![]()

![]()

![]()

![]()

- Interim Update 19th August 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

No Weekly Update for

the coming week

We will be taking a short break

and therefore won't be publishing a Weekly Update for the week commencing

Monday 24th August. Normal programming will resume with next week's

Interim Update.

We will send out a Market Alert email if something

unexpectedly dramatic or dramatically unexpected happens in the financial

markets during the period between these commentaries.

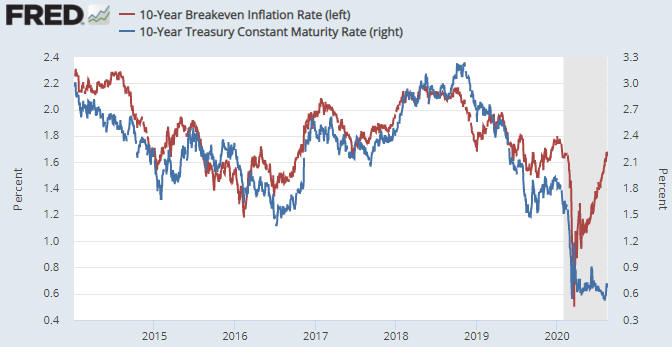

The Fed's

footprints are all over the financial markets

Many analysts downplay the Fed's

influence on bond yields, but we don't think it's possible to explain the

following chart without reference to the massive yield-supressing boot of

the Fed. The chart compares the 10-year T-Note yield with the 10-Year

Breakeven Rate, a measure of the market's inflation (CPI) expectations.

The Breakeven Rate is calculated by subtracting the Treasury Inflation

Protected Security (TIPS) yield from the associated nominal yield.

The chart reveals that the 10-year T-Note yield generally moves in the

same direction as the 10-Year Breakeven Rate. This is hardly surprising,

given that the expected "inflation" rate is usually the most important

determinant of the long-term interest rate. In particular, a higher

expected "inflation" rate usually will result in a higher long-term

interest rate. However, something very strange has happened since March of

2020. Since that time there has been a large rise in the expected CPI

while the nominal 10-year yield has drifted sideways near its all-time

low.

As far as we can tell, there are only two ways that the sort of

divergence witnessed over the past five months between inflation

expectations and nominal bond yields could come about.

One way is

capital flight from outside the US to the perceived safety of the US

Treasury market that overrides other effects on bond prices/yields. This

is what happened during 2011-2012, which is the only other time that a

substantial rise in inflation expectations coincided with flat or

declining nominal US bond yields. In 2011-2012, capital flight to the US

was prompted by the euro-zone's sovereign debt crisis.

Manipulation

by the Fed is the other way that the divergence could arise.

Over

the past five months there has been no evidence of capital flight to the

US. Therefore, it's clear that the Fed has maintained sufficient pressure

to prevent the nominal 10-year bond yield from responding in the normal

way to a large rise in the bond market's inflation expectations. Not

without ramifications, though.

A large rise in the expected

"inflation" rate in parallel with a flat nominal interest rate equates to

a large decline in the 'real' interest rate. In this case, it equates to

the 'real' US 10-year interest rate moving well into negative territory.

This has put irresistible downward pressure on the US$ and irresistible

upward pressure on the prices of most things that are priced in dollars,

including gold, equities, commodities and houses. It has even put upward

pressure on the price of labour, despite the highest unemployment rate

since the 1930s.

At the moment the Fed undoubtedly is pleased with

its handiwork. The rise in the gold price to new all-time highs could be

viewed as a rebuke, but these days no-one in the world of central banking

cares about the gold price. Central bankers do, however, care about the

stock market, and the Fed's governors will be patting themselves on the

back for having helped the S&P500 Index fully retrace its February-March

crash. They also will be pleased that the CPI is rising in spite of the

deflationary pressures resulting from the lockdowns. After all, the

concerns they have expressed over the years about insufficient "inflation"

make it clear that the last thing they want is for your cost of living to

go down*.

However, the Fed is 'playing with fire'. Putting aside

the long-term negative economic consequences of the mal-investment caused

by the Fed's money pumping and interest-rate suppression, if the Fed

continues to prevent bond yields from reflecting rising inflation

expectations then the steady shift currently underway towards hard assets

and anything else that offers protection against currency depreciation

will become a stampede. And once that happens, the sort of central-bank

action that would be required to restore confidence would crash both the

stock market and the economy.

If the Fed continues along its

current path then an out-of-control rise in prices won't be an issue to be

dealt with in the distant future. It possibly will become an issue before

the end of this year and very likely will become an issue by the middle of

next year.

*Nobody with common-sense can

figure out why.

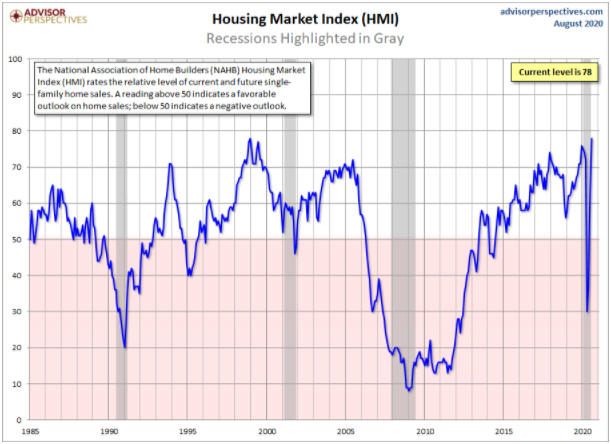

Commodities

Lumber Extreme

In the midst of a recession and in parallel with double-digit

unemployment, the NAHB Housing Market Index just hit an all-time high.

Refer to the following chart for the details. This means that US

homebuilders have never been more optimistic than they are today.

Source:

Advisor Perspectives

The above chart helps to explain the

following chart, which shows that the lumber price has more than doubled

over the past few months and is now much higher than it was at the

pre-COVID peak in February-2020.

This could be almost as good as it gets for the lumber price and for

homebuilder optimism. However, don't be surprised if the sort of price

action seen in the lumber market over the past few months occurs in many

other commodity markets within the next 12 months.

Is the

copper correction over?

We expected a significant

pre-election (July-October) correction in the copper market as part of a

1-2 year cyclical advance from the March-2020 low. The copper price pulled

back from an early-July high near resistance at US$3.00 to a low late last

week near its 50-day MA in the high-$2.70s, before reversing course and

returning to $3.00 over the past three days. So, was that it? Has the

correction come and gone?

Possibly. The latest COT data show that the total speculator net-long

position in copper futures is well below where it was at important price

tops during 2016-2018 (the most recent multi-year bullish period for

copper), so there is scope for additional speculative buying. However,

whether or not there is additional speculative buying of copper in the

short-term will be mostly determined by the currency market. This is

because US$ weakness is the primary driver of the current upward trend in

the copper price.

If the Dollar Index (DX) extends its downward

trend over the weeks immediately ahead then the copper price probably will

test its 6-year high in the $3.30s during September. This could happen,

but it would be risky to bet on further short-term weakness in the US$.

Because the probability of a short-term US$ rebound is high, copper's

short-term risk/reward is neutral at best.

The Stock Market

A risk at the moment is that

there will be too much US$ weakness and, as a result, too much "inflation"

in the stock and commodity markets too soon. This could lead to upside

blow-off moves in many markets over the coming three months, as opposed to

the corrective action we've been expecting. Don't get us wrong, a US$

rebound and resultant sizable pullbacks in stocks, gold and commodities

still describes the most likely short-term scenario, but it's possible

that enough traders now understand the intermediate-to-long-term

consequences of the 'stimulus' measures of the past six months that price

changes that would have occurred over the next 9-12 months will be

compressed into 2-4 months. This risk can be managed by maintaining core

exposure in line with the cyclical rising-inflation trend.

At the

moment, the stock market is signalling neither an acceleration to the

upside nor a reversal. Instead, the S&P500 Index (SPX) is trading quietly

near its February-2020 all-time high.

The NYSE Composite Index (NYA) remains well below its early-2020

all-time high, but it, too, is trading quietly.

The fact that the stock market is complacent doesn't mean that the

short-term upward trend will continue, because the stock market is usually

complacent immediately prior to the start of a sizable downward move.

However, complacency by itself is not a reason to be concerned about

downside risk.

We are concerned about short-term downside risk for

a number of reasons, one being the extent to which a number of

inter-related markets are stretched in one direction or the other right

now. This suggests to us that the stage is set for countertrend moves

lasting 1-2 months.

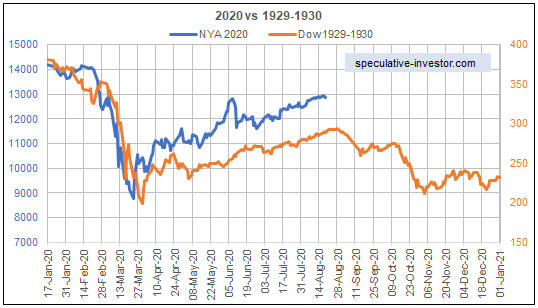

Another concern stems from comparisons between

this year's price action and historical periods with similar price action.

The best example is the following chart-based comparison of the NYA's

performance in 2020 and the Dow's performance during 1929-1930.

If the Fed continues to do what it has been doing then the stock

market will not follow the 1930s path, but there still could be a shakeout

within the next few weeks that acts as a sentiment reset.

Gold and the Dollar

Gold

Here's how we concluded the Gold discussion in the latest Weekly Update:

"The upshot is that a multi-month price top probably is in place.

If so, it's a good bet that the plunge from the 7th August high to the

12th August low was the initial leg down and that the market is in

consolidation mode pending the start of the next leg down. The

consolidation could encompass a test of the 7th August high."

Nothing changed over the first three days of this week.

Two-way

volatility suddenly picked up on 7th August and remains elevated. For

example, the gold price swung through an $85 range on Wednesday 19th

August.

The elevated volatility is, we think, symptomatic of a

topping process that could involve a test of the early-August high within

the next couple of weeks. Furthermore, the fact that the price closed

slightly below its 20-day MA on Wednesday 19th August does not eliminate,

or even significantly reduce, the probability that the high will be tested

before a larger decline gets underway. On the contrary, oscillations

around the 20-day MA are part and parcel of the increased price volatility

associated with broadening disagreement between large traders regarding

the market's prospects.

Our guess is that the correction will end in the low-$1800s in

October, but actually there is no need to guess. Instead, decisions should

be made in real time as new facts related to price action, sentiment and

fundamentals become known.

Silver

Like the

US$ gold price, the US$ silver price has rebounded from an intra-day low

on Wednesday 12th August. It's possible that the rebound from last week's

low will exceed the early-August high near $30, but if it does it should

be viewed as an excellent short-term selling opportunity rather than a

reason to get enthused about an extension of the upward trend.

Further to comments in recent TSI reports, we think there will be an

opportunity to buy silver near its 200-day MA within the next couple of

months.

Gold Stocks

Regarding the gold mining sector

as represented by the HUI, our thinking, as outlined in recent

commentaries, can be summarised as follows:

1) A multi-month price

top (probably the top for the year) was set on 5th August when the HUI

spiked up to 374.

2) The 11th August low (319 for the HUI) marked

the end of the initial leg down and the start of a consolidation phase.

3) The consolidation could encompass a test of the 5th August high.

4) The most likely place for the HUI's ultimate correction low is 260

or thereabouts. The reason is that the area around 260 contains important

lateral support and will soon encompass the 200-day MA.

5)

Near-term strength in the gold sector should be viewed as an opportunity

to do some selling or hedging, but 'core' exposure should be kept due to

the likelihood that much higher prices -- in line with the very bullish

fundamentals for the industry -- will be seen during the first half of

next year.

The price action during the first three days of this

week was consistent with the above.

A weekly HUI close above 374 in the near future would indicate that a

different scenario was playing out. If this were to happen it likely would

be because speculators are front-running the coming US "inflation", thus

bringing forward some of next year's expected price action (the risk

mentioned in the Stock Market section of today's report).

The Currency Market

On Tuesday of this week the Dollar

Index fell for the fifth day in a row. In doing so it moved below its

late-July low to its lowest level in more than two years, thus 'stretching

the rubber band' a little further. On Wednesday it reversed upward.

Due to Tuesday's failed downside breakout, the short-term US$ outlook

has become a little more bullish.

Resistance at around 98 is still

a plausible target for a rebound, but a daily close above 94 is required

to confirm a short-term reversal to the upside.

The financial markets are always interconnected, but rarely has the

interconnectedness been as obvious as it is right now. Currently, most

markets are keying off the US dollar's exchange rate. In particular, many

prices are being pushed upward in relentless fashion as the US$ weakens.

This explains the strong positive correlation between the Australian

dollar (A$) and the S&P500 Index (SPX) illustrated by the following chart.

Over the 6-month period covered by this chart, owning an S&P500 index fund

has been almost the same as owning the Australian dollar.

Based on the message of the above chart, the next significant

correction in the US stock market should go with a significant correction

in the A$. By the same token, if the stock market continues on its upward

path for another 1-2 months than so, in all likelihood, will the A$.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Recent

company news/developments:

Recent

company news/developments:

[Note: AISC = All-In Sustaining

Cost, boepd = barrels of oil equivalent per day, dmt = dry metric tonnes,

CIL = Carbon In Leach, E&P = Exploration and Production, EBITDA = Earnings

Before Interest, Tax, Depreciation and Amortisation (a measure of cash

flow), EV = Enterprise Value or Electric Vehicle, FS = Feasibility Study,

FY = Financial Year, IRR = Internal Rate of Return, ISR = In-Situ

Recovery, JV = Joint Venture, MD&A = Management Discussion and Analysis,

M&I = Measured and Indicated, MLP = Master Limited Partnership, NAV = Net

Asset Value, NPV(X%) = Net Present Value using a discount rate of X%, NSR

= Net Smelter Return or Net Smelter Royalty, O&G = Oil and Gas, P&P =

Proven and Probable, PEA = Preliminary Economic Assessment, PFS =

Pre-Feasibility Study]

*Adriatic Metals (ADT.AX):

The all-stock acquisition of Tethyan Resource (TETH.V) by ADT has been

approved by TETH shareholders and is scheduled to close next month. When

the takeover was announced in May we suggested buying shares of TETH at

around C$0.16 as a way of getting into ADT at a discount. Buyers of TETH

shares at that time could have achieved a gain of up to 200%.

The

next milestone for ADT will be completion of the PFS for its Vares project

in Bosnia, which is scheduled to happen in September-2020. As mentioned

previously, if the PFS confirms the economics of the PEA then ADT's

project contains one of the world's most lucrative undeveloped metal

deposits.

*Golden Arrow Resources (GRG.V)

published its financial results for the quarter ending 30th June 2020.

At 30th June the company had no long-term debt and C$29M of working

capital. However, the bulk of its working capital is an investment in SSR

Mining (SSRM), which is worth a bit less today than it was at the end of

June. Current working capital is around C$27M, or about C$0.23/share.

In addition to its working capital, GRG has a portfolio of

early-exploration-stage projects in Chile, Argentina and Paraguay.

The current price of a GRG share (C$0.185) is a discount of about 20% to

the company's liquid financial assets. This means that despite the

increasingly speculative market for gold mining stocks, the stock market

continues to attribute negative value to GRG's exploration-stage projects.

This makes GRG a value proposition, but a large increase in the stock

price will require a discovery.

Adding an all-purpose hedge

Adding an all-purpose hedge

The euro probably has

just made or is close to making a short-term top. If so, a routine

correction would take the CurrencyShares Euro Trust (FXE) down to around

$109. However, speculators have piled into long euro positions to the

extent that the coming correction could push the FXE down as far as $106.

That would be the equivalent of the DX rebounding to around 98.

Given that US$ weakness has been the primary driver of rising prices

in the equity and commodity markets over the past few months, FXE put

options could be used to hedge against short-term weakness in these

markets. In effect, a bet against FXE could be viewed as an all-purpose

hedge against short-term weakness in everything that has been boosted in

price by the declining US$.

The FXE December-2020 US$108 put

option has been added to the TSI List at the mid-point of its 19th August

closing bid-offer spread (US$0.75-$0.85), primarily as a hedge or a form

of insurance.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://research.stlouisfed.org/

![]()