![]()

![]()

![]()

![]()

- Interim Update 17th June 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

It is very different

this time

The phrase "this time it's

different" is usually dangerous, because most of the time when market

participants believe that the current situation is different they are

kidding themselves and eventually will incur a hefty cost for the belief.

However, at the moment the phrase could not be more appropriate.

Due to government and central bank intervention on a never-before-seen

scale, financial markets and economic statistics recently have done many

things they have never done before. Here are two examples:

1) In

the US, the rate of growth in personal income has plunged during every

recession prior to this year. This is hardly surprising, given that as the

economy contracts more people will be out of work and there generally will

be less scope for salary/wage increases for the people who remain

employed.

During the first three months of the recession that

officially began in February-2020, however, the rate of increase in

personal income rocketed upward. This is illustrated by the first of the

following two charts, which shows that at the end of April-2020 the

year-over-year rate of growth in US personal income was at its highest

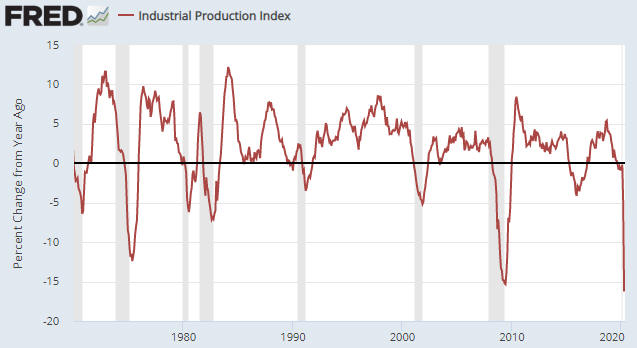

level since the early-1980s. Contrast this with the second of the

following charts, which reveals the largest year-over-year decline in US

Industrial Production in more than 70 years. So, we have soaring personal

income in the face of collapsing production. Nothing remotely similar to

this has ever happened before.

This strange turn of events is the

result of a substantial recent increase in unemployment benefits. Due to

this change, many people are making more money being unemployed than they

did when they were working.

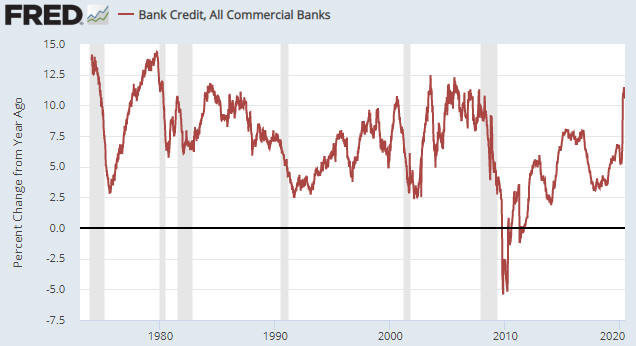

2) The rate of growth in US bank credit made a multi-year peak prior

to every previous recession of the past fifty years. It then plunged

during the recession. This time around it couldn't be more different.

The following chart shows that rather than plunge like it normally

does during the first few months of a recession, during the first few

months of this year's recession the year-over-year rate of growth in US

bank credit surged to a 12-year high. We assume this was the result of

many companies responding to the lockdowns by maxing-out existing credit

facilities as fast as they could, either because they needed additional

money in the short-term or for risk management purposes.

Now, it

isn't unusual for company managements to behave this way, but it is

unusual for banks to accommodate such behaviour on an economy-wide scale.

During normal cycles, banks start tightening credit before it becomes

clear that the economy is in recession and are very restrictive in their

lending practices during recessionary periods. In other words, most

businesses usually don't have the option of increasing their bank debt

during recessions.

The most plausible explanation for the dramatic

difference in bank credit growth during the 2020 recession is that the

leaders of commercial banks believe that the Fed is now backstopping all

bank lending. In effect, the Fed has removed the risks that caused the

commercial banks to 'pull in their horns' during previous economic

downturns, or, to put it more aptly, the Fed has transferred the risk of

loan default from the commercial banks to savers and taxpayers.

Clearly, it is different this time. The economy is recording many

firsts and so is the stock market. Considering the scale of the

intervention on the part of both the government and the Fed, it won't be a

major surprise if the S&P500 Index makes a new all-time high late this

year or during the first half of next year in the face of double-digit

unemployment.

Oil Update

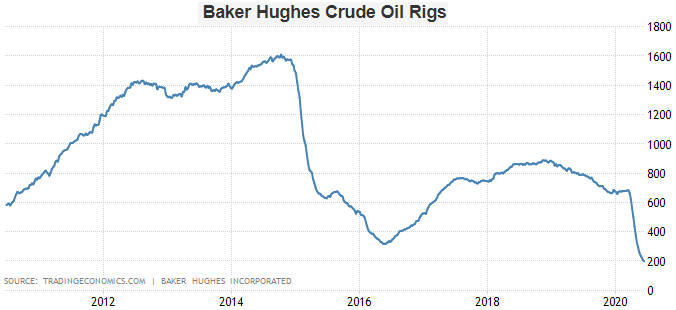

The oil market remains well

supplied, but there is no longer a glut and the potential exists for the

oil supply situation to tighten (become more price-bullish) over the next

six months due to a decline in US oil production.

US oil

production peaked about three months ago at 13M b/d and already has fallen

by 15% to around 11M b/d. Furthermore, a large additional decline appears

to be 'baked into the cake' due to the change in the rig count illustrated

by the following chart. In less than three months the number of operating

oil rigs in the US has plunged from 700 to 200.

We expect that declining oil production, a weakening US$ and

increasing oil demand as the world goes back to work will conspire to move

the oil price up to the $60s by the first half of next year, but long-term

support/resistance at $42 probably will cap the price over the next three

months. Also, if we get a meaningful stock market correction within the

next couple of months then the next $10 move in the oil price is more

likely to be down than up.

The Stock Market

Early this week the S&P500 Index

(SPX) again tested and held its 200-day MA. It then rebounded to the

short-term resistance created by last Thursday's gap to the downside.

Fluctuations between 3000 and 3150 are essentially meaningless. The

SPX must break out of this range to signal the start of a significant

move.

We'll take a look now at the Russell2000 SmallCap ETF (IWM), which has

been relatively weak since the start of this year. The following chart

shows that IWM rebounded over the past two days to test important lateral

resistance at $145 and 200-day MA resistance at $147. The resistance held,

so IWM's position is a little precarious.

Short-term risk was already high prior to this week, but the risk has

escalated due to a COVID-19 outbreak in Beijing. In an effort to contain

the latest outbreak, parts of Beijing have been locked-down/quarantined

and schools have been closed.

This development could become

significant, mainly because the stock market has been acting as if the

all-clear had been sounded and a quick return to the pre-virus/lockdown

world was underway. Part of the reason for this unrealistic optimism (the

cold, hard reality is that so much damage was done by the lockdowns that a

return to pre-virus economic conditions will take years, if it happens at

all) was China's recent economic resurgence, so China taking a step

backward could throw a figurative bucket of cold water on bullish equity

speculators.

Also, evidence that China is retreating economically

could dampen the spirits of bullish commodity speculators. We are bullish

on industrial commodities with regard to the coming 12 months, but we do

not think that the short-term risk/reward is favourable.

The upshot

is that we remain focused on the potential for a decline that retraces up

to half of the rally from the March-2020 low. For the SPX, that implies

the potential for a decline to the 2700s. Given the extent of the Fed's

current support and the near certainty that the Fed will be quick to

provide even more support if it seems that a large stock market decline is

getting underway, at this stage the probability of the SPX retracing

substantially more than half of the March-June rally is low.

Gold and the Dollar

Gold

The

US$ gold price has been consolidating for more than two months. Therefore,

in terms of time this is now a significant correction, even though the

price has stayed at a high level.

In euro terms the recent price action has been more bearish. With

reference to the following chart, the euro gold price signalled a

short-term top by breaking below important lateral support eleven trading

days ago. It has since rebounded to test its downside breakout.

Although speculator positioning in gold futures is less of a risk now

than it was a few months ago, it is still the biggest short-term threat to

the gold market. The gold price is being supported by bullish fundamentals

that could become even more bullish over the next few months due to a dose

of economic realism and a stock market correction, but there is still the

potential for a quick decline to US$1560-$1600 in response to a rush for

cash by leveraged speculators.

For many investors a quick decline

of up to 10% wouldn't be a problem, but for some it would be. We would

welcome a near-term shakeout, because as long as the fundamentals remained

bullish it would create a better risk/reward for new purchases.

However, there's no assurance that we'll get a shakeout of speculator

'longs' before the next rally to new multi-year highs gets underway. We

are prepared for it, but we aren't betting on it.

Gold

Stocks

The HUI made its peak for this year to date in

mid-May, but all the price action since late-April could be interpreted as

being part of a consolidation/correction. In other words, it could be

argued that the gold mining sector has been in correction mode for almost

two months, even though the HUI made its high about a month ago.

The following daily chart shows that the HUI has been 'peppering' support

at 260. It has tested this support on ten of the past eleven trading days

without ever closing below it.

We suspect that a daily close below 260 would be followed by a decline

to 220-230. This is the short-term downside risk, which admittedly isn't

substantial. In fact, with the HUI at 260 the short-term risk is low

relative to the intermediate-term reward potential.

The

Currency Market

We think that the Dollar Index (DX) is in

the early stages of a cyclical bear market. That's the big picture.

Zooming in on the short-term situation, the DX is immersed in a multi-week

rebound that probably will extend to the 98.0-98.5 range.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Euronav

(EURN) trade stopped out

Euronav

(EURN) trade stopped out

The EURN trading position that

was added last month closed below its trailing stop on Wednesday 17th June

and has been removed from the Stocks List. The result, including

dividends, was a loss of 6%.

We will look for an opportunity to

return EURN to the List before the company's next quarterly financial

performance is reported on 6th August, because the reported earnings

should be very good.

The ideal place for new buying would be near

the March low in the mid-US$7 area, but obviously there is no guarantee

that the price will get that low.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://tradingeconomics.com/

https://research.stlouisfed.org/

![]()