![]()

![]()

![]()

![]()

- Interim Update 17th February 2016

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Oil Update

On Tuesday the oil price

initially moved higher when it was reported that representatives of Saudi Arabia

and Russia, the world's two largest oil producers, were in discussions regarding

oil supply. The gains were soon given back, though, when it was reported that an

agreement had been reached to freeze production at January-2016 levels. Freezing

production at a record high obviously does nothing to improve the fundamentals

driving the oil price.

In any case, we don't need to read/watch the news to know that supply/demand

fundamentals remain unsupportive for the oil price. All we have to do is look at

the spread between spot prices and futures prices in the oil market. The larger

the contango, that is, the higher the futures price relative to the spot price,

the more abundant the current supply and the less price-supportive the

fundamental backdrop.

Oil for delivery in about 6 months' time (July-2016) is currently $6.40/barrel,

or about 20%, more expensive than oil for immediate delivery onto the cash

market. This is very unusual. It means that if someone could buy physical oil

and store it cheaply they could make a risk-free annualised return of almost 40%

by simultaneously selling July futures contracts. The reason that every man and

his dog is not eager to do this trade is that the cost of storing oil is now so

high that even a contango that represents a potential 40% annualised return on a

physical-futures arbitrage is not very profitable. And the reason that the cost

of storing oil is now so high is that there is a much-greater-than-normal amount

of oil already in storage.

Unfortunately, knowing that there is an oil glut and, therefore, that the

fundamentals remain bearish doesn't tell us what will happen to the oil price in

the future. This is because the bearish fundamentals are very well known and are

factored into the current price. It is also because the fundamentals are always

bearish at major price bottoms in commodities markets.

We suspect that the oil price is close to a major bottom. This is because in

real terms it is now below its 1986 bottom and at its recent low was almost as

low as its 1998 bottom (the two lowest points of the past 40 years). It is also

because if stock markets have made long-term peaks then the commodities markets

are likely to be among the main beneficiaries of future monetary inflation.

However, it's very unlikely that there will be a 'V' bottom in the oil market.

Considering the short-term positive correlation between the oil price and the

S&P500 Index (see chart below) and the well-known bearish fundamentals, it's

more likely that the oil market will build a base this year involving a Q1

bottom and one or two successful tests of the bottom.

The Stock Market

The US

In last week's Interim Update, we wrote:

"Although the SPX's price action suggests that there will be a spike below

the 20th January low (1812) before the next multi-week bottom is in place, there

have recently been two positive developments in the US stock market. The first

is that the Dow Transportation Average (TRAN), which was relatively weak and led

to the downside from late-2014 through to 20th January of this year, has started

to show relative strength."

And:

"The other positive development is the recent divergence between the NASDAQ

Composite Index (NAS) and the NASDAQ's McClellan Oscillator (MO) illustrated by

the following chart. We are referring to the fact that this week's new price low

for the NAS coincided with a higher low for the NAS's MO."

We concluded as follows: "We expect that another multi-week rebound or period

of consolidation will soon begin, but there could first be spikes to new lows by

the SPX and some other stock indices."

The next day the SPX spiked below its 20th January low and then reversed upward.

It traded as low as 1810 last Thursday and is now (as at the end of the 17th

February session) at 1927, meaning that there has been a 117-point turnaround in

only 4 trading days.

TRAN continues to lead. Whereas the SPX is still comfortably below its 50-day

MA, the following chart shows that TRAN has decisively broken above this MA.

There is no evidence that the rebounds of the past few days are over.

Furthermore, due to the successful test of the SPX's 20th January low and the

extent to which the market was 'oversold' last week, there could be 1-3 months

of consolidation prior to the start of the next tradable decline.

At the same time, the SPX is nearing important resistance at 1950 and TRAN is

nearing even more important resistance at 7400. These levels will probably cap

the upside over the days immediately ahead.

The Emerging Markets

The Emerging Markets Equity ETF (EEM) has rebounded to trend-line resistance, MA

resistance (the 50-day MA) and within 50c of important lateral resistance. Refer

to the following chart for details. This means that a rebound peak could be

close in terms of both price and time.

Put Option Tactics

We took profits on all bearish positions (put options, in our case) near the

lows in mid-January and have since been waiting for the right time/price to

re-enter. With the SPX, TRAN and EEM nearing important resistance levels, there

is now a decent opportunity to START entering new bearish positions.

We emphasised the word "start" in the preceding sentence because, as discussed

above, there's a realistic chance that the stock market will consolidate for 1-3

months before embarking on a decline that solidly breaches the January-February

lows. To put it another way, this is not the time to be diving head-first into

leveraged bearish trades, but some exposure to the 'dark side' might now be

warranted.

With regard to new bearish positions, we don't plan to add anything to the TSI

Stocks List in the near future. Instead, we'll wait and hope for a better entry

point. Also, we haven't done anything in our own account yet, but we might make

an initial purchase of EEM June-2016 $25 put options within the next two trading

days.

Note that if our overall market outlook is close to the mark then EEM's days of

relative weakness (weakness relative to the SPX, that is) are almost over,

implying that EEM is not the ideal target for a new bearish speculation.

However, we have begun to build exposure to non-gold commodity stocks. The

relevance is that due to the long-term positive correlation between

emerging-market equities and commodity-related equities, an EEM put-option

position can serve as a hedge against declines in non-gold commodity stocks.

Gold and the Dollar

Gold

Goldman Sachs (GS)

reiterated its bearish gold forecast at the beginning of this week. Gold

will slump to $1100 an ounce in 3 months and $1000 an ounce in 12 months,

according to a gaggle of GS analysts.

GS's short-term timing was quite good, in that late last week the gold market

was almost as 'overbought' on a short-term basis as it ever gets (refer to the

latest TSI Weekly Update for details). The premise of the bearish forecast is

probably wrong, though, because it revolves around a strengthening US economy

and rising real interest rates.

Additionally, with a company such as GS you always have to wonder whether the

forecasts put out for public consumption accurately reflect the expectations of

its senior traders and managers. We suspect that there will often be a

substantial difference between the information made public and the information

on which GS is acting for its own account, but we don't care either way. If

gold's true fundamental drivers have made a sustainable shift into bullish

territory then the gold price has bottomed and will work its way upward over the

coming 12 months, regardless of what GS's analysts say in public and regardless

of what its senior staff genuinely expect.

But even if the true fundamentals have made a sustainable shift into bullish

territory, the extent to which the gold market was 'overbought' late last week

is a reason for short-term caution. The price action hasn't yet signaled that a

multi-week top is in place, but it certainly could be.

As illustrated below, Tuesday's sharp decline in the US$ gold price ended at

former resistance (now support) defined by the October-2015 peak. There is

currently no way of telling whether this sharp decline was a routine pullback to

'test' the preceding upside breakout prior to the resumption of the rally or the

start of a correction that will run for at least a few weeks. A daily close

below $1190 would point to the latter.

Gold Stocks

In the email sent to subscribers following Tuesday's US trading session, we

wrote:

"...the price action on Wednesday 17th February could provide us with a clear

signal -- or at least a clearer signal than we currently have -- that short-term

price tops were put in place last week. To generate such a signal, all it would

take is a down-day for the HUI on Wednesday."

Wednesday was a small up-day for the HUI, so a short-term top hasn't yet been

signaled. This means that there could still be a rise to a new high for the year

prior to a top that holds for more than a few days. We don't have a strong

opinion on the matter.

In the latest Weekly Update we used a moving-average (MA) envelope to illustrate

the unusual degree to which the US$ gold price was stretched to the upside at

last week's high. Below is a similar chart that shows the unusual degree to

which the HUI was stretched to the upside late last week.

In its entire 20-year history the HUI has never been higher relative to its

50/20 MA envelope (a 20% envelope around the 50-day MA) than it was at the end

of last week.

Although the above chart indicates an 'overbought' extreme and suggests that a

correction will soon begin (if it hasn't already), it also supports the view

that a cyclical bull market has started. The reason is that the only times in

the past that the HUI got close to being as stretched to the upside on a

short-term basis as it was last Friday was during the first 6 months of the

multi-year rally that began in November-2000 and the first few months of the

multi-year rally that began in October-2008. In contrast, the bear-market

rallies of 2012-2015 ended at or below the top of this MA envelope.

Buying opportunities in individual gold stocks will continue to crop up, but the

next sector-wide buying opportunity probably won't occur until the HUI trades

near its 50-day MA. This could happen within a week or it could take as long as

two months. The 50-day MA is presently in the low-120s, but it is rising and

could be at a much higher level by the time the price reaches it.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() New

TSI stock selection: Petrus Resources (TSX: PRQ). Shares: 45M issued, 48M fully

diluted. Recent price: C$2.95

New

TSI stock selection: Petrus Resources (TSX: PRQ). Shares: 45M issued, 48M fully

diluted. Recent price: C$2.95

It has been many years since there was an oil-and-gas (O&G) stock in the TSI

List. That changes today, with the addition of Petrus Resources (PRQ.TO).

PRQ has been operating for a few years but only began trading on a public

exchange (the TSX) last week. The stock traded as high as C$4.99 on its first

trading day (8th February) and has since traded as low as C$2.85. In other

words, it had a volatile start to its life as a publicly-traded company. It

ended Wednesday's trading session at C$2.95.

The company has Canada-based current production of about 9,000 boe/d (barrels of

oil-equivalent per day), split 35%/65% between liquids and natural gas. It is

therefore more of a natural gas producer than an oil producer.

Detailed financial records for the company aren't yet available, but according

to

PRQ's presentation the company generated operating cash flow of C$1.35/share

in 2015. This year's cash flow could be lower due to lower average prices for

oil and gas, although some of the price risk has been removed via hedging (about

half of this year's production has been hedged).

As is the case with most O&G producers, PRQ has substantial debt relative to the

size of the company. According to the above-linked presentation, there is net

debt of C$150M. There is also unused credit of C$100M.

The senior management and board members of PRQ are well known and

highly-regarded within the Canadian oil industry. For example, the chairman is

Don Gray, the founder and former CEO of Peyto Energy (PEY.TO). Peyto was one of

the biggest success stories in the O&G industry over the past 16 years, rising

from around $0.20/share to more than $30/share (16 years of better than 35%/year

compound growth).

PRQ's primary aim at this time is to take advantage of the O&G industry

depression by picking up quality assets on the cheap. As long as there is a

turnaround in the coming year or so, the worse things get for the O&G industry

in the short-term the better it should ultimately be for PRQ.

PRQ should be viewed as a long-term speculation based on the potential for a

sustained turnaround in the oil market this year. If, like us, you think that

such a turnaround is likely then it could make sense for you to average into a

PRQ position. However, if you are convinced that excess supply will result in a

depressed (US$25-$35 or lower) oil price for at least a few more years, then PRQ

is not a stock for you.

At this time it is difficult to come up with a valuation and price target for

PRQ. There just isn't enough to go on. That being said, it is probably

significant that PRQ completed a private placement at C$7.40/share with

knowledgeable/experienced investors only one month ago. Also, C$7.40/share was

the indicative value used when PRQ recently purchased Phoscan (FOS.V) in order

to get hold of FOS's C$45M of cash. This suggests to us that the shares offer

good value near their current price of C$2.95.

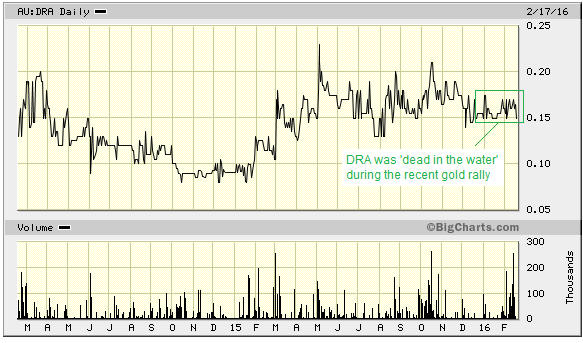

Updated thoughts on Dragon Mining (ASX: DRA)

Updated thoughts on Dragon Mining (ASX: DRA)

DRA is not a current member of the TSI Stocks List, but it is a member of the

TSI Small

Stocks Watch List. This means that we think it has speculative merit, but is

probably too risky and/or too illiquid to be closely tracked at TSI.

DRA's stock price barely moved during the recent gold-mining rally. This is

despite the fact that DRA has 50K ounces/year of unhedged current production and

therefore gets an immediate bottom-line benefit from a higher gold price.

The lack of response by DRA to the recent gold rally is partly due to the stock

not being well known and partly due to gold-stock speculation being focused on

the more liquid stocks at this early stage of what is probably a new bull

market. It is also, we suspect, due to a concern that DRA doesn't have much in

the way of reserve life, that is, a concern that DRA could run out of ore to

feed its production facilities in Sweden and Finland within the next couple of

years. This is a legitimate concern that the company is attempting to address

via the development of the Faboliden mine in northern Sweden. With a current

resource of 743K ounces grading 3.3-g/t this mine could provide profitable ore

feed for many years, but the risk is that it still has to be permitted and

developed.

DRA has a strong cash position, with net cash of A$16.5M (about A$0.18/share) at

31st December 2015. This means that DRA is still trading below its cash value,

although the amount of cash fell by almost A$4M last year as the company

invested in new sources of production.

With DRA's mining assets still being valued by the stock market at less than

zero, the stock is a speculative buy. However, it's possible that a LOT more

patience will be required with this one.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://bigcharts.marketwatch.com/

![]()