![]()

![]()

![]()

![]()

- Interim Update 19th September 2018

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Housekeeping

Taking a break

Please note that TSI will be on vacation next week. A Weekly Update

will be published this weekend (22-23 September), but there will be no

Interim Update next week and no Weekly Update on 30 September. We'll be on

a remote island and may not have ready access to a reliable internet

connection, but we still should be able to send out a brief update via

email if something unexpected and dramatic happens in the markets while we

are away from the office.

Problems receiving TSI emails

If you have an aol.com, a verizon.com or a rogers.com email address

then there's a good chance that you didn't receive email notification of

the last two TSI reports (the Interim Update published on 13th September

and the Weekly Update published on 16th September). It seems that after a

great many years with no issues, the aforementioned ISPs have decided to

block our emails. When an email is blocked by an ISP it registers as a

"bounce" in the reports that our email provider (MailChimp) generates for

us.

We are making a minor change to the way the emails are sent

that hopefully will get around the problem. The change should be fully

implemented by the time we send out the email for the Weekly Update.

On a related matter, you always can get access to the commentaries by

logging in at the TSI web site.

Industrial Metals

Update

Copper Bottom

President Trump announced earlier this week that he was going ahead

with tariffs on US$200B of goods imported from China. The tariff (tax) on

these goods will be 10% beginning next Monday, increasing to 25% on 1st

January. Naturally, China's government responded in kind if not in size.

The tariffs constitute a war on consumers, with the US government

attacking US consumers and China's government retaliating by attacking

Chinese consumers. It brings to mind the movie "Fight Club", in which the

main character sometimes beats himself up.

It appears that Trump is

willing to escalate the war on US consumers until something breaks. The

strangest thing is, right now hardly anyone seems to care. Commodity

traders cared during June-August when the prices of many commodities

plummeted due to selling pressure stemming from fear of what the tariffs

would do to international trade, but despite the escalating economic war

there are now signs that commodity prices are beginning to recover. Most

notably, the copper price was on the verge of breaking out to the downside

on Tuesday after the announcement regarding $200B of new tariffs, but it

reversed course and rallied. This counterintuitive reaction to news is

preliminary evidence that an intermediate-term bottom was put in place

when the price dropped to $2.55 last month.

A daily close above

$2.76 would be additional evidence that at least a multi-month bottom is

in place.

Platinum Bottom

On Tuesday of this week the

platinum price broke above short-term lateral resistance and closed above

its 50-day MA for the first time since February. This is preliminary

evidence that a sustainable bottom is in place.

That being said, in

each of the past 5 years the platinum price made an important low in

December. Dropping back to below the 50-day MA within the next 2 months

would suggest that another December low was on the cards.

T-Bond Update

The T-Bond price has dropped back to near its May-2018 low. This means

that the T-Bond market is close to breaking out to the downside.

We

expect the T-Bond price to be a lot lower by this time next year, but we

haven't been expecting a downside breakout to happen during

September-October of this year. On the contrary, we've been anticipating a

bear-market rebound.

A bear market rally lasting 2 months or more

remains our favoured short-term scenario for the T-Bond, but the risk of a

sooner-than-expected downside breakout obviously has increased. If the

T-Bond does break out to the downside in the near future it could have a

similar effect on the stock market as the T-Bond's late-January downside

breakout, that is, it could be the catalyst for a sharp stock market

decline.

When will tighter US

monetary conditions start to matter?

The US monetary inflation rate, as indicated on the following chart by

the year-over-year rate of change in US True Money Supply (TMS), has been

near the bottom of its 20-year range since the middle of last year, but

the economy still seems to be doing fine and nothing bad has happened to

the stock market. With the monetary inflation trend showing signs of

having turned upward early this year, in the current cycle has the US

sidestepped the painful effects of rapid money creation and seamlessly

transitioned from one credit-fueled boom to another? Putting it another

way, is it different this time?

Although "it's different this time" is reputed to be the financial

world's most dangerous phrase, to some extent it's always different. In

particular, although creating a lot of money out of nothing inevitably

leads to major problems, the problems will manifest in different ways and

at different times depending on a) how/where the new money is injected, b)

the domestic economic and political situations and c) what's going on in

other parts of the world.

In one respect the current cycle has been

very different in that the Fed has been directly responsible for a large

proportion of the US$ creation. Normally the Fed creates no money

directly, but acts as a backstop for the money creation of the commercial

banks.

This difference is huge. It means that during the current

cycle the bulk of the new money entered the economy via the financial

markets instead of the way it traditionally enters -- via loans to

businesses and individuals. This is why the post-2011 boom has been far

more evident in the stock market than the real economy. Also, it could be

why, this time around, there is a much longer-than-usual gap between the

tightening of monetary conditions and the effects of the tightening

becoming obvious in prices and economic statistics.

Just to be

clear, there is no chance that the US economy and financial markets will

escape the painful knock-on effects of the rapid money-supply growth of

2009-2016, but it's possible that over the next 6 months it will seem as

if it has. That's especially so if the Fed puts its rate-hiking on hold

due to concerns about an inverted yield curve.

As mentioned in

previous commentaries, if at this late stage of the economic expansion the

Fed were to become more concerned about the flattening yield curve than

about "price inflation", a consequence could be a sort of inflationary

blow-off during 2019-2020. That's a scenario in which it would be a bad

idea to be short anything except bonds.

Returning to the question

of when the tighter US monetary situation will start to matter, it matters

right now because it is part of the reason that the yield curve is close

to inversion. As such, it could prompt a premature end to the Fed's

rate-hiking campaign. And if this were to happen within the next few

months it could lead to the superficial effects of inflation becoming less

evident in the stock market and a lot more evident in the commodity

markets and the CPI.

The Stock Market

The S&P500 Index (SPX) managed

to get through the first three days of this week without doing anything

significant. Something significant would be closing above the all-time

high achieved last month (2917) or closing below support at 2870.

Gold and the Dollar

Gold

Over the first three days of this week the US$ gold price oscillated in a

narrow range around its 20-day MA. The price action was not significant.

Gold must break above $1220 to provide the next piece of evidence that

a meaningful rally has begun. Achieving such a breakout would suggest a

short-term target of around $1280. Gold must also avoid closing a day

below $1190, as that would warn that a decline to a new low for the year

was underway.

It's likely that moving up to around $1280 is the best that gold will

be capable of as long as the fundamental backdrop remains bearish,

although there is one way that a sizable rally in the US$ gold price could

occur in the face of an overall-bearish fundamental situation. It could

occur in response to US$ weakness.

A gold rally that was driven

solely by weakness in the US$ would involve a tradable upward move in US$

terms and minimal strength in terms of most other major currencies. It

also would involve weakness in gold relative to many other commodities.

Gold Stocks

In the latest Weekly Update, we

wrote:

"GDX's price action over the final two days of last week

didn't provide much in the way of new information. As illustrated below,

there was a touch of the 20-day MA on Thursday and then a minor pullback.

Additional information will be provided early this week, in that IF a

multi-month bottom is in place then the rally should resume within the

next two trading days without a significant extension of the pullback from

last Thursday's high."

The rally resumed immediately and on

Wednesday 19th September GDX achieved a solid daily close above its 20-day

MA. The next resistance of significance is defined by the late-August

rebound high ($19.50) and the 50-day MA. These resistance levels probably

will be tested within the next several days, although we won't be

surprised if there is some 'corrective' action during the next 1-2 days.

At this stage we aren't expecting more from the gold-mining sector

than a 1-3 month rebound to resistance*, but we will continue to take the

evidence as it comes. A larger and longer rally is possible, but only if

there is a substantial improvement in gold's true fundamentals.

*For GDX, the maximum that would be accomplished by a counter-trend

rebound is a test of intermediate-term resistance near $21.

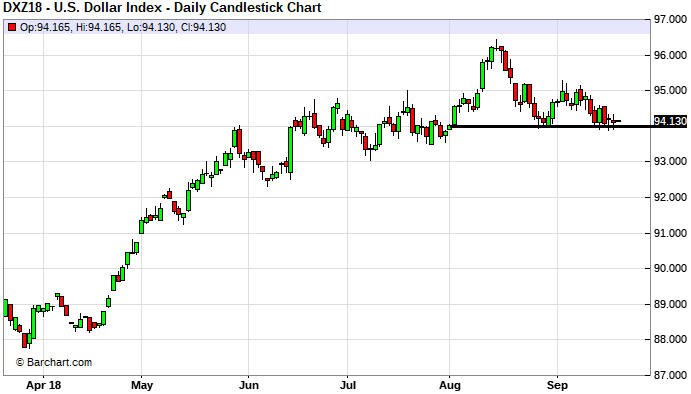

The Currency Market

The first of the following

charts makes it look like the Dollar Index (DX) broke out to the downside

on Tuesday 18th September, but this is just a quirk of the Stockcharts.com

system. Stockcharts shows the nearest futures contract and when one

contract is about to expire it automatically switches to the new nearest

contract. This switching from a nearer to a later contract causes price

gaps to appear in the chart that don't reflect the actual trading. For

example, on Tuesday the Stockcharts.com system stopped showing the

September contract (DXU) and started showing the December contract (DXZ)

on the $USD chart, resulting in a misleading price decline on the chart

due to the December contract being about 0.4 points below the September

contract. In this case, switching from one contract to the next

transformed a 0.15-point daily gain in the market price into a 0.26-point

daily loss on the chart.

This is not a defect in the Stockcharts

system; it's just the way that charts based on the nearest futures

contract work. It's something to be aware of when looking at futures-based

price charts that span multiple contracts.

At this stage there has

been no downside breakout in the DX. For the December contract (the

current nearest futures contract), the important nearby support lies at

94.0.

The technical 'line in the sand' is more clearly defined for the euro

than for the DX. In the euro's case it looks like the 'neckline' of a

well-defined H&S bottom is around 117.50.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://www.barchart.com/

![]()