![]()

![]()

![]()

![]()

- Interim Update 17th October 2018

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Commodities

Update on uranium's

recovery

Our most recent comment on uranium was in the

24th September Weekly Update. At that time we wrote: "This year's rebound

in the uranium price has been slower and longer than the rebounds that

began in late-2016 and late-2017. This suggests that it has been propelled

by a steady rise in commercial demand relative to supply as opposed to a

burst of speculation, which could mean that it will have more staying

power."

The uranium price has since edged a little higher, which

suggests that the slow recovery is continuing and that the price rise will

prove to be sustainable.

Traders of uranium-mining equities have viewed the latest rebound in

the uranium price with scepticism. In fact, the $5-$6 increase in the

uranium price from its early-February level has resulted in no increase in

the Global X Uranium ETF (URA). From a contrarian perspective, this is

longer-term bullish.

For URA, a daily close above $13.80 would be

an upside breakout and suggest that a multi-month rally had begun, while a

daily close below $12.00 would paint a short-term bearish picture.

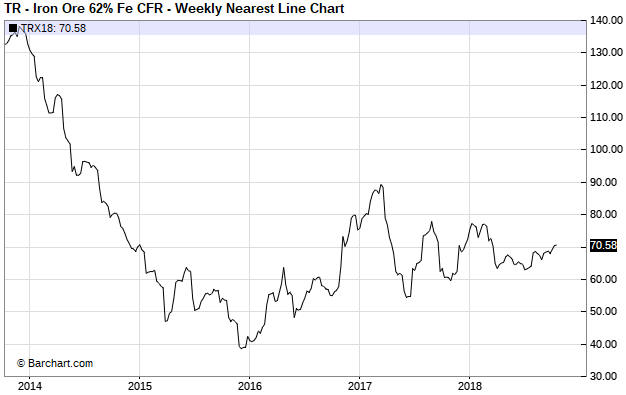

The resilience of the iron-ore price doesn't fit the narrative

Over the past several weeks the per-tonne iron-ore price worked its

way up from the low-$60s to the low-$70s. This up-move doesn't yet look

meaningful on the weekly chart (see below), because it hasn't resulted in

a breakout or changed the price pattern in a significant way. It's

interesting, though, because it is at odds with the popular "China's

economy is tanking" narrative.

It isn't just iron-ore. Signs of strength have appeared recently in

the markets for most industrial metals.

It's still early days, but

it looks to us like the industrial metals complex has completed its

downward correction.

The oil price takes out short-term

support

The oil price tested and held short-term support

at $70.50 during the final two days of last week, potentially setting up a

minor rebound. In the latest Weekly Update we wrote that a rebound to

$72.50-$73.0 would not be surprising and would create a new opportunity to

bet against oil via USO put options expiring in January-2019.

The

oil price traded as high as $72.70 on Monday, but it was downhill from

there. On Wednesday, short-term support at $70.50 was breached.

The

next support of significance is the 200-day MA, which is presently at

$67.20. This support probably will hold (temporarily) if it is tested in

the next few days.

The Stock Market

Warning Signals

There were more than the usual number of warning signals ahead of the

recent sharp stock-market decline, all of which were highlighted in TSI

commentaries prior to the start of the decline. Specifically, there was a

bearish divergence of the NYSE Advance-Decline Line (ADL) beginning in

late-August, a switch to "bearish" by our Equity True Fundamentals Model

(ETFM) on 7th September, a rare sell signal from the TSI put/call

indicator on 26th September, and, most importantly, a downside breakout by

the T-bond price on 3rd October. These were all warnings that a

potentially-steep short-term or intermediate-term stock market decline was

coming. However, up until now there haven't been any warnings that a bear

market is about to begin.

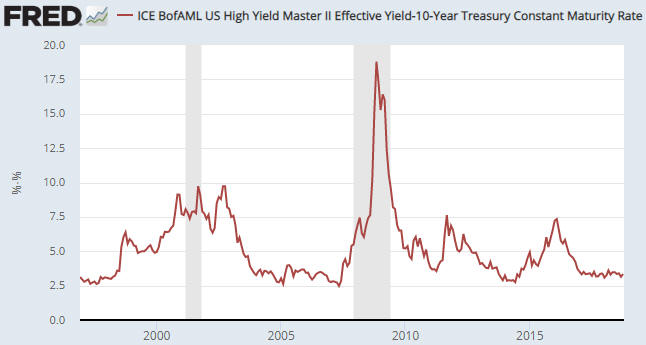

Something that's likely to happen prior

to the start of the next equity bear market is a clear-cut trend reversal

in credit spreads. More specifically, there likely will be a significant

widening of credit spreads. However, the following chart shows that credit

spreads remain near their lows of the past few years.

Arguments

have been made that credit spreads may not lead the next bear market the

way they led previous bear markets. As explained in a

blog post earlier this week, we don't find these arguments persuasive.

Instead, with regard to warning of major trouble in the economy and the

stock market we think that credit spreads are more likely to generate a

false positive signal than a false negative signal. Putting it in more

colourful terms, they are more likely to cry wolf when there is no wolf

than to not cry wolf when there is a wolf.

Something else that's likely to happen at or prior to the start of the

next equity bear market is a significant steepening of the yield curve

driven by falling short-term interest rates. Over the past 6 weeks there

has been a minor steepening of the yield curve, but it was driven by

rising long-term interest rates rather than falling short-term interest

rates. A steepening of the yield curve driven by rising long-term interest

rates is evidence of increased inflation expectations, not evidence that

an economic bust or equity bear market is about to begin.

That

being said, there is a risk that the above-mentioned warning signals and

other historically-reliable leading indicators won't trigger ahead of the

next bear market. Furthermore, with the broad US stock market more

expensive than it has ever been and monetary conditions relatively tight

it is not hard to imagine that the long-term bull market is close to its

end. Fortunately, with or without a suite of reliable leading indicators

there will be clear bear-market warnings in the price action while the

market is still near its high in terms of both price and time. We'll

mention two of these warnings in the coming Weekly Update.

Current Market Situation

Here are the short-term scenarios

that we described in last week's Interim Update and again in the latest

Weekly Update:

"One possibility is a correction low within the

next few days. This will be most likely if the SPX's decline extends well

beyond its 200-day MA -- perhaps to as low as 2650 -- without more than an

intervening 1-day bounce.

A second possibility is an interim low

within the next three days and within 3% of Wednesday's close, followed by

a 1-3 week rebound and then a decline that tests the October low in

November. In this scenario, taking out the October low could lead to a

crash."

Also, in the Weekly Update we wrote:

"...although

there's a high probability that last Thursday's intra-day low will be

taken out before the overall decline comes to an end, we can't rule out

the possibility that the correction low was put in place on Thursday 11th

October."

The second possibility appears to be the most

likely, in that last Thursday's low for the SPX was within 3% of last

Wednesday's close and we are now almost one week into a rebound.

For the SPX, the breakdown level (the support that had to hold to maintain

the short-term upward trend) was 2870-2875. This former support is now

critical resistance and defines the highest level that could be achieved

by a counter-trend rebound, especially since it now coincides with the

50-day MA. To be clearer, if the rebound extends further than 2875 on a

daily closing basis then it is far more likely to be part of a new upward

trend (a rally to new all-time highs) than a reaction within a continuing

downward trend.

For the NASDAQ100 Index (NDX), the breakdown level was 7400. This

former support now defines the maximum level that could be achieved by a

counter-trend rebound.

We think that the market is immersed in a counter-trend rebound that

will end with the SPX between 2850 and 2870. Our plan, therefore, is to

buy some additional SPY December-2018 put options if the SPX trades at

2850-2870 within the next two weeks.

Gold and the Dollar

Gold

At

the moment, the exciting action is in the stock market. The gold market is

making steady upward progress without much fanfare.

During the

first three days of this week the US$ gold price made a marginal new high

for the rally that began in mid-August, but it's more appropriate to

characterise this week's performance as a consolidation than as an

extension of the rally.

With the fundamental backdrop gold-bearish and not close to turning

bullish we continue to view gold's recovery from its August low as a

counter-trend rebound. At the same time, with sentiment still very

constructive and the market not close to being short-term 'overbought', we

expect additional gains prior to the next multi-month top.

As

previously advised, we think that the gold price stands a good chance of

rising to the vicinity of its 200-day MA (near $1280) within the next few

weeks.

Silver

The silver price has

short-term resistance at $14.90. Getting through this short-term

resistance would, we think, be followed by a quick move up to the

longer-term resistance in the $15.60s or the 200-day MA near $16.00.

Gold Stocks

Perhaps not surprisingly, the

gold-mining sector performed similarly to gold over the first three days

of this week. The HUI made a new 2-month high, but the price action was

more of a consolidation than a rally extension.

Support at 150

should hold on a closing basis during any further consolidation over the

days ahead. If it does, then a near-term rise to around 170 will be a good

bet.

Based on the information we have today, a near-term rise to

around 170 would prompt us to do some selling and/or hedging.

It's worth mentioning that for the moment the gold-mining indices are

negatively correlated with the senior US stock indices. In particular, we

note that last week's sharp stock-market decline was accompanied by a

gold-mining rally and that the stock-market rebound of the past four days

was accompanied by a gold-mining consolidation. This suggests that the

gold sector will benefit from an extension of the stock market's

correction, as long as the correction doesn't evolve into a crash.

The Currency Market

The euro broke below important

lateral support in early-October and then rebounded to slightly above the

breakdown level. The rebound appears to have been a successful test of the

breakdown. If so, a return to the August low near 113 probably will happen

within the next few weeks.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://www.barchart.com/

https://research.stlouisfed.org/

![]()