![]()

![]()

![]()

![]()

- Interim Update 20th February 2019

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The copper market is

performing as expected

In our 31st December commentary,

we wrote:

"We expect the copper price to do well during the

first half of 2019 in response to the extremely low LME copper inventory

level, a rebound in the stock market and the temporary cessation of the

US-China trade war. In fact, the prices of all base metals are set to

rebound over the next few months for the same reasons. However, copper's

price action suggests that a spike to a new 12-month low could precede the

start of a tradable rally."

The copper price spiked to a new

12-month low a couple of days later and then reversed course. This

prompted us to write (in the 14th January Weekly Update) that the bottom

might be in place. We subsequently (in the 6th February Interim Update)

mentioned a minimum short-term upside target of US$3.15.

As

illustrated below, the copper price broke above resistance at $2.87 on

Wednesday 20th February. More important resistance at $2.95-$3.00 is about

to come into play and could halt the advance temporarily, but a short-term

rise to $3.15 or higher remains likely.

The Stock Market

Still uncertain about

whether the long-term trend has changed

The NYSE Composite

Index (NYA) includes all stocks traded on the NYSE, which means that it

includes more than 1900 stocks, while the S&P500 Index (SPX) comprises 500

large-cap stocks. The ratio of these two indices (NYA/SPX) is therefore a

measure of how the overall market is performing relative to the

largest-capitalisation stocks.

The top section of the following

long-term chart shows the NYA/SPX ratio and the bottom section shows the

NYSE Advance-Decline Line (ADL). The performance of the NYA/SPX ratio

suggests that the October-2018 top was very different to the October-2007

top, but similar to the March-2000 top. The ADL, on the other hand,

suggests that the current situation is not similar to the situation around

either of the previous two major tops.

The ADL trended downward for about two years prior to the March-2000

major peak. This indicates that the bull market's final 2-year advance got

progressively narrower. The ADL only trended downward for a few months

prior to the October-2007 major peak, but it continued to trend downward

until the bear market ended in early-2009.

This time around, the

ADL diverged bearishly from the SPX for only a few weeks prior to the peak

and has since risen to a new high. This is a very strange turn of events

IF a bear market began last October.

Perhaps it is different this

time and the ADL's recent rise to a new all-time high is a misleading

signal (a bull trap). We don't know (and neither does anyone else), but

the ADL's rise to a new high has tipped the scales in favour of the

long-term bull market having further to run. If it were to occur, an

extension of the bull market probably would be of greatest benefit to

late-cycle sectors such as consumer staples and commodities.

Bear

market or not, there's a good chance of a significant pullback within the

coming few weeks and a test of the December-2018 low during the second

half of the year.

McClellan Oscillator trumps Put/Call

During the second week of January there was a McClellan Oscillator

(MO) surge to an unusually high level. We explained the potential

implications of this in the 9th January Interim Update, as follows:

"Over the past three trading days the MOs for both the NYSE and

the NASDAQ moved significantly further into 'overbought' territory -- to

at or near 20-year highs. A chart showing the NYSE Composite Index and the

NYSE MO is presented below. The signal is not infallible, but an MO surge

of this magnitude suggests the sort of internal strength that usually is

followed by only minor setbacks over the ensuing few weeks."

Within about a week of the bullish MO surge the TSI Put/Call Indicator

(TPCI) came very close to generating a sell signal. This muddied the

waters. It meant that one reliable indicator was warning of short-term

downside risk at the same time as another reliable indicator was warning

that short-term downside risk was low and that the market probably would

grind upward over the ensuing few weeks.

We now know that the MO

signal was correct. This suggests that when our put/call indicator and the

MO simultaneously reach extremes (something that almost never happens),

the MO signal should be given priority.

The following chart shows

the NASDAQ Composite Index and the NASDAQ MO. Notice that over the past

few weeks the MO has pulled back from its extreme while the market has

moved upward with only minor setbacks.

The MO signal has run its

course, but even so there is no reason to expect more than a 50%

retracement of the December-February rebound prior to a rally to new highs

for the year.

Gold and the Dollar

Gold

For

the past several weeks our expectation has been that the US$ gold price

would test major resistance in the $1360s during the first quarter of this

year. From our perspective the main uncertainty revolved around whether

there would be a correction to as low as $1250 prior to a rise to test the

aforementioned resistance. This uncertainty was expressed as follows in

the latest Weekly Update:

"...the market has been

consolidating/correcting since late-January. The price bounced after

hitting its 20-day MA late last week, which could mean that the correction

is over and that a rise to major resistance in the $1360s has begun.

However, it's just as likely that the correction isn't complete and that a

drop to $1250-$1280 will precede a move up to test the aforementioned

major resistance."

The US$ gold price broke above its

late-January high during the first half of this week, so it looks like the

test of major resistance will happen sooner rather than later.

A test of resistance in the $1360s could involve a slightly lower

high, for example, a downward reversal from the mid-$1350s. It could also

involve a slightly higher high, such as a spike up to the $1380s.

Note that a downward reversal following a spike above resistance would be

more bearish than a downward reversal from below resistance, because then

we would be dealing with a false upside breakout.

Silver

As illustrated below, the US$ silver price has not yet closed above or

traded above its late-January high. Therefore, it is yet to confirm this

week's upside breakout in the US$ gold price. This is not a bearish

non-confirmation, because it is normal for silver to lag gold until the

late stages of a rally. It is simply noteworthy.

We think that

silver stands a good chance of trading up to the low-$17s within the next

few weeks, at which point it would be a short-term sell. It would be a

short-term buy following a pullback to the $15.20s.

Gold Stocks

From the latest Weekly Update:

"Due to the depressed level of the HUI/gold ratio and the

potential intermediate-term 'coiling' patterns evident in the charts of

the gold-stock indices and ETFs, the short-term risk/reward is more

bullish for gold mining than for gold bullion. If GDX and the HUI can

close above their late-January highs then quick-fire additional gains of

10%-20% could be in store. Moreover, last week's price action suggests

that the risk on new long positions could be limited to a few percent by

placing a sell stop slightly below the 14th February low (163 for the HUI,

$21.84 for GDX). The sell stop is critical in this case."

The

HUI and GDX broke above their late-January highs early this week. Here is

a daily chart of the HUI showing the breakout.

The sell stop remains critical as there is no telling when a

significant top will be put in place. For now the stop could be kept

slightly below the 14th February low, but if the HUI closes above 180 then

the stop should be raised to 169.

Shortly after a short-term top is

put in place the top should be confirmed by the HUI/gold ratio.

Confirmation would come in the form of a daily close below the 40-day MA

(the blue line on the following chart).

This is an interesting time

because the position of the HUI/gold ratio is now roughly the same as it

was at the multi-month tops of February-2017, September-2017, January-2018

and July-2018. Additional strength from here will be evidence that despite

the choppy price action of the past several months, the rally from the

September low is not just another counter-trend rebound within the context

of a multi-year decline.

The Currency Market

Almost nothing has

happened in the currency market since the end of last week. The only

comment we'll make is that the euro has been chopping back and forth

within a narrow horizontal range (112-115) for long enough now that there

likely will be significant follow-through in the direction of the eventual

breakout.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Stocks

List Review, Part 3

Stocks

List Review, Part 3

A general review of the TSI Stocks

List started with the "Trading Positions" section in the 6th February

Interim Update. The review continued with the "Gold and Silver" section in

the 11th February Weekly Update and concludes today with the "Other

Stocks" section. Here is a brief comment on each of the stocks in this

section:

1) Alkane Resources (ALK.AX) owns the

Tomingley Gold Operation (TGO) in New South Wales. It also owns the Dubbo

Project (DP), which is construction-ready and slated to produce zirconium

(43% by revenue), hafnium (10% by revenue), niobium (17% by revenue) and

REEs (30% by revenue). The TGO has generated a significant amount of cash

for ALK over the past few years, but it always will be a small-scale

operation and as such will never warrant a large stock-market valuation.

The DP, on the other hand, has the potential to generate huge wealth and

is the reason for our on-going interest in ALK.

The company has a

healthy balance sheet, with no debt and cash-plus-investments of around

A$80M. With 506M shares outstanding and a current stock price of A$0.20,

in effect the market is valuing the combination of the TGO and the DP at

only A$20M. This seems absurd, given that the DP's 2018 FS estimated a net

present value of about A$1.2B at current commodity prices and using a

discount rate of 8%.

The seemingly-absurd market valuation can be

explained by the snail's pace at which ALK's management is moving the

Dubbo Project forward. Before construction can commence, offtake

agreements must be put in place and financing must be arranged for the

A$1.3B of up-front capex.

Ideally, financing of the up-front capex

will be achieved by entering a JV with a much larger company. The reason

is that even if it is possible for a small mining company to arrange all

of the financing required to build a substantial mine, it is a high-risk

path to take. The cost overruns that often occur during the construction

phases of large projects generally can be taken in stride by major mining

companies, but can be life-threatening to small companies that have chosen

to 'go it alone'. And even if the small company is able to arrange

sufficient additional financing to cover the overruns, the high cost of

this additional financing probably will crater the stock price. A good

recent example is Nemaska Lithium (NMX.TO), which lost about 45% of its

market value last week after announcing a cost overrun at its

construction-stage mining project.

This might be an unfair

appraisal, but we get the impression that in terms of sorting out the

offtake agreements and construction financing ALK's position today is not

materially different to what it was three years ago. We hope we are wrong

and tangible progress will be demonstrated within the next few months.

The bottom line is that ALK is extraordinarily cheap, but it will stay

that way until/unless a deal is done that enables the DP to move into the

construction phase.

2) Africa Oil (AOI.TO) is like

a fund that owns stakes in oil exploration/production projects in Africa.

It has several assets, but the bulk of its current value (at C$1.20/share,

the market cap is C$565M) is associated with two investments.

The

first of these flagship investments is the company's 25% stake in the

development-stage South Lokichar Basin in Kenya. It is expected that over

the next few years South Lokichar will be developed into a producing oil

field with output of around 100K barrels of oil per day (bopd). The

initial stage is estimated to have total capex of US$2.9B and result in

production of 60K-80K bopd.

The second of these investments is the

soon-to-be-completed acquisition of 12.5% of a company that holds

interests in multiple producing and developing offshore oil fields in

Nigeria. This acquisition will transform AOI from an oil

explorer-developer to a profitable oil producer.

AOI should perform

well over the coming 12 months as long as the oil market is stable or

strong. At this stage we expect a strong oil market during at least the

first half of 2019.

We are comfortable with AOI's progress and

on-going inclusion in the TSI List.

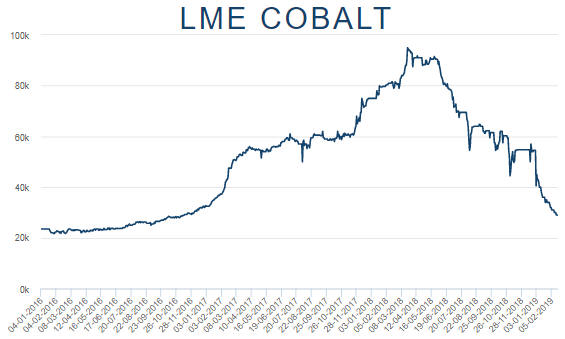

3) Clean TeQ (CLQ.AX,

CLQ.TO) is developing the Sunrise nickel-cobalt-scandium project

in New South Wales (NSW), Australia. When it was added to the TSI List our

suggestion was to buy half a position at around A$1.03 (the price at the

time) and wait for the FS before deciding whether to buy more.

The

results of the FS were published in July and made it clear that CLQ's

project was not as valuable as we thought. Also, the FS showed that the

project's economics were very sensitive to metal prices, which would be a

plus after the metals resumed their bull markets but would work against

CLQ while the cobalt and nickel markets were in correction mode.

We

concluded that it made sense to stay with a half-size position pending

evidence that the cobalt correction had run its course. That evidence

still hasn't arrived. In fact, the cobalt price made a new 2-year low over

the past few days and is down by an incredible 70% from its March-2018

peak. Refer to the chart displayed below for the gory details.

As is the case with Alkane's project, financing of the huge up-front

capex (US$1.5B) for CLQ's Sunrise project ideally will be achieved by CLQ

entering a JV with a much larger company. However, the project would not

be economically viable at current metal prices so the probability is low

that such a deal will be done in the near future.

We are not

comfortable with CLQ. In its favour is a healthy balance sheet (net cash

in excess of A$100M) and a low enterprise value (about A$120M at its

current A$0.31/share price), but it is clear that we should have removed

it from the List as soon as the disappointing FS results were announced.

Despite the large decline in its price it is not a good candidate for new

buying, although there could be a strong rebound in the stock price in

response to strengthening metal markets over the next three months.

4) Energold Drilling (EGD.V) provides drilling

services to the mining and O&G industries. Also, it has begun to diversify

into geothermal drilling as part of an effort to smooth-out the large

seasonal swings in its traditional business. In particular, the goal here

is to boost revenue outside the traditional November-April Canadian

oil-sands drilling season.

EGD's stock market capitalisation is

extremely low relative to the size of its business. This is evidenced by

the fact that it is generating revenue at the rate of about C$90M/year and

has a current market cap of only C$9M (at C$0.17/share). This should

enable EGD's stock price to make a rapid recovery once the market for

junior resource shares turns the corner.

The company also has about

C$17M of long-term debt.

Our main concern with EGD is that its

revenue has been slowly growing for the past 2 years but the revenue

growth hasn't translated into profits and positive cash flow. Instead,

there has been a steady draining of cash from the balance sheet. This is

probably the main reason for the extremely low market valuation.

EGD will be risky until it becomes cash-flow positive, but despite the

risk the stock's risk/reward is very attractive at the current price.

5) Cobalt 27 Capital Corp. (KBLT.V) started out as a

pure play on cobalt via its ownership of physical cobalt (2,983 tonnes a

year ago, about 2,700 tonnes today). It subsequently added a few cobalt

royalties on early-stage projects, but at this point almost all of its

value was still associated with its stash of physical cobalt. Then, in

May-June of last year it did two major cobalt streaming deals. It

purchased cobalt and nickel streams associated with the stake owned by

Highlands Pacific (HIG.AX) in the fully-operational, long-life Ramu

nickel/cobalt project in Papua New Guinea (PNG), and it purchased a cobalt

stream associated with the massive Voisey's Bay nickel mine in Canada.

The timing of the streaming deals was bad, because it turned out that

in May-June of last year the cobalt price was in the early part of huge

decline. Fortunately, however, the Ramu streaming deal fell through and

was renegotiated in January of this year as a takeover of HIG.AX. Due to

the renegotiation, KBLT will end up with slightly more exposure to cobalt

and substantially more exposure to nickel than under the original deal, at

a much lower up-front cost.

KBLT has been severely punished in the

stock market due to the huge decline in the cobalt price and the

substantial downward correction in the nickel price, but its balance sheet

is healthy and the company's management appears to be adequate (management

has made some good moves and some bad moves, but overall it has been

satisfactory). Most importantly, KBLT has transformed itself into the

stock market's premier battery-metals play, so once the cobalt and nickel

prices begin to rebound with conviction there should be a large upward

re-rating of KBLT shares.

If you are going to own only one

battery-metals stock, KBLT should be it.

6) Mineral

Resources (MIN.AX) was added to the TSI List to provide

relatively low-risk exposure to lithium, although it generates most of its

revenue from pit-to-port mining services. The reliable and profitable

mining-services revenue enables the company to pay a significant dividend.

The company's business strategy involves taking part ownership of

exploration-stage projects that it helps to finance through to production.

In most cases its aim is to end up with a life-of-mine service contract

and to sell down its equity stake in the mine, but it retains ownership

stakes in some projects. These projects provide direct exposure to the

prices of iron-ore and lithium.

The company's most valuable single

asset is the Wodgina lithium project in Western Australia's Pilbara

region. MIN and Albemarle (the world's largest lithium producer) are in

the final stages of negotiating a JV on this project. Assuming that the JV

is established as presently agreed between the companies, Albemarle will

pay US$1.15B in cash to MIN in exchange for 50% of the project. This deal

values Wodgina at A$17 per MIN share, making the current price of

A$16.80/share for the entire company seem very low.

We remain

comfortable with MIN and have a 2-year target of A$30/share in mind. It is

the lowest-risk way we know of to obtain exposure to lithium. Our own

account also has lithium exposure via Kidman Resources (KDR.AX), which we

have mentioned a few times in TSI commentaries.

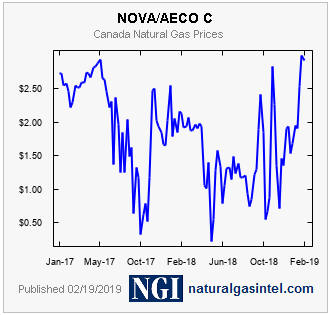

7) Petrus

Resources (PRQ.TO) is a junior Canadian natural gas (NG) producer

with current production of 8,000-9,000 boe/day. Its current market cap is

only about C$25M, which is extremely low relative to its production and

assets. However, it is also carrying a debt burden of about C$140M, so its

enterprise value is much greater (about C$165M).

PRQ's financial

performance depends to a large extent on the price of NG in Canada. As

illustrated by the following chart, over the past 2 years the Canadian NG

price has oscillated at a very low level -- from close to zero to around

$3.00/GJ. It presently is near the top of this range, but it will have to

make a sustained move to much higher levels to have a big effect on PRQ. A

sustained move to much higher levels eventually will occur due to

increasing liquefied natural gas (LNG) demand from China and Japan, but

the timing is unknowable.

Chart source:

https://www.naturalgasintel.com/

Although it isn't in the TSI

Stocks List, in the current market we would opt for Peyto Exploration

(PEY.TO) over PRQ.TO for new NG-focused buying. PEY's market value has

fallen by almost as much as PRQ's over the past three years and PEY is

better positioned to ride out whatever remains of the Canadian NG bear

market.

Note that in an effort to take more control over their own

destiny, PEY and nine other Canadian NG producers

recently formed a consortium with the aim of building a new LNG export

terminal on Canada's west coast.

8) Tinka Resources (TK.V)

owns the Ayawilca exploration-stage zinc project in Peru. The project has

both the size (the current resource estimate includes 7.4 billion pounds

of zinc) and grade (the average zinc grade is about 6%) going for it.

Also, it is in a relatively low-risk jurisdiction. Therefore, there's a

good chance that TK eventually will be bought be a much larger company.

Our hope is that the takeover bid will come after the stock price has

already moved much higher.

The first look at Ayawilca's economics

should arrive via a PEA in the second quarter of this year.

At its

current price of C$0.31/share, TK's market cap is about C$80M. It

potentially will be valued at a multiple of this within the coming two

years.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://www.lme.com/

![]()