![]()

![]()

![]()

![]()

- Interim Update 16th November 2016

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Trump's first 100 days

At the end of October Donald

Trump released

a list of things that he would do within his first 100 days in office

if elected President. Many of the items on the list are either not

realistic or not important. For example, the first item on the list is: "Propose

a Constitutional Amendment to impose term limits on all members of

Congress." He can certainly propose such a change, but there is no

way that a majority of incumbent politicians will vote in favour of it.

There are, however, items on Trump's "things to do list" that are both

achievable and important. We will now single-out some of the ones that

stand a good chance of happening and would have a significant effect on

the financial markets.

1) "I will direct my Secretary of the

Treasury to label China a currency manipulator".

This is

wrongheaded thinking in three ways. First, every currency is being

manipulated. For example, if China deserves to be labeled a currency

manipulator then so does the US Federal Reserve. Second, the "currency

manipulator" charge would stem from the belief that China's government was

trying to weaken the Yuan in order to obtain a trade advantage, but the

fact that China has reduced its holdings of US government bonds by

hundreds of billions of dollars over the past two years means that China's

government has actually been trying to STRENGTHEN the Yuan. The reality is

that the Yuan has been falling under the weight of its own over-valuation

and China's government has been trying to slow the decline. Third, it's

nonsense that China's economy would gain a trade advantage over the US

economy via an artificially-low Yuan.

Based on wrongheaded thinking

it certainly is, but this is something that Trump seems determined to push

ahead with. The potential effects are reduced trade, higher costs for US

consumers, an increase in the pace at which China's government sells off

its US Treasury bonds and higher US interest rates.

2) "I will

direct the Secretary of Commerce and U.S. Trade Representative to identify

all foreign trading abuses that unfairly impact American workers and

direct them to use every tool under American and international law to end

those abuses immediately".

This implies that the US government

will implement tariffs and put other obstacles in the way of international

trade. Did nobody in US politics learn anything from

Smoot-Hawley?

3) "Middle Class Tax Relief And

Simplification Act. An economic plan designed to grow the economy 4% per

year and create at least 25 million new jobs through massive tax reduction

and simplification, in combination with trade reform, regulatory relief,

and lifting the restrictions on American energy. The largest tax

reductions are for the middle class. A middle-class family with 2 children

will get a 35% tax cut. The current number of brackets will be reduced

from 7 to 3, and tax forms will likewise be greatly simplified. The

business rate will be lowered from 35 to 15 percent, and the trillions of

dollars of American corporate money overseas can now be brought back at a

10 percent rate."

As discussed in the latest Weekly Update,

Trump's proposed tax cuts aren't being funded by reduced government

spending and therefore aren't genuine tax cuts. The private sector will

end up paying, one way or another.

What the tax cuts constitute is

a Keynesian stimulus program, and in this regard they could be effective.

In other words, they could give the economy a significant boost over the

coming year or two at the cost of slower long-term progress. They could

also give equity prices a significant intermediate-term boost (especially

when it is considered that more than 70% of the tax cut will go to the top

5% of taxable-income earners) and add to the upward pressure on interest

rates.

The proposal to lure trillions of dollars of American

corporate money from outside to inside the US will give the Dollar Index

and the US stock market a boost if it is effective, but we don't see why

it would be effective. Why pay 10% to the US government just for the

'privilege' of bringing home money that has already been subject to

foreign tax requirements?

As an aside, the money-supply figures

reveal that there has been a substantial transfer of US dollars from

outside to inside the US over the past 12 months. That is, the

international money flow that Trump's tax proposal is designed to

incentivise has already happened for other reasons. The other reasons are

probably fear of the ECB's profit-crushing Negative Interest Rate Policy

(NIRP), the risk of a European banking crisis, "Brexit"-related

uncertainty, and the range of social, political and economic problems

infesting Europe.

4) "End The Offshoring Act. Establishes

tariffs to discourage companies from laying off their workers in order to

relocate in other countries and ship their products back to the U.S.

tax-free."

This would hinder international trade, lower

corporate profits and increase costs for US consumers.

5) "Repeal

and Replace Obamacare Act. Fully repeals Obamacare and replaces it with

Health Savings Accounts, the ability to purchase health insurance across

state lines, and lets states manage Medicaid funds. Reforms will also

include cutting the red tape at the FDA: there are over 4,000 drugs

awaiting approval, and we especially want to speed the approval of

life-saving medications."

This could be a big step in the

right direction. It could boost the economy, pave the way for more

full-time jobs and save a lot of lives, but it isn't something that's

going to happen in the first 100 days.

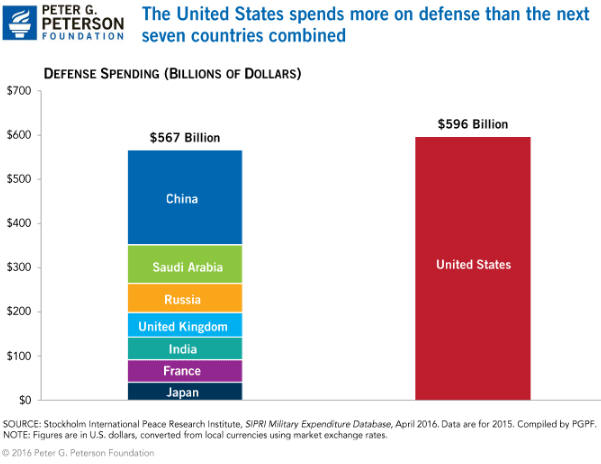

6) "Restoring National

Security Act. Rebuilds our military by eliminating the defense sequester

and expanding military investment".

The idea that the US is

not spending enough on its military is absurd, as made clear by the

following chart.

The problem is that policing the world and being constantly involved

in regime change in multiple countries* is both very expensive and

counter-productive. US foreign policy under Trump is likely to be

less-interventionist that it would have been under Clinton, but funding

the military is still going to place a large burden on the US economy over

the next few years. Moreover, no matter how excessive the size of the

military, war-mongers in the government will always find ways to make full

use of it.

7) Dismantle the

Dodd-Frank Wall Street Reform and Protection Act that was passed in

2010 as part of a typical "closing the stable door after the horse has

bolted" response to the 2007-2009 financial crisis. This wasn't on the

first-100-days list linked above, but Trump has said that it is a top

priority.

It should first be understood that if fractional reserve

banking were recognised under the law as the fraudulent practice that it

is, then there would be no need for any special laws to 'regulate' the

banks. To put it another way, an entity that has been granted the power to

create new legal tender out of nothing has the ability to disrupt the

entire economy and therefore needs a special set of laws/regulations.

Unfortunately, Dodd-Frank is not a useful set of laws/regulations. The

big banks are currently engaged in the same sort of activities that

contributed to the 2007-2009 crisis, so the legislation hasn't achieved

its touted purpose. The legislation has, however, caused the banks to

employ an army of lawyers and compliance officers that produces reams of

paperwork and adds no value. Actually, the 'compliance army' that must now

be employed by every financial institution adds negative value, because

from a customer's perspective it makes dealing with banks, brokers and

other financial firms far more difficult than it should be.

In

effect, Dodd-Frank makes the economy less efficient and its elimination

should be an important plus, although much will depend on what replaces

it.

Summing up, the various proposals aimed at making international

trade 'fairer' will be costly to the US economy. The tax cuts could be

very effective as a short-to-medium-term stimulus program, with

substantially-higher interest rates being the most obvious ramification.

The elimination of some unwieldy legislation, most notably Obamacare and

Dodd-Frank, will help, while growing the already-bloated military will

waste resources.

*Rarely does a week go by

when the US is not involved in the bombing of at least three countries,

and in September it actually managed to

bomb six countries in a single weekend.

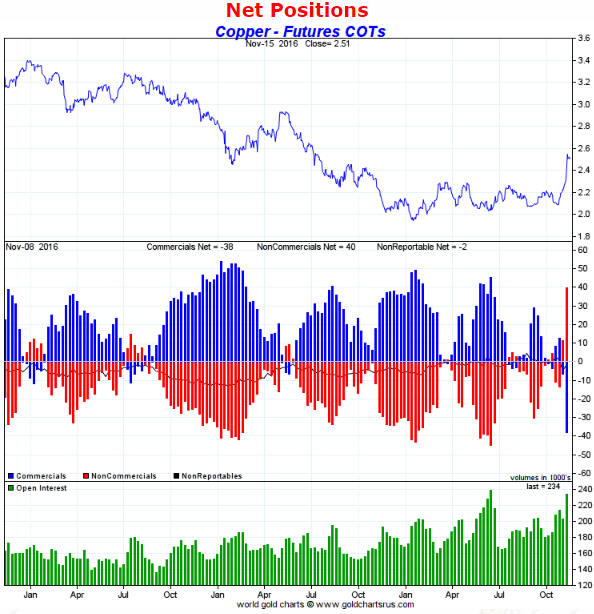

Copper breaks the bear

market pattern

The middle section of the

following chart illustrates the Commitments of Traders (COT) situation for

Comex copper futures. It reveals a spectacular rise in the speculative

net-long position (the red bars) during the one-week period ending Tuesday

8th November, which is the date of the latest available data.

At

8th November the speculative net-long position in copper futures was

actually higher than at any time since early-2004. In other words, it hit

a 12-year high last week. Furthermore, the 8th November numbers don't

include the effects of the post-election price surge.

The dramatic increase in the speculative net-long position in copper

futures has smashed the bear-market pattern that dominated over the

preceding three years. Prior to the past two weeks, whenever the

speculative net-long position in copper futures moved above the zero line

the price was near a short-term peak. The price would then decline until

speculators, as a group, had become net-short to the tune of 30,000-40,000

contracts.

Putting it in simpler terms, the change in copper's COT

situation suggests that copper has commenced a cyclical bull market.

At the same time, the ramp-up in speculation has created short-term

downside risk. In this regard, the copper-futures speculation in China

discussed in the article posted

HERE is of greater concern than the goings-on at the Comex. It seems

that speculators in China will buy any futures contract that happens to be

in a steep upward trend.

The T-Bond is close to a

short-term bottom

Here is a chart of the 20+ Year

Treasury ETF (TLT), a proxy for the prices of long-dated US government

bonds. The bottom section of the chart shows the daily RSI(14), a

short-term momentum indicator.

On Monday of this week, TLT's daily RSI hit its lowest level since the

second quarter of 2007. This means that by one measure, the T-Bond market

is now more 'oversold' than at any time over the past 9 years.

Also

worth noting is that TLT has just experienced a "death cross", meaning

that its 50-day MA has just crossed its 200-day MA from above. Despite the

name, "death crosses" are reliable short-term BULLISH signals, the reason

being that they tend to occur near short-term price bottoms. Specifically,

a "death cross" will often occur near the end of a multi-month correction

within a bull market or around the first short-term bottom within a

long-term decline.

The combination of the 'oversold' extreme in the

daily RSI and the "death cross" suggests that the Treasury market is very

close to a short-term bottom in terms of both price and time.

The Stock Market

The US

In the latest Weekly Update we listed "market internals" as one of three

reasons that there could be a 6-12 month extension to the US stock

market's long-term bullish trend. Here's what we wrote:

"...at

no time over the past several months has there been a meaningful bearish

divergence between the senior US stock indices and the 'market internals'.

Furthermore, during last week's rally the 'internals' were stronger than

most of the indices. For example, whereas the S&P500 Index (SPX) rebounded

to a lower high last week, the UWSPX/SPX ratio (the Unweighted SPX divided

by the capitalisation-weighted SPX, a measure of breadth within the

S&P500) made a new high. This is a bullish divergence."

Today

we wanted to make it clear that the upside breakout by the UWSPX/SPX ratio

was not the only bullish divergence over the past week between the indices

and the 'internals'. Of perhaps greater significance is that there have

been more individual common stocks making new 52-week highs on both the

NYSE and the NASDAQ than at any time over the past few years.

Here's a chart showing the NYSE situation. Within the past few days the

number of individual common stocks making new 52-week highs (the green

bars on the lower section of the chart) hit its highest level of the past

three years even though the NYSE Composite Index was below its

September-2016 peak and well below its 2015 peak.

We hasten to point out that while this is evidence of a continuing

bull market, it does not imply a bullish short-term outcome. There were

many cases over the past 15 years when the number of individual stocks

making new 52-week highs became relatively large just prior to the start

of a significant short-term market decline.

Gold and the Dollar

Gold

Current Market Situation

The US$

gold price almost touched important lateral support in the low-$1200s on

Monday. Also, Monday's intra-day low might have defined the bottom of a

price channel.

The rebound following the test of support has been

weak up until now, so we won't be surprised if there are additional tests

over the days ahead. An intra-day spike below support wouldn't be a

problem, but a weekly close below $1200 would be a problem for the

intermediate-term bullish case.

At this stage the decline from the July peak looks like a routine

correction, but with the 'new bull market scenario' having not yet been

confirmed we shouldn't blindly assume that this is necessarily the case.

In the financial markets, blind assumptions that turn out to be wrong are

often very costly.

We are looking forward to seeing the next set of

COT data as it will show the extent to which speculators liquidated their

collective net-long position during the post-election rout. It will be a

positive development if the total speculative net-long position in Comex

gold futures has fallen to 150K contracts or less.

India's Gold Market

In last week's

Interim Update we linked to an article by Jayant Bhandari dealing with the

general panic, and the panic-buying of gold, that was set in motion by an

incredibly ill-conceived and poorly-planned decision on the part of

India's government to ban the most popular currency notes. A follow-up

article by the same author has been posted at

http://www.acting-man.com/?p=47842. It is a must read.

The

situation in India appears to have gone from very bad to much worse over

the past week. Economic collapse appears to be an imminent risk, all

because of the gross stupidity and arrogance of Narendra Modi, India's

Prime Minister.

Gold Stocks

In the latest

Weekly Update we mentioned that the HUI didn't have any remaining nearby

lateral support of significance, but that the bottom of a price channel

was situated a few points below Friday's low. As illustrated by the

following chart, the channel bottom was reached on Monday.

The rebound from the channel bottom has not done enough, yet, to

indicate that a short-term low or even just a multi-week low is in place.

Conclusive evidence of a reversal would require a solid break above the

channel top, but a daily close above 196 would be an early warning of a

bullish turnaround.

Interestingly, one of the same signs that the

T-Bond market is close to a short-term bottom also applies to the HUI. We

are referring to the fact that the HUI has just experienced a "death

cross". Even if we are dealing with a far more bearish intermediate-term

scenario than we currently have in mind, the "death cross" increases the

probability that a short-term bottom will soon be put in place if it isn't

already in place.

The Currency Market

The Dollar Index

In the latest

Weekly Update we wrote that major resistance at 100.0-100.5 for the Dollar

Index would probably be tested within the next two weeks. As illustrated

below, the resistance is now being tested.

There is a good chance

that this resistance will be breached within the coming few months.

On a short-term basis, the Dollar Index is 'overbought'. This could

result in a few weeks of consolidation in the 98-101 range prior to a

breakout.

The likelihood of an upside breakout in the Dollar Index

within the coming few months represents a threat to gold-related and

commodity-related investments. It is a good reason to be cautious. More

specifically, it is a good reason to maintain a hefty cash reserve and to

look for opportunities to hedge long-term positions.

The Australian Dollar (A$)

The A$

is beginning to confirm the C$'s bearish performance.

The Yen

Our expectation has

been that the Yen's July-August 'double top' near 100 would be followed by

a roughly 10% decline to the vicinity of the 70-week MA, after which there

would probably be a rally to new multi-year highs. This expectation was

based on what happened in the past after rallies from multi-year lows to

above the 200-week MA, and is unchanged.

As illustrated by the

weekly chart displayed below, the 70-week MA is in the 89-90 range and the

current price is 91.7. This should mean that the Yen is now within 2

points of a correction low and in roughly the same position as it was at

the times indicated on the chart by the green arrows.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Premier

Gold (PG.TO) published the long-awaited results of the FS for the

Hardrock (Trans-Canada) gold project after the close of trading on

Wednesday 16th November. The results can be summed up in one word:

lacklustre.

Premier

Gold (PG.TO) published the long-awaited results of the FS for the

Hardrock (Trans-Canada) gold project after the close of trading on

Wednesday 16th November. The results can be summed up in one word:

lacklustre.

The results are lacklustre because they reveal that

the project is economically unattractive near the current gold price. The

project has significant option value, but there is little chance of it

being shifted into the construction phase with the gold price at or below

US$1250/oz. If all else remains the same, a gold price of at least

US$1400/oz will probably be required.

Although the results are

unimpressive, they aren't surprising. We were hoping for better, but the

delays in completing the FS and PG's efforts to de-emphasise the Hardrock

project by making investments elsewhere were warnings that Hardrock's

economics would not justify mine development anytime soon.

If the

stock market were an unemotional weighing machine then the FS results

wouldn't lead to additional weakness in PG's stock price. This is because

PG offers good value at its current price even if a value of zero is

assigned to Hardrock. However, the stock market is a highly emotional

voting machine.

There will be additional comments on Hardrock's FS

in the Weekly Update.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.goldchartsrus.com/

![]()