![]()

![]()

![]()

![]()

- Interim Update 18th April 2018

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

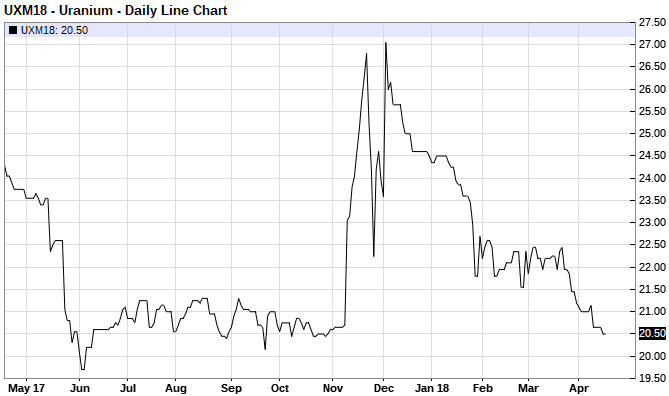

Strange uranium-mining

rally

The first of the following daily

charts shows that the Global X Uranium ETF (URA), a proxy for the

uranium-mining sector of the stock market, has rebounded strongly over the

past three weeks. This is a rather strange sentiment-driven rally, because

the second of the following daily charts shows that over the same period

there were no signs of life in the uranium futures market. Instead, over

the past three weeks the uranium price extended the downward trend that

got underway in December.

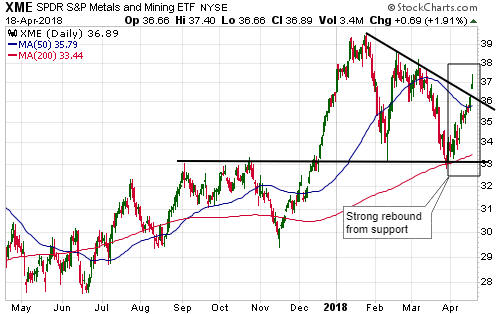

It's likely that uranium-mining equities have been boosted by an

increase in demand for mining equities in general, which, in turn, is

related to anticipation of a US$ breakdown and, more recently,

ill-conceived

US government sanctions against some major Russian commodity producers.

The general mining rebound is illustrated by the following chart of

the S&P Metals and Mining ETF (XME).

Due to the complete absence of support from the uranium price, we

think that the current rally in uranium-mining stocks should be viewed as

a selling opportunity. There are presently no uranium stocks in the TSI

List, but in our own accounts there is exposure to uranium via the shares

of Energy Fuels (EFR.TO). For your information, we probably will exit this

position if there is significant additional share-price strength over the

coming few weeks.

The Stock Market

The most interesting development

over the first three days of this week was the relative weakness in the

banking sector. As illustrated by the following chart, the Bank Index

(BKX) has dropped back to near its low for the year and the BKX/SPX ratio

has plummeted. Furthermore, this weakness occurred in parallel with bank

quarterly earnings reports that were superficially good.

As an

aside, the pronounced relative weakness in the banking sector over the

past three days is the main reason for the bullish shift in our gold model

discussed later in today's commentary.

We can't come up with a good explanation for the sudden bout of

relative weakness in the banking sector. It could be argued that the

demand for bank stocks is declining due to a rise in the banking

industry's interest expense relative to its interest income, but the

contraction of bank interest margins is not a new development and

therefore cannot be the main reason. Also, the valuations of most US bank

stocks are low relative to the S&P500's valuation, so the problem isn't

that bank stocks are too richly priced.

Before we dive more deeply

into this issue we want to see if the relative weakness persists. If it

does it will have implications for other markets, most notably the gold

market.

Moving on, more evidence emerged over the past three days

that the US stock market has completed its downward correction. We are

referring to the fact that both the SPX and the NDX achieved consecutive

daily closes above their respective 50-day MAs. Naturally, the NDX's break

above its 50-day MA was mirrored by the QQQ, a daily chart of which is

displayed below.

As previously mentioned, we bought a small position in QQQ put options

due to the risk of a trend-ending plunge below the February low. This

position will be exited within the next few days, leaving our account

devoid of short-term bearish speculations apart from some TSLA put

options.

The biggest short-term threat facing the stock market now

is the same as the biggest threat that has faced it since the beginning of

the year: higher interest rates. The stock market has become accustomed to

a 10-year bond yield in the 2.80%-3.00% range, but it's likely that at

some point over the coming three months the 10-year yield will move well

above 3.00%. When it does it should usher in the next bout of extreme

stock-market volatility.

Gold and the Dollar

Gold

The Fundamentals

A week ago, we

wrote: "...the fundamental backdrop -- as indicated by the GTFM -- is

very close to turning gold-bullish. In fact, the GTFM shifted into bullish

territory on 11th April, but for a shift to be official it must be based

on weekly closing levels."

It turned out that last week's

mid-week shift into bullish territory by the GTFM wasn't sustained until

the end of the week.

We are presently faced with another bullish

intra-week shift in gold's true fundamentals, in that the GTFM turned

bullish on Tuesday 17th April. Again, though, the shift must be confirmed

by the weekly close in order for it to count.

The Price Action

The gold price

gained a small amount of ground over the first three days of this week,

but the chart pattern is essentially the same as it was at the end of last

week. It's still the case that important resistance lies in the low-$1360s

and that the gold price must achieve a weekly close above this resistance

to signal the start of a strong rally.

At the same time, it is

evident that the bullion market is placing emphasis on the 20-day MA (the

black line on the following chart), in that this MA has regularly acted as

support and resistance over the past several weeks. For example, Tuesday's

downward spike in the gold price ended at the 20-day MA. As a consequence,

a daily close below the 20-day MA (let's say, below $1340 over the

reminder of this week) would warn that an upside breakout was not

imminent.

More evidence of gold market manipulation

According to the article posted

HERE, traders working for large banks have been manipulating the gold

market for many years. In other breaking news, the Earth is round and the

sun sets in the west.

The gist of the above-linked article is that

the US government has taken legal action against some banks and individual

traders working for the banks because the banks/traders engaged in

"spoofing". Spoofing involves entering and then quickly removing large

orders to buy or sell with the aim of causing the price to rise or fall

without having to actually buy or sell. The idea is to influence the

actions of other traders so that the price moves in the desired direction.

It isn't a new idea. For example, Jesse Livermore regularly used similar

tactics during the first 2 decades of the 1900s. In more general terms,

the practice involves making other traders think that you are a large

buyer when actually you want to sell or that you are a large seller when

actually you want to buy. The main difference today is that things happen

far more quickly due to computer-facilitated trading.

There is

nothing inherently wrong with spoofing. It is not unethical and should not

be illegal. It is certainly within the rights of commodity exchanges to

set rules prohibiting the practice and to ban or fine the rule-breakers,

but the government should not be involved.

In any case, like all of

the other direct market-manipulation practices that have come to light,

the effects of spoofing are a) extremely short-term (we are talking

seconds or minutes), b) small by the standards of the average retail

trader/investor, and c) in both price directions. Here's a hypothetical

example: The gold price is at $1350 and Trader Joe wants to buy at $1348.

Joe places a large SELL order on the Comex at $1350 or slightly above,

with no intention of having the order filled. Other traders attempt to

jump in front of this order and in doing so knock the price down to $1348,

thus enabling Joe's BUY order to be filled. Joe's sell order is removed

and the price returns to $1350. Potentially, this could all happen within

a few seconds.

The main reason we are mentioning the above article

and the new cases of banks getting caught breaking the rules is to point

out that this information has absolutely nothing to do with the assertion,

popularised by GATA, that the gold market has been subject to a successful

long-term price suppression scheme. There has never been any evidence to

support this assertion and, since it is based on central and private banks

having powers they do not actually possess, there never will be.

The reality is that over the past 20 years the gold price generally has

done what it should have done based on the fundamental backdrop at the

time. Also, the senior members of the major central banks no longer care

what happens to the gold price (in the 1970s they cared, but they don't

care anymore) and even if they did care they do not have the power to

alter important gold-price trends via direct manipulation. The actions of

the major central banks do, of course, indirectly affect the gold price by

affecting confidence in the official money, but in this regard the actions

are more often than not gold-price supportive. That's why the gold price

is in a multi-generational upward trend relative to commodities in

general.

Gold Stocks

It looked like the Gold Miners ETF

(GDX) was going to break above resistance at $23.00 on Wednesday 18th

April, but the ETF gave up its early gains and again failed to break out.

GDX ended Wednesday's session right at resistance, with the US$ gold

price about $10 below resistance. The market therefore is close to an

upside breakout, but the proximity to resistance also makes it vulnerable

to a price reversal.

We think it's a toss-up as to whether an

upside breakout happens now (that is, within the next few days) or happens

a few weeks from now following some intervening weakness.

As time goes by it is becoming less likely, but the risk of a

trend-ending plunge in the gold-mining indices and ETFs to new 12-month

lows will remain until the gold price breaks above resistance in the

low-$1360s.

The Currency Market

It's

interesting that when stock market volatility suddenly picked up in

late-January, the currency market became much less volatile. At least as

measured by the performance of the Dollar Index (DX), the currency market

has been unusually stable since the late-January stock market peak and

volatility surge.

Over the past seven trading days the DX has

barely moved at all. It remains close to the middle of the narrow

multi-month range from which it must escape to signal the direction of its

next short-term trend. The anticipation of an eventual downside breakout

appears to be building, at least in the minds of commodity speculators,

but until there is a daily close below 88.5 there will be a risk of an

upside breakout.

In our opinion, the major currencies with the best short-term

risk/reward ratios are the Australian Dollar and the Swiss Franc.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Cassini

Resources (CZI.AX). Shares: 276M. Recent price: A$0.067. Cash: about A$2M.

Current enterprise value: about A$17M

Cassini

Resources (CZI.AX). Shares: 276M. Recent price: A$0.067. Cash: about A$2M.

Current enterprise value: about A$17M

With the nickel

price having moved up to US$6.90/pound and with the stock price of Cassini

Resources (CZI.AX) having dropped back to a long-term trend-line (see

chart below), it's time for us to revisit the stock. CZI is a member of

the Small Stocks Watch List (SSWL) and is a leveraged play on nickel via

its JV with mid-tier miner Oz Minerals (OZL.AX) at the West Musgrave

project in WA.

Due to the rise in the nickel price over the past several months, the

West Musgrave project looks economically viable. Moreover, OZL seems to be

bullish on this project's prospects. Therefore, we think that the downward

drift by CZI's stock price to trend-line support has created a speculative

buying opportunity.

We most recently wrote about the CZI-OZL joint

venture and the economics of the West Musgrave project in the 15th

November 2017 Interim Update. For ease of reference, here is a copy of

that write-up:

"CZI's flagship asset is the West Musgrave

Project (WMP) in Western Australia, a project that contains a large,

low-grade nickel-copper resource. The WMP is a JV between CZI and Oz

Minerals (OZL.AX), a mid-tier copper producer. OZL can earn up to 70% of

the project by spending A$36M in stages and advancing the project to the

point where there is a completed FS.

On Tuesday of this week CZI

reported the results of a Scoping Study (that is, a PEA) for the WMP. The

Scoping Study (SS) was done by OZL as part of its earn-in obligations.

The SS is based on the development of a mine with average annual

production of 44M-55M pounds of nickel plus 55M-66M pounds of copper plus

1.5M-2.2M pounds of cobalt over an initial mine life of 8 years. The

pre-production capex is estimated to be A$730M-$800M.

The headline

economics indicated in the SS look good. In particular, the post-tax IRR

is estimated to be 20%-25%. These headline numbers prompted a flurry of

buying in the immediate aftermath of the news and pushed CZI's stock price

up 25% to A$0.125, but when a closer look was taken at the SS details it

became apparent that the robust IRR was based on very aggressive

assumptions and the stock sold off.

The 20%-25% IRR was calculated

assuming a copper price of US$2.95/pound, a nickel price of US$7.13/pound

and an A$/US$ rate of 0.74. The copper price assumption is justifiable

given that the current price is around US$3.00, but the nickel price

assumption is unreasonably high given that the price is currently around

US$5.20 and hasn't been above $7.00 since 2014. Also, the assumed A$/US$

rate is unreasonably low given that the current rate is around 0.76 (the

lower the assumed A$/US$ rate, the better the economics will appear to

be).

Unfortunately, CZI hasn't yet provided information on what

the economics would be under more conservative/realistic price

assumptions, but we suspect that the project would look economically

marginal at today's metal prices and exchange rate.

That's the bad

news. The good news is that OZL has committed to continue with its

earn-in. The larger company could have 'pulled the plug' having spent only

A$3M, but it has opted to spend another $19M over the next 18 months to

boost its stake in the WMP to 51%. It wouldn't be doing this if it didn't

believe that the WMP could be developed into a profitable mining

operation.

Given that the forecast production costs are low (bottom

1/3 for nickel and bottom 1/4 for copper), the marginal-economics problem

is most likely caused by the pre-production capex being too high relative

to the mine size or mine life. It may be possible to resolve this problem

by expanding the mineable resource.

The bottom line is that CZI is

still an interesting speculation. The keys are that its market cap is very

low and that it is being free-carried by OZL to the point where a decision

is made to build a mine."

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.barchart.com/

http://bigcharts.marketwatch.com/

![]()