of up to 25% within the next few weeks. A daily close

below the 50-day MA would warn that this scenario was playing out. On the

other hand, if the back-and-forth trading of the past six weeks proves to

be a mid-trend consolidation then a strong 1-2 month rally could be about

to begin.

Dealing with these very different short-term

possibilities is not difficult. Ideally, your 'core' exposure to the gold

mining sector will cover you against the bullish short-term possibility

and you will be hedged against the bearish short-term possibility by

virtue of having built up cash over the past 1-2 months and/or purchased

insurance in the form of put options.

The Currency Market

The global economy usually

looks more vibrant when the US$ is weakening. One reason is that a

weakening US$ encourages inflationary monetary policy outside the US. A

second reason is that a weakening US$ reduces the cost in local currency

terms of servicing US$-denominated foreign debt and incentivises

additional foreign borrowing of dollars. A third reason is that US$

strength tends to be symptomatic of a global shift away from risk and

towards the relative safety offered by the US bond and stock markets.

Consequently, an upside breakout in the Dollar Index (DX) from its

92-94 short-term trading range would warn that we were entering a more

negative 1-2 month period for risk assets, including industrial

commodities and commodity-related equities. By the same token, if the DX

breaks below the bottom of its 92-94 range it will warn that upward

acceleration in the prices of risk assets is likely over the ensuing 1-2

months.

At this stage a short-term upside breakout looks more

likely than a short-term downside breakout, whereas the intermediate-term

outlook for the DX continues to be decidedly bearish. Therefore, we think

it makes sense to have 'core' exposure predicated on US$ weakness while

being hedged against short-term US$ strength.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://research.stlouisfed.org/

![]()